Uranium: A complete guide of the investment thesis

Uranium: A complete guide of the investment thesis

Deep dive into nuclear energy, the uranium market and how I am investing in it

Summary

In this report I will go through why nuclear energy is the clear path for energy, both in the short and long term. And I will explain how I am playing this thesis.

Uranium has been in a supply deficit (relative to primary production) since the 1990s.

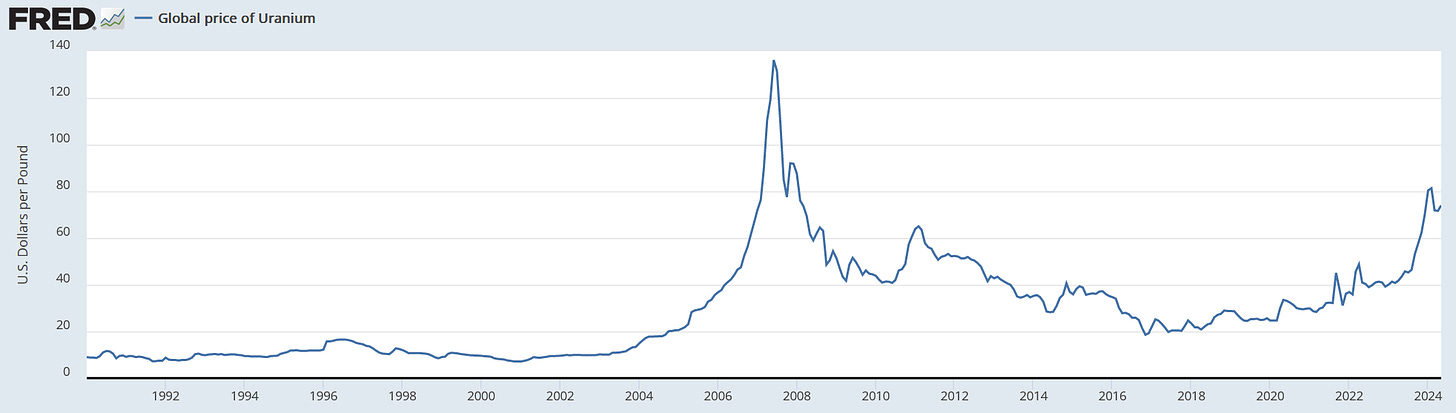

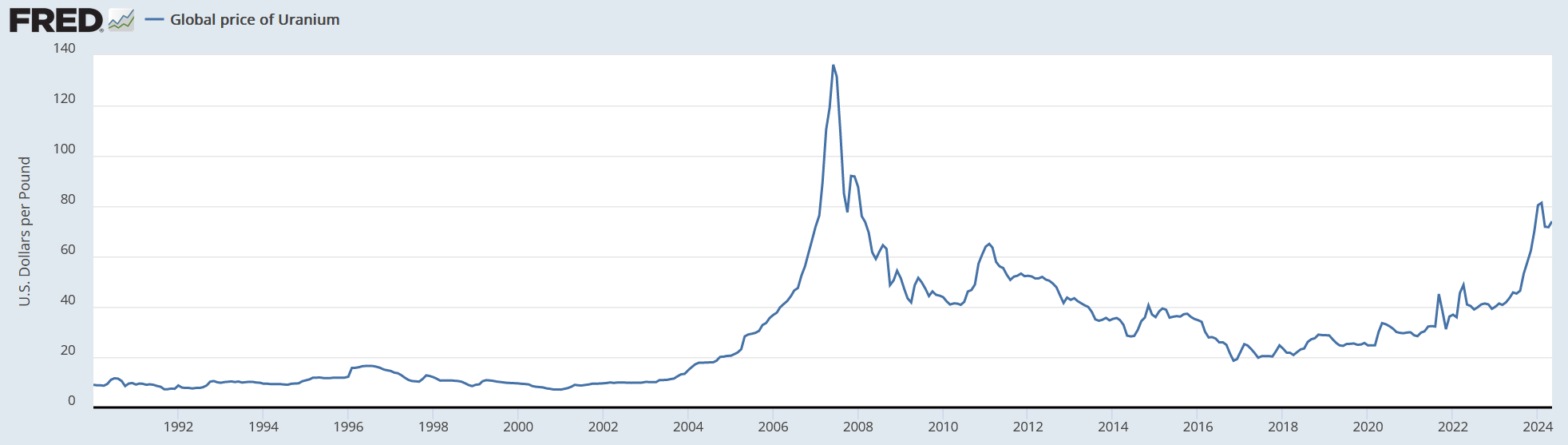

In the early 2000s uranium prices went from a low of $7/lb in 2000 to $136/lb in 2007. After Fukushima in 2011, price plummeted to $18/lb in 2018 and prices have now since recovered to around $90/lb.

Uranium equities have had quite a run since 2018, particularly since 2020. Billions have been poured into equities and uranium ETFs have gone from $150M in AUM in 2020 to $5 billion in 2024.

These inflows have benefited many investors, including myself. From 2017-2018 to 2022 I was fully invested in uranium and got a 1000% average return on my portfolio.

I believe this rush into uranium has pushed equity valuations of most miners and juniors from being undervalued, to being overvalued. Therefore, I believe the best way to play this thesis going forward is physical uranium.

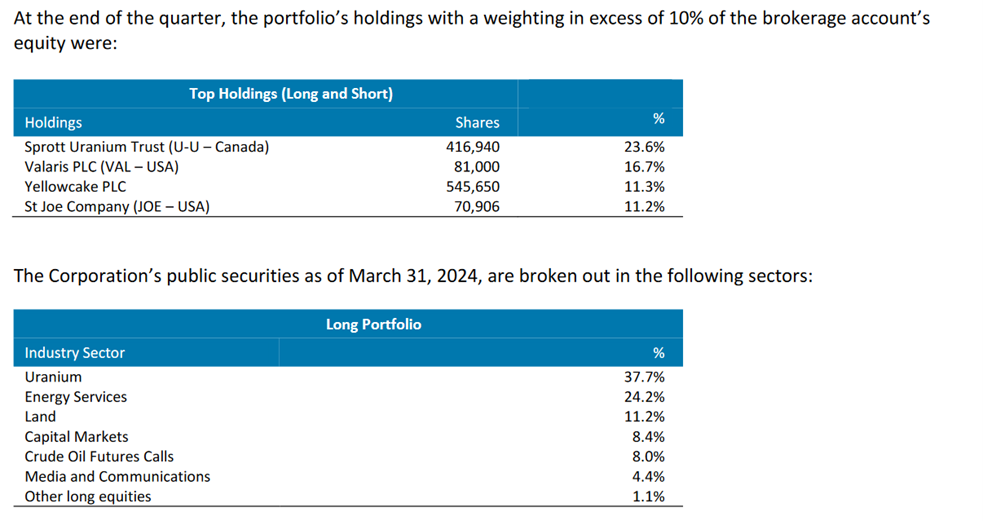

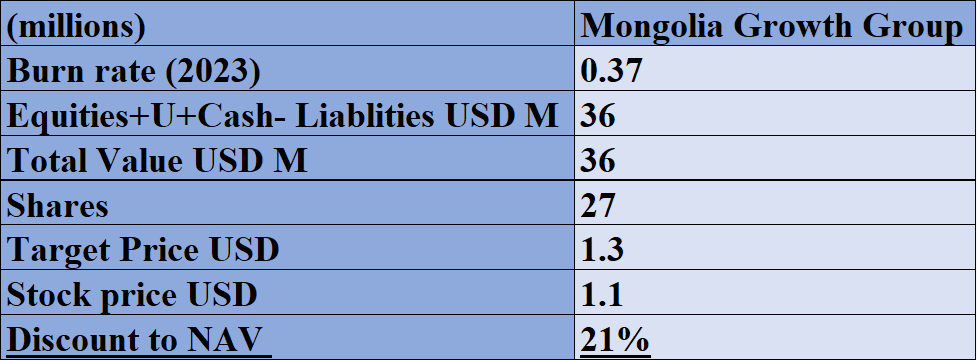

My top pick for the sector is Mongolia Growth Group (CVE: YAK). Which trades at a 21% discount to NAV. It also has revenues that cover most of the operating expenses. The holding is not a pure play uranium play though, as it holds around 40% of its assets as uranium investments.

However, I also hold shares in District Metals (CVE: DMX), a highly speculative play of uranium development in Sweden. It trades at a massive discount to peers as uranium mining is illegal in Sweden, however the Swedish government is trying to remove the ban on uranium mining.

There are other ways to hold physical uranium but the discount to NAV that Mongolia Growth Group trades at, makes it the most attractive uranium physical vehicle by far in my opinion.

Uranium price. FRED.

YAK stock price. Google finance

Glossary

Glossary of terms.

Introduction

Back in 2017 I accidently learned about the uranium investment thesis through a YouTube video about uranium miners. The thesis made perfect sense: the industry was selling uranium at half the price that is costed them to produce it, while the nuclear energy sector was stable and had a promising future. I went all in into uranium juniors and thanks to that I got 1000% average return on my portfolio when I sold them all in 2022 and achieved financial independence. Not long before that I had seen a conference by Warren Buffet. He had given a talk at a university (years before), and one quote stuck with me while I listened the uranium conference I had found, he said something along the line of: “I fully understand the chewing gum business, and I know what the dynamics of the business will look like 20 or 40 years down the road. If you understand these dynamics of an industry and you can buy the industry cheap, you are going to make a lot of money”. It made perfect sense to me. I could “buy” the uranium industry while it was going bankrupt, knowing fully well that in 20 or 40 years the nuclear energy industry was going to thrive.

Now the thesis has somewhat changed. Now uranium firms are no longer going bankrupt. But the deficit is growing due to supply side issues. Except this time, I believe that uranium firms are fairly valued or overvalued. And I believe the play now is to buy physical uranium. If the deficit persists, I believe uranium will be trading at multiples from what is trading now. And if I’m wrong the uranium price will remain stable or even perhaps rise a little. This is the motto of my investment philosophy: “I flip a coin, if its tails I win multiples of my money, and if its heads I lose little or nothing”.

Risk and reward are often misunderstood concepts in the investment world. Particularly among computer scientists and other people trained in STEM fields. They believe that risk is volatility and there is a correlation between risk and reward. I believe this is a common misconception among other investors as well, in popular culture people say, “big risk, big reward”. I don’t believe they are correlated. In 2020 investing in uranium (or coal) was almost risk free as the industry had been decimated and yet it offered immense upside. In fact, from the lows of 2020 to the highs of 2022, a lot of uranium firms delivered anywhere between 200% and 2000% returns.

Firstly, I will analyse why Mongolia Growth Group is the best way to “buy” physical uranium. Secondly, I will go into a deep dive about District Metals. And finally, I will write as to why nuclear energy and uranium have a bright future. For those unfamiliar with this thesis, I recommend jumping straight into the third section of the report, as you should first understand the nuclear and uranium markets to fully understand the dynamics of the sector. For those familiar with uranium, I have put the thesis of YAK and DMX first in the report, so you don´t have to reread another uranium thesis, which I’m sure there are plenty of by now. However, even of you are familiar with the sector you might learn something new.

Deep dive into Mongolia Growth Group: a holding managed by a great investor

Holdings of YAK. Company reports.

The first thing you should know is that Mongolia Growth Group (YAK from now on) is not a pure play uranium firm. Approximately 40% of their portfolio according to their latest report is held as physical uranium investments. Therefore, if you are looking for 100% physical uranium, you may be better off holding the Sprott Uranium Trust or Yellowcake PLC. Both are physical uranium firms.

However, Mongolia trades at a 20% discount to net asset value. It also owns a subscription-based business: KEDM (Kuppy's Event Driven Monitor) which provides financial information for subscribers and data on especial situations like no other. This subscription revenue helps lowering down the burn rate of YAK and on some financial quarters it has delivered a profit. Also notice that the holding is managed by Harris Kupperman, a historian and investor who manages Praetorian Capital, one of the most successful hedge funds of the last years.

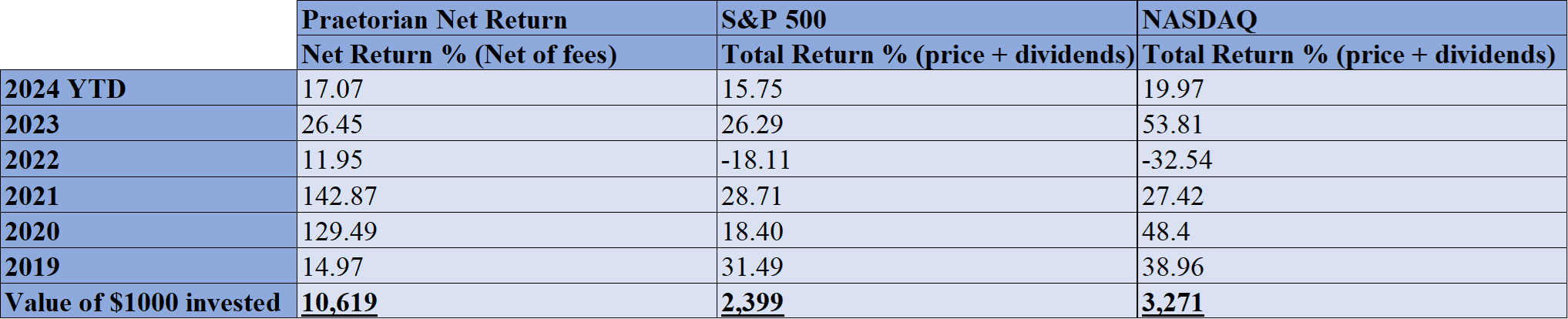

Returns of the S&P, NASDAQ 100, and Praetorian Capital.

Praetorian has delivered over a 1000% return over the almost 6 years it has been in operations. While the NASDAQ 100 and the S&P 500 do not come even close to that return. Also bear in mind that the Praetorian returns are net of fees, while if you wanted to replicate any of those indices you would have to buy an ETF, which charges you an annual fee. Therefore, by buying stock in YAK you also put the money into the hands of one of the best investors out there.

Mongolia growth group valuation. Own estimates, financial statements from YAK.

For $1.1/share you buy $1.3/share of NAV in the form of cash, physical uranium investments shares, shares in Valaris and shares in St Joe. Plus, you get top quality management, which I think should imply a premium on the valuation. YAK also has some Monero cryptocurrency but it’s a tiny fraction of its NAV.

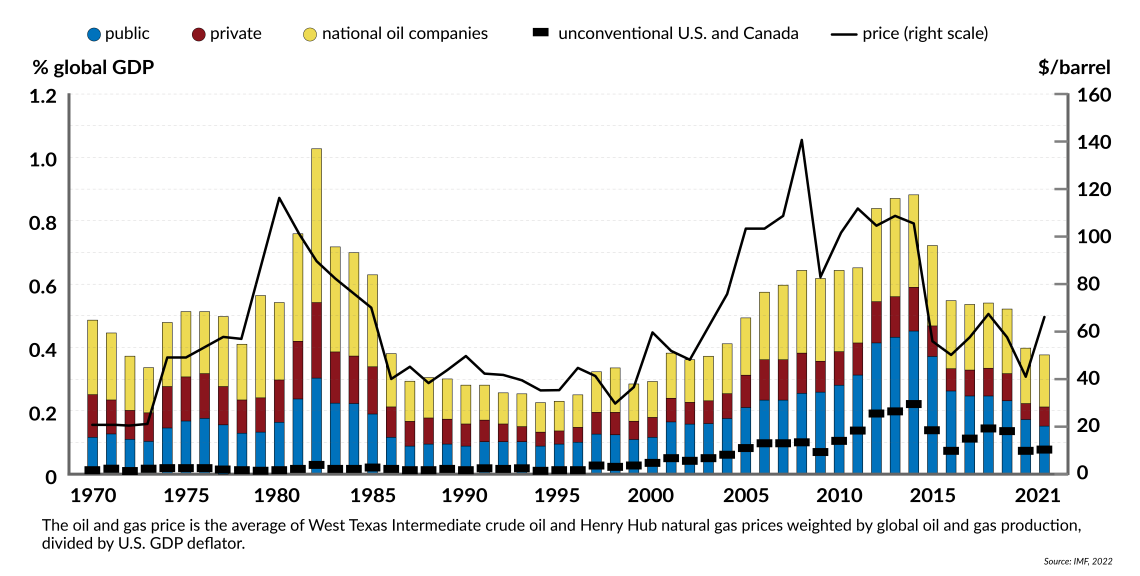

Oil and gas investment as a share of world GDP. IMF.

For those of you not familiar with this companies, Valaris is an offshore driller. It trades at a massive discount to replacement value. And it will greatly benefit from the increase in oil and gas exploration and production. Investments in oil and gas have been in decline relative to GDP, while the world is consuming more oil each year.

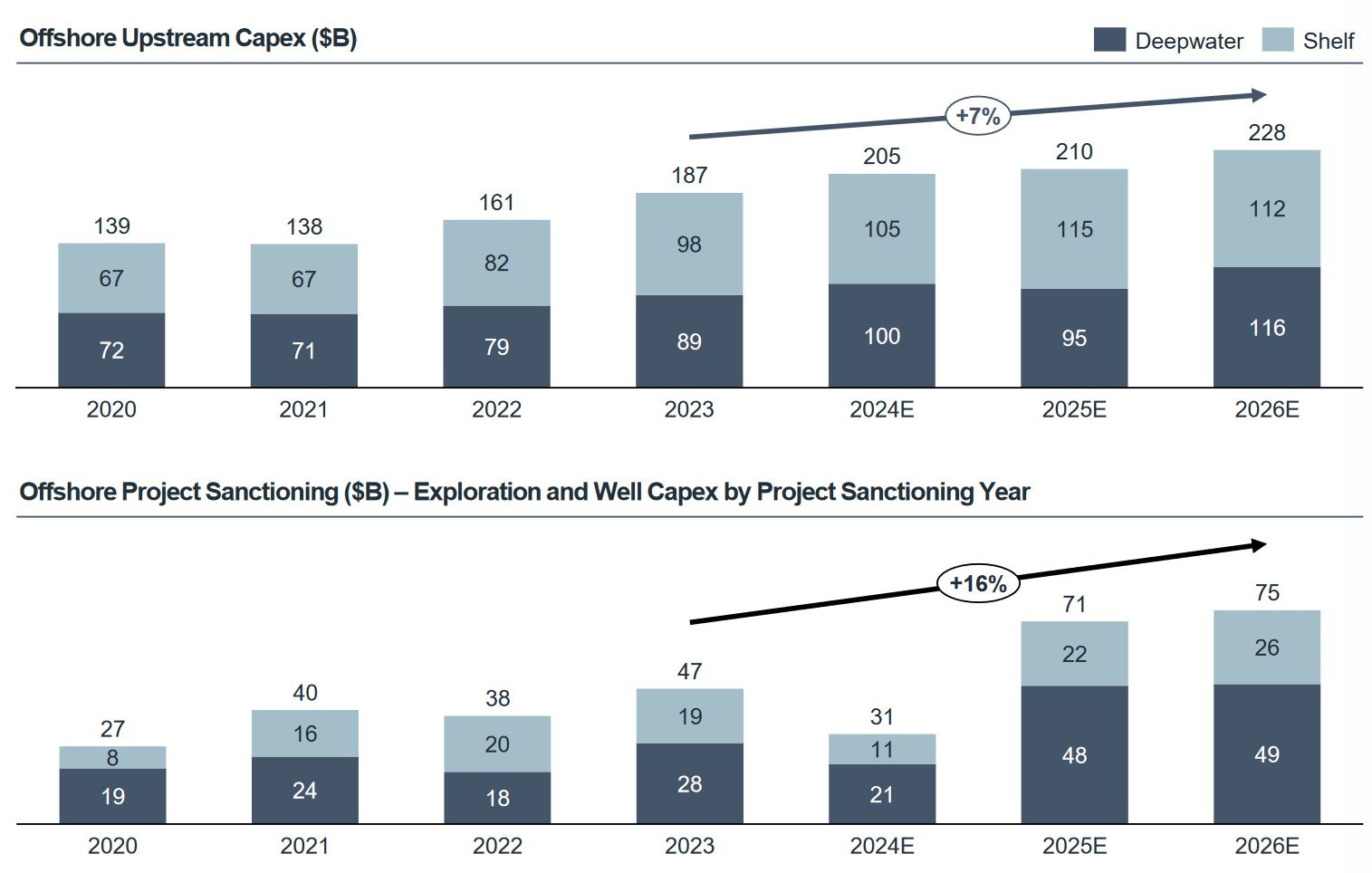

Offshore upstream capex. Valaris investor presentation.

The segment Valaris operates in is projected to increase significantly. And Valaris is the largest of its kind by number of rigs.

Regarding St Joe, I thought it best to just copy here the comment of Praetorian Capital on their last letter: ”JOE owns approximately 168,000 acres in the Florida Panhandle. It has been widely known that JOE traded for a tiny fraction of its liquidation value for years, but without a catalyst, it was always perceived to be “dead money.”

Over the past few years, the population of the Panhandle has hit a critical mass where the Panhandle now has a centre of gravity that is attracting people who want to live in one of the prettiest places in the country, with zero state income taxes and few of the problems of large cities.

The oddity of the current disdain for so-called “value investments” is that many of them are growing quite fast. I believe that JOE may grow revenue at a rapid rate for the foreseeable future, with earnings growing at a much faster clip. Meanwhile, I believe the shares trade at an attractive multiple on Adjusted Funds from Operations (AFFO), while substantial asset value is tossed in for free.

Besides the valuation, growth, and high Return on Invested Capital (ROIC) of the business, why else do I like JOE? For starters, land tends to appreciate rapidly during periods of high inflation—particularly an inflationary period where interest rates are likely to remain suppressed by the Federal Reserve. More importantly, I believe we are about to witness a massive population migration as people with means choose to flee big cities for somewhere peaceful.

I suspect that every convulsion of urban chaos and/or tax-the-rich scheming will launch JOE shares higher, and it will ultimately be seen as the way to “play” the stream of very wealthy refugees fleeing for somewhere better.”

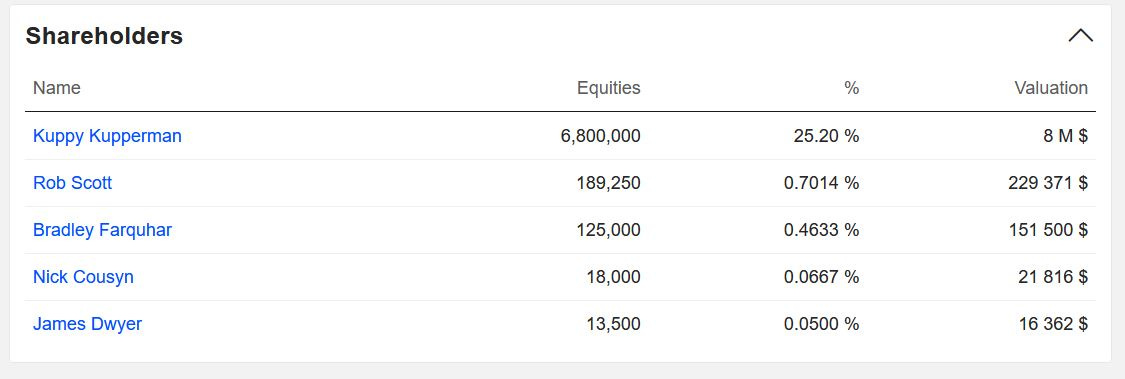

YAK ownership. Marketscreener.

Insiders own over 25% of the firm. Which I think its great since it gives them an incentive to improve shareholder returns.

Shares outstanding of YAK. TIKR.

Management has been buying back shares lately, something I think its great considering it trades at a discount to NAV.

I own YAK on my personal portfolio, and I have a very large stake in YAK through an account I manage.

Deep dive into District Metals: a play on Sweden legalizing uranium mining

Resource comparison of large uranium developers. Own estimates, company reports, economic studies.

As you can see in the table above the company has over a billion pounds of uranium as resources, albeit most of them are inferred. However, it trades at such a massive discount (in terms of uranium resources: market cap) to other firms with large nonproducing assets, that I find it a very good speculative bet. Although I must say that if I’m wrong and Sweden doesn’t legalize uranium mining, the stock will likely drop heavily. That said, District owns another 8 projects apart from Viken. Therefore, I believe there is some margin of safety with this firm.

Management owns 5% of the business.

In February 2024 Swedish Climate Minister, Romina Pourmokhtari proposed to remove the ban on uranium mining. I quote: “If the European Union is to become the first climate-neutral continent, access to sustainable metals and minerals must be ensured. We need to use the uranium we have, instead of sorting it out and considering it as waste, as is the case now – due to the current ban on mining uranium.” The country has 25% of European uranium resources. Considering the continent´s move towards self sufficiency in natural resources, I think there is a fair chance of the ban being removed.

I own shares in DMX.

Why not buy uranium miners or developers?

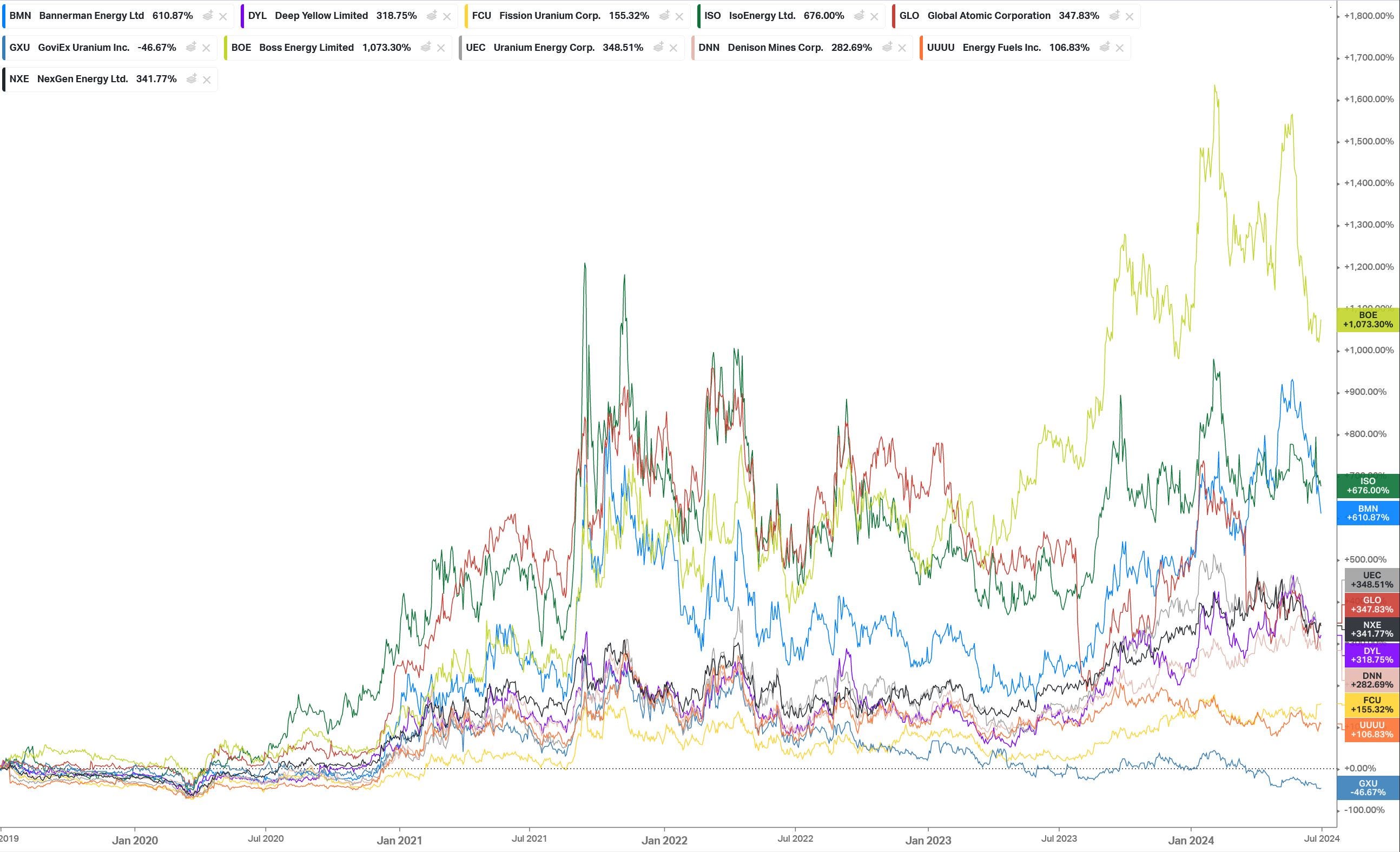

Performance of uranium developers over the past 5 years. Koyfin.

Uranium developers have had an incredible run since 2020. Many are up 1000% or 2000% from the lows of 2020. And some are now trading at small discounts to their NPV (Nexgen or Bannerman for example) and there are even firms trading multiples higher than their NPV (Boss Energy). Whereas prior to 2020 most of them were trading at massive discounts to NPV. In 2020 Vimy and Global Atomic were trading at over a 90% discount to NPV when I bought them. I believe that these valuations make no sense to me anymore in terms of risk and margin of safety. I much rather own physical uranium.

In terms of exploration the firms I like the most is Forum Energy Metals. The CEO of the company is probably the most veteran among any uranium exploration firm. However, exploration is a particularly tough business due to complex geologies, recoveries & metallurgies. In fact, uranium exploration is almost as tough as diamond deposit exploration, which is very expensive and complex. Therefore, I’m staying out of uranium exploration. I owned ALX years ago but it was one my worst performers in the bull run.

There are some firms such as Goviex that trade at significant discounts to their NPV. But due to jurisdiction risk in Niger nowadays, Goviex is not something I want to get involved with. In my opinion the most undervalued uranium junior relative to peers is Deep Yellow. Management is exceptional and they trade with a bit of discount to NPV like Nexgen or Bannerman do, but I believe having John Borshoff as a CEO should probably imply a premium, not a discount. That said, I bought Deep Yellow for AUD20 cents some years back and made almost 500% on my money, so I’m not interested in buying again at these prices.

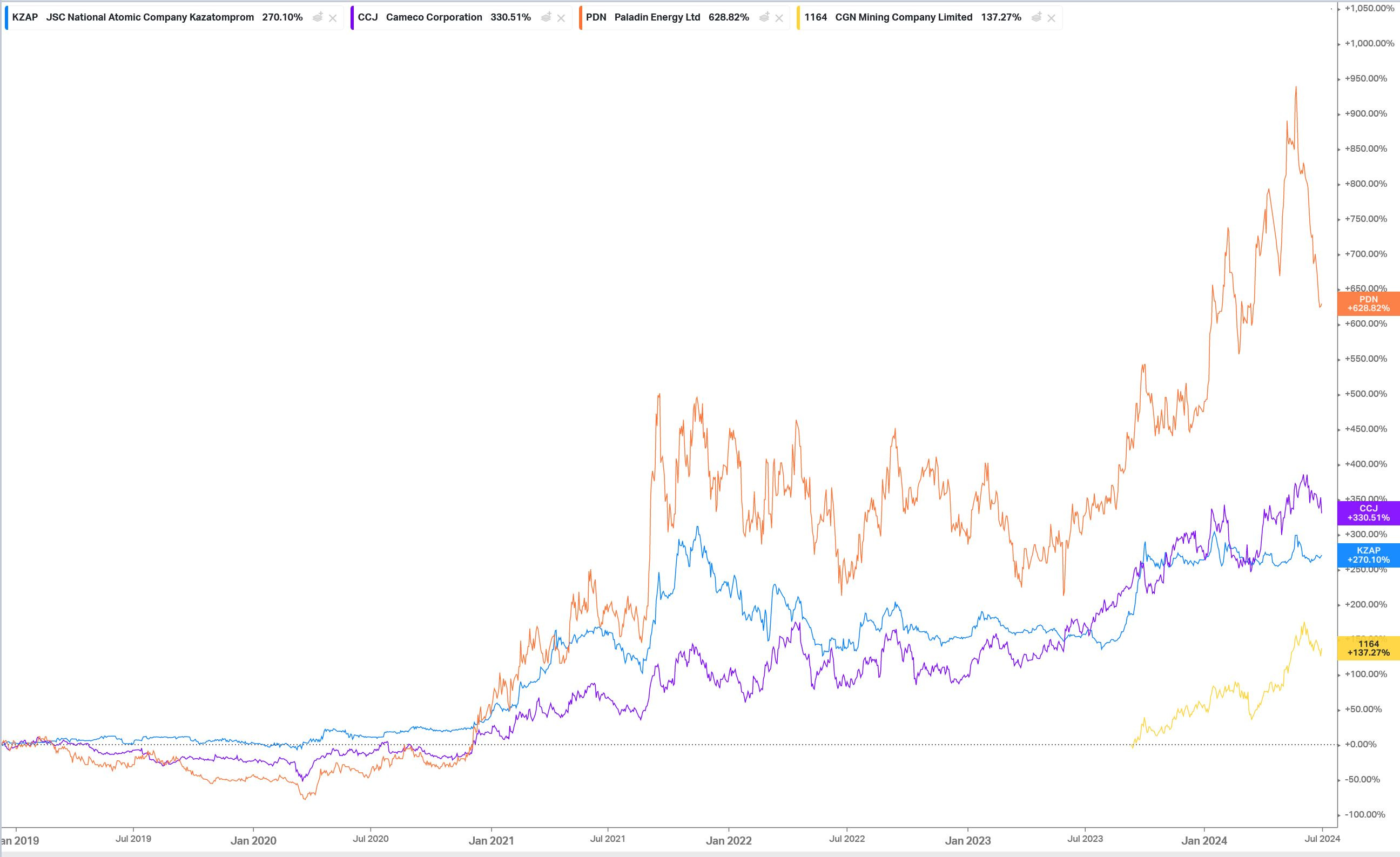

Performance of uranium miners since Kazatomprom´s IPO. Koyfin.

Same goes with uranium miners. They are all up multiple times their market cap of the lows of 2020. And I don’t think the risk that Cameco or Kazatomprom carries is worth investing in them.

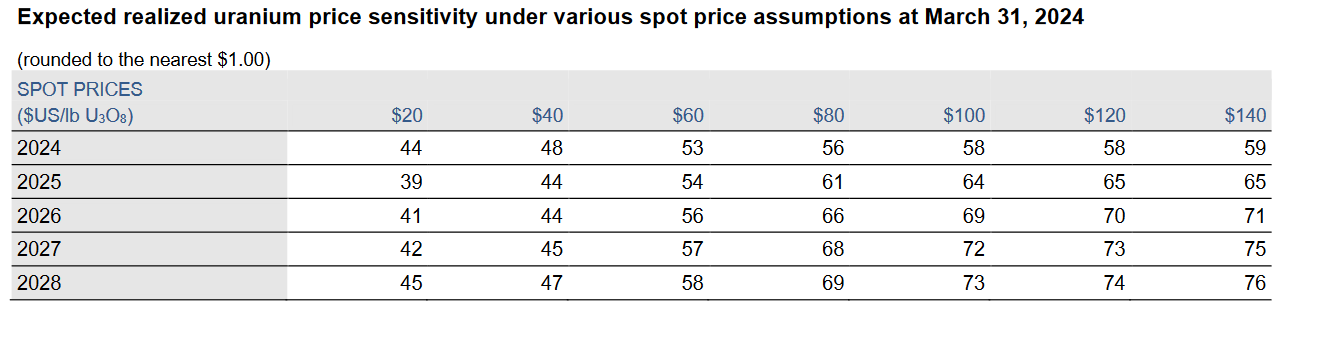

Cameco sensitivity to uranium prices. Cameco Q1 results.

Cameco has done a terrible job at profiting from the rise in uranium prices. Not only did they lose money on Q1 2024, but as you can see in the table above their leverage to uranium prices is almost nonexistent. In fact, if we had $140/lb prices by 2028, their realized price would not even reach $80/lb. Management has done a bad job.

Regarding Kazatomprom, their output, revenues and profits are down significantly in Q1 2024. Which I think is unforgivable given the higher uranium prices. In 2023 after Kazatomprom sold part of the Budenovskoye project to Russia, the firm had a massive senior management exodus. And 4 days ago, former Kazatomprom Chief Commercial Officer was arrested. This is very odd as he is a very respected figure in the nuclear and uranium industries. I doubt Kazatomprom is managed well at the moment.

Paladin recently announced the acquisition of Fission uranium. I am not sure this was the best use of FCF for Paladin, since their assets are in Africa and they have little expertise in Canada. Not to mention the Chinese government owns a portion of Fission, and I am not sure they will be happy to give it away for almost no profits. I think Paladin purchasing Lotus, Bannerman or Deep Yellow would have made more sense given their expertise in Africa.

For CGN, production in the first quarter was 10% lower than expected. This reflects the supply issues the industry continues to have despite higher prices.

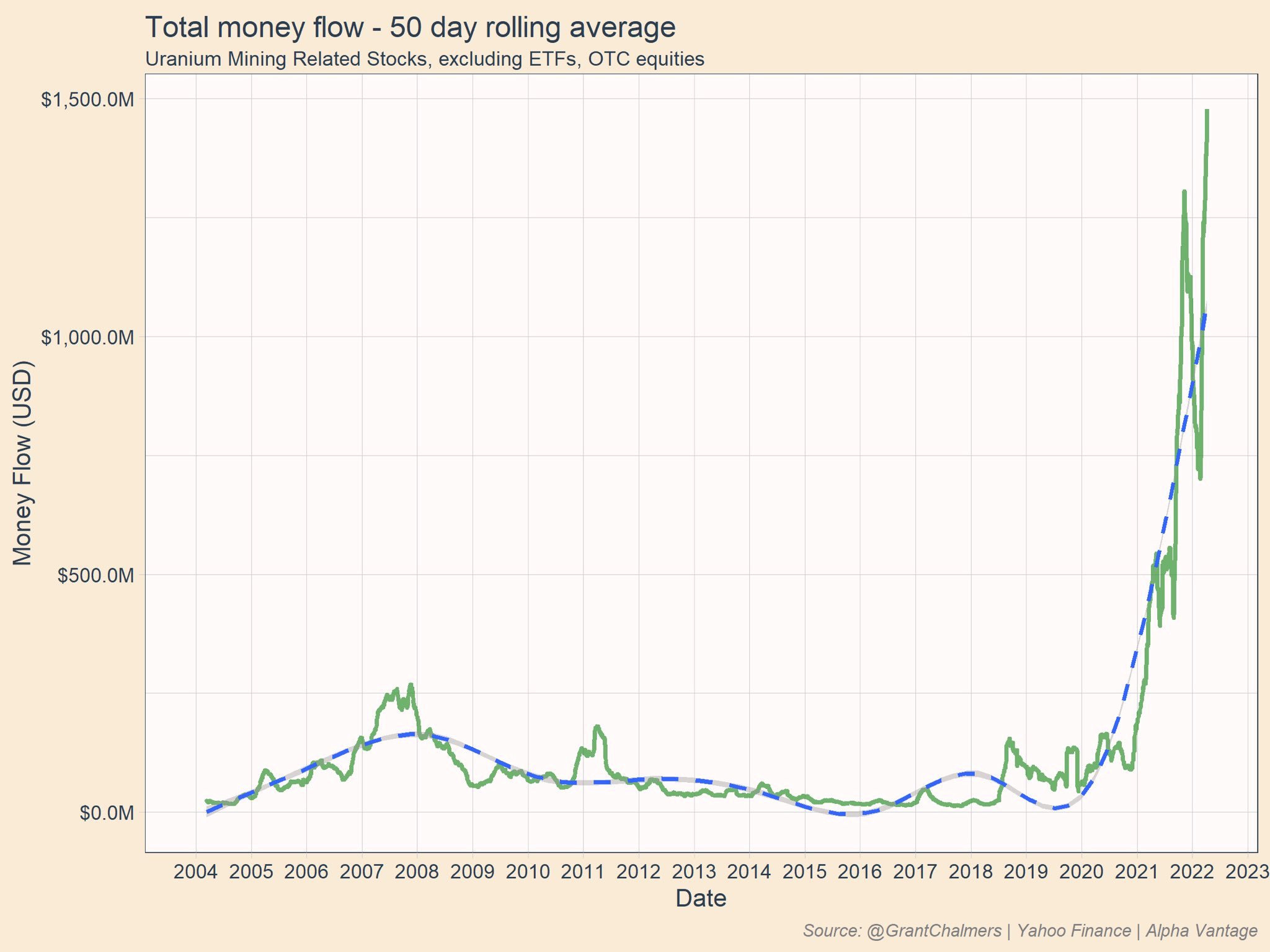

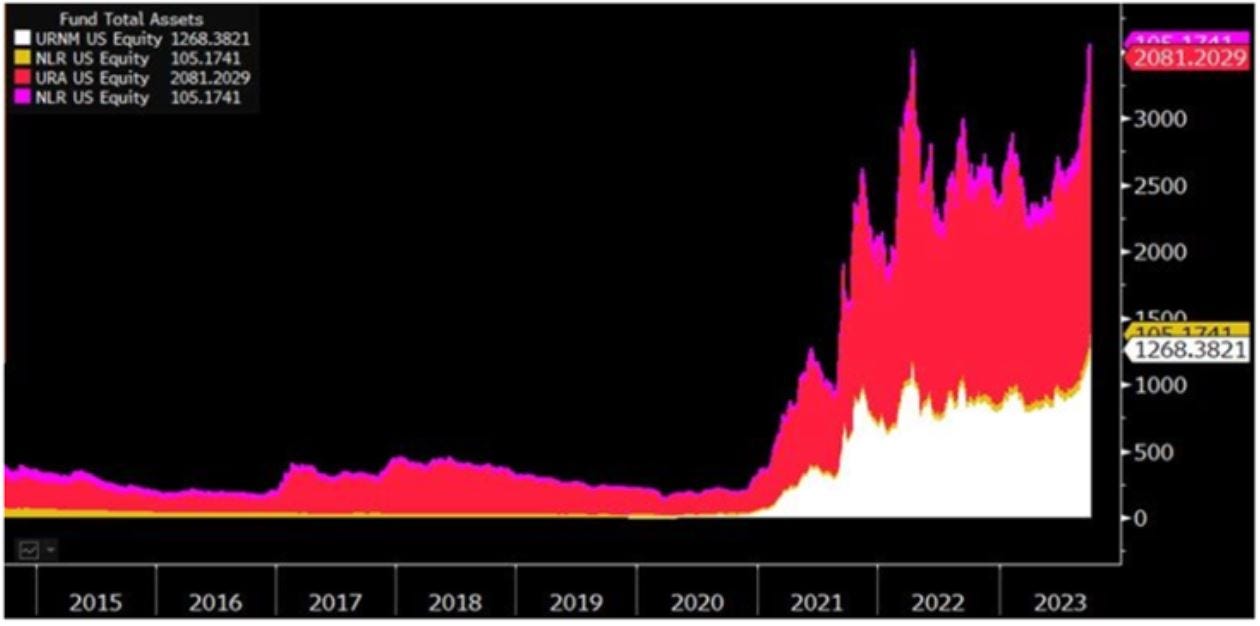

Money flows of uranium equities. @GrantChalmers

In fact, since 2020, billions of dollars have been poured into uranium equities and uranium mining ETFs as can be seen in the image above and below. This has made uranium equities larger and therefore they have now more attention from analysts. As a result of this, it has become increasingly difficult to buy uranium firms at good prices.

AUM of uranium ETFs. Bloomberg.

As a result of all this I prefer to put my money into physical uranium except for District Metals. I’m sure there are some equities that will outperform physical uranium in the coming years, but it is not clear to me which ones will be. And I don’t think its worth the risk investing in any one of them. Even if I were to diversify by investing in many uranium firms, I don’t believe I would perform better than holding the physical uranium given current firm valuations.

Nuclear Energy: The ultimate source of electricity

Uranium has a high energy density:

Uranium has the highest energy density of all fuels known today. According to the Nuclear Energy Institute, each uranium pellet (about 10 grams of weight), contains as much energy as 481 cubic meters of natural gas, 564 liters of gasoline or a ton of coal. This entails several economic benefits as will be seen later. It also implies that nuclear power plants can generate more energy using less waste than a gas or coal power plant. By example, according to the US Department of Energy, all the waste produced by all US nuclear plants over the last 60 years, would fit in a deposit of the size of a football (soccer) field 9 meters deep. And all radioactive waste generated in the life of a human being would fit in a small can of coke, assuming this human being only consumed nuclear energy. In addition, this waste can be recycled (although the US is not doing it for now). There are several nuclear reactors in development that are expected to use recycled nuclear fuel, giving place to a closed fuel cycle, which does not generate waste.

Nuclear energy is clean:

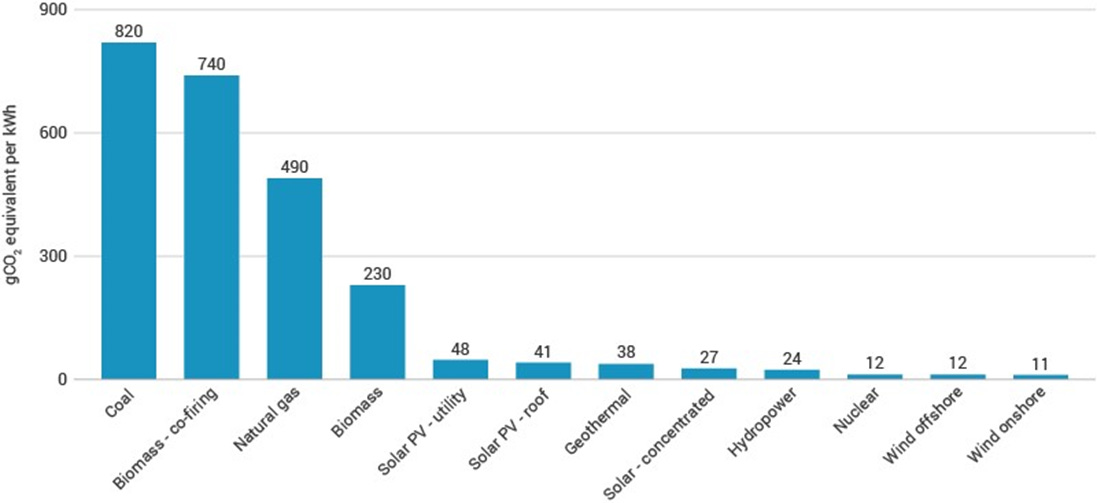

The study, done by the Intergovernmental Panel on Climate Change (IPCC), and published on the page of the World Nuclear Association, shows the generation of CO2 per kWh of electricity produced. As it can be seen on the table below, the only less polluting energy source than nuclear is wind energy. But it is important to mention that CO2 emissions of nuclear energy they do not come from the electric production itself. Emissions come from the production of cement, steel and components that are used to build nuclear plants. This is the main advantage of the nuclear energy since it is the only baseload energy source that does not generate any emissions.

Emissions gCO2/kWh. WNA.

A very safe source of energy:

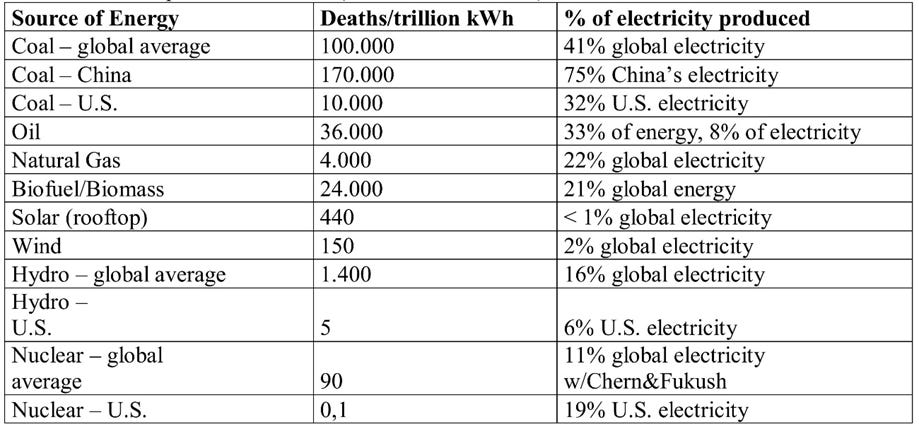

The data below represent deaths related to different types of electricity generation. These deaths can be caused due to the emission of CO2, to accidents during the operation or construction of the infrastructure, to accidents related to mining necessary to obtain materials for building the energy infrastructure, or to produce the fuel used in them. For example, according to Reuters, in China an average of seven people die in coal mines every day, this increases the death toll/kWh of coal. Regarding global nuclear energy data, the figure of 90 deaths per billion kWh includes the Chernobyl and Fukushima accidents. Therefore, it is only surpassed by the generation of hydro and nuclear energy in the USA, which suffered 90 and 0.1 deaths/trillion kWh respectively. This shows that nuclear energy is safer than most other sources of electricity. In global terms, nuclear is the electrical source with fewer deaths per kWh. Furthermore, contrary to popular belief today, a nuclear reactor cannot cause a nuclear explosion. The concentration of uranium in the reactors is not high enough to cause a nuclear explosion. The uranium in a reactor is enriched to 5%, while a nuclear warhead is enriched to more than 90%.

Deaths/trillion kWh for each source of electricity. Forbes, WHO.

The explosion of one of the reactors at Chernobyl exploded due to a design flaw, not due to nuclear energy itself. In fact, the explosion was due to an accumulation of gases in the reactor, not to an explosion due to a nuclear chain reaction. And the death of people following Chernobyl was mainly due to the incompetence of the Soviet regime which did not want to admit its own fault and did not evacuate the area in time.

In the Fukushima accident of 2011, no one died due to the reactors failing. The only person that died in that regard was in 2018, when a worker tried to measure radiation inside and later died of lung cancer.

Nuclear is a reliable energy source (it has a high-capacity factor):

The capacity factor is the coefficient between the energy generated by a power plant for a period (usually a year), and the capacity to generate energy from that plant (the energy produced if it had worked at full capacity in that period).

US Capacity Factor. Office of Nuclear Energy.

As can be seen in the table above, nuclear energy has the highest capacity factor. This implies, that there are no energy sources that can take as much advantage of all their potential energy output, as nuclear does. This is especially relevant when compared to hydraulic, coal, gas, or geothermal energy because although they are all baseload energy sources (they generate energy continuously, unlike solar or wind), only nuclear can generate energy continuously for the potential output it was installed for. This implies that nuclear energy is the most reliable source of electricity, because it can generate energy at any time and practically in any circumstance.

Nuclear also produces energy 24 hours a day, almost every day of the year. Therefore, its critical for modern infrastructure to be able to run all day long, Infrastructure like data centers, hospitals, traffic lights, electric cars/trucks, or electrical trains (to name a few) all need power at any given time. As a result of this, both in the short term and in the long term, the world needs energy all day long, and batteries are too far behind (and expensive) to enable solar or wind to achieve this. Nuclear is deployable anywhere, unlike geothermal or hydroelectric power. Albeit the last two can produce energy all year, every day, they can only be constructed in very specific locations.

Nuclear energy requires less surface area than other energy sources:

According to the Nuclear Energy Institute, a 1,000-megawatt nuclear power plant has a surface area of approximately 2,589,988 square meters (1 square mile). To put this into perspective, a wind farm of the same capacity has a surface area 360 times larger (about 900,000,000 m2) with 430 turbines. A photovoltaic solar farm requires 75 times more space (about 187,500,000 m2) with 3 million panels solar. This means that nuclear energy generation has a smaller environmental footprint, because it requires razing less land to build, and it also requires less materials for its construction, and therefore it is a process that pollutes less.

Comparison of different of largest power plants and infrastructures of each type. Own estimates, Energy Information Agency.

The most important column is the one on the right (Ratio output: area), which shows the production in MW per square km. The nuclear plant generates 1896 MW/Km2, while solar, wind, hydraulic or geothermal technology all generate 40 MW/Km2 or less. This implies that nuclear energy is more than 40 times more efficient in the use of space than other low-polluting electrical sources.

The cost of fuel is low for the operator of a nuclear power plant:

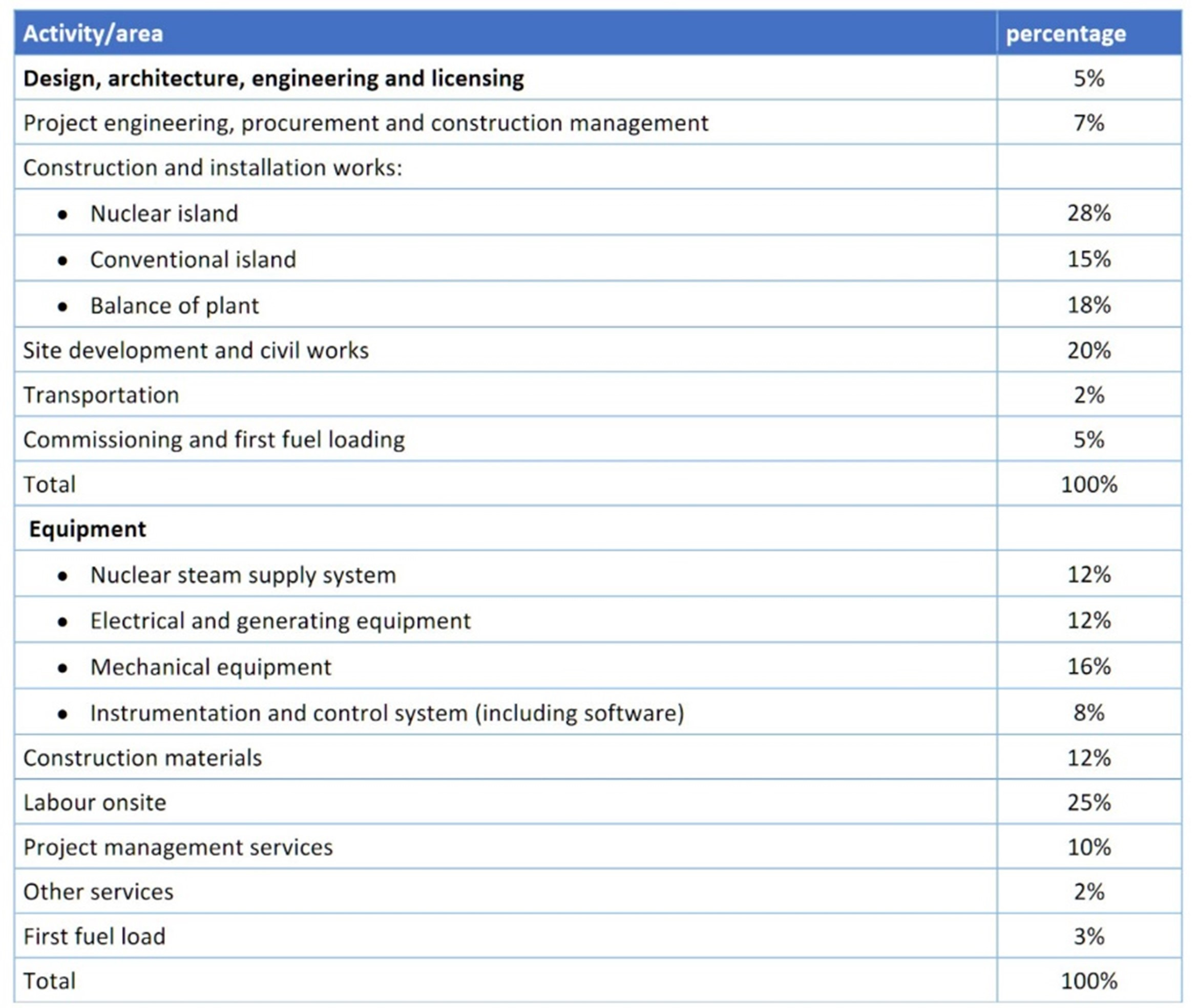

Relative (%) costs for the construction of a nuclear power plant. Rijksoverheid/Government of the Netherlands.

As the penultimate row of the table shows, the first shipment of fuel Nuclear is equivalent to 3% of total costs. In a gas or coal plant that cost can be between 30% and 50% depending on the technology used. Therefore, nuclear power plant operators are much less dependent on the price of the raw material than the operators of a gas or coal plant. This too causes nuclear operators to be less sensitive to the price of uranium and, therefore, they are willing to buy it even if the price skyrockets.

A low cost of energy:

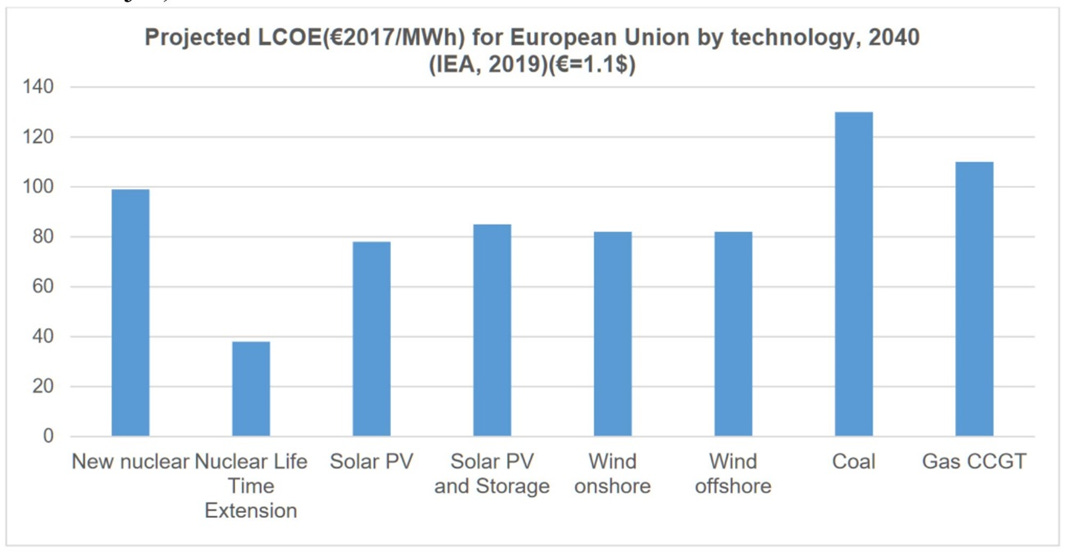

The levelized cost of energy (LCOE) is a measure represents the cost of electricity generation of a plant during its useful life. The LCOE formula is as follows: LCOE= sum of all costs during the useful life of the plant/ sum of the value of the electricity produced during it´s useful life.

LCOE for different electricity sources. Rijksoverheid/Government of the Netherlands.

The higher the LCOE, the less profitable a technology is. As the table above shows, it is expected that in the future nuclear energy will be the most cost-efficient technology of all the base energies analyzed (gas, coal and nuclear). And the extension of current nuclear plants is multiples times less costly than the other sources of energy.

Nuclear power plants are less dependent on fuel prices than other energy sources:

Costs of operating different electricity plants, % of the total cost. Energy Information Agency.

As can be seen on the left-hand side of the table above, fuel costs of a nuclear power plant are a fraction of the costs of coal or gas. On the right-hand side of the table, you can see the operating costs of different energy sources (operational and maintenance costs). Nuclear fuel costs are a smaller proportion of its total costs than those of other energy sources. This implies that nuclear power plant operators are less vulnerable to price increases of uranium.

Furthermore, uranium costs are only one third (approximately) of the total costs of nuclear fuel, because the rest of the costs are due to enrichment, conversion, or reconversion of uranium. Therefore, the price of uranium can rise significantly without affecting nuclear energy production. Not only because of the low fuel costs, but also because there is no substitute for uranium. Utilities invest billions of dollars in the construction of nuclear plants and closing them would imply an enormous sunk cost. Therefore, closing nuclear power plants is not a viable economic option for utilities. This greatly favors uranium producers because it makes consumption inelastic to the price (the price can rise a lot without affecting uranium consumption).

Structure of the uranium market

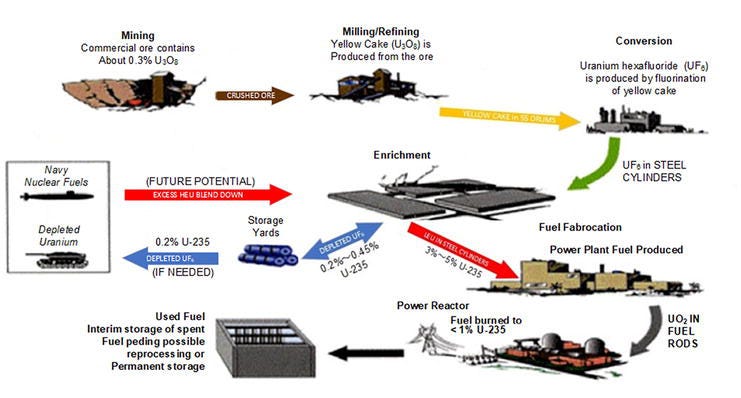

A nuclear power plant is usually made up of several reactors. Each reactor carries out a fission process, which involves “splitting” the nucleus of the uranium atom. When uranium atoms split, neutrons are ejected from the fission and they impact other atoms, causing their fission. The result of this is a process called nuclear chain reaction, which generates enormous amounts of energy. For fission it is necessary to have uranium, specifically the isotope 235, which is the only known isotope of uranium that is known to fission, causing a chain reaction. The isotope 235 accounts for only 0.7% of all the uranium on Earth. Uranium238 makes up most of the uranium, but it is not fissile.

As table below shows, the uranium mining process begins in the mine. The purity of the ore can vary from less than 0.01% to over 20%. This ore is transported to a refining mill that removes all the uranium oxide from the rock, removing impurities. This uranium oxide, also known as “yellow cake”, due to its yellowish appearance, is transported to a central processing plant for conversion. The conversion centres turn this uranium oxide into uranium hexafluoride, which although in its natural state is gaseous, it can be liquefied for subsequent transport to enrichment. In the enrichment plant the isotope uranium 235 is separated from non-fissile isotopes. Enrichment plants can produce uranium for nuclear power plants, for nuclear weapons, for medical purposes or transport fuel (submarines mainly, although ships can also be fuelled with uranium).

A nuclear power plant consumes uranium enriched with 3%-5% uranium235 and this requires an intense and expensive enrichment process. However, nuclear weapons contain more than 90% uranium235. It is usually thought that with the same installations both concentrations of uranium235 can be achieved. But the reality is that achieving 90% of uranium235 requires much more infrastructure and costs, therefore the risk of non-proliferation by enrichment plants is overrated. A conventional enrichment plant cannot create uranium with sufficient purity for atomic weapons.

The waste resulting from the enrichment process has some uses. Some is used for anti-tank projectiles and for tank armour. This is because depleted uranium (depleted because it has little uranium235) has a very high density, making it ideal for armour and projectiles. This uranium is also used for medical purposes, specifically it is widely used in radiology and oncology for the detection of some types of cancer. Unused depleted uranium is stored in special warehouses.

The uranium with 5% uranium235 is then transported from the enrichment plant to the fuel factory. There the uranium is converted into small pellets, which are transported to nuclear power plants for use. They usually change fuel once a year, although for new plants they usually put fuel in them for two years. Once the plant has consumed the uranium, the waste is transported to a definitive warehouse to remain there for all its radioactive life. Waste that is not stored is usually used for recycling, to extract useful waste or uranium 235 that may have remained from the process of fission.

Uranium production process. Office of Nuclear Energy.

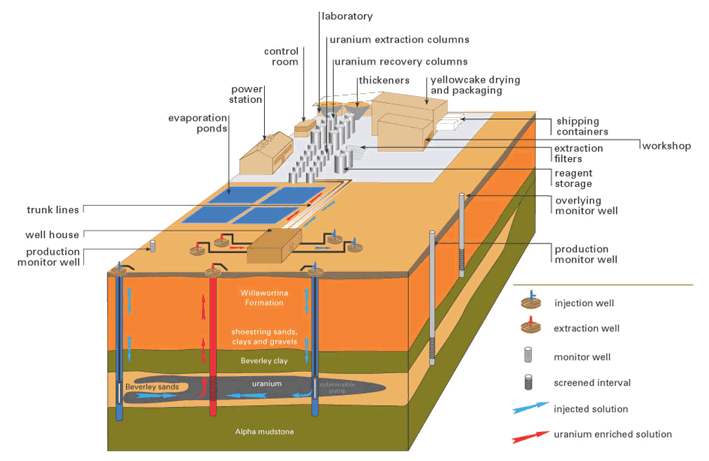

Uranium mining can occur with three different methods: open pit mining, underground mining or in situ mining (ISL/ISR). The kind of method of exploitation of the mine depends on its geology and the laws that govern the country where the mine is located. Open pit uranium mines are the most common in Africa, although Orano, in its Cominak mine in Niger, uses underground mining. This last technique (underground) is the most common in Canada and in Australia. In situ mining is the most profitable of all techniques because it is the one that employs the least capital. This mining method is the most common in Kazakhstan and in the United States, although in Australia the Honeymoon mine, operated by Boss Energy uses in situ mining. In Canada they are now trying to implement the in-situ technique. But implementation has been very slow so far because mining permits are only provided for underground, or open pit mining, and there are concerns about possible groundwater contamination. Specifically, Denison, in Canada, is trying to use in-situ mining at one of its deposits in the Athabasca basin. All Kazatomprom mines use this method (ISR).

In situ uranium mining. Energy Information Agency.

In situ mining, as shown in the table above, consists of injecting into the subsoil a mixture of water with an alkaline or acidic substance (depending on the geology of the deposit). The liquid dissolves the uranium in the subsurface. The liquid is then drawn with a fountain and sent through tubes to the treatment centre to extract from the liquid all the uranium. The uranium is converted to uranium oxide for subsequent distribution to customers or conversion plants.

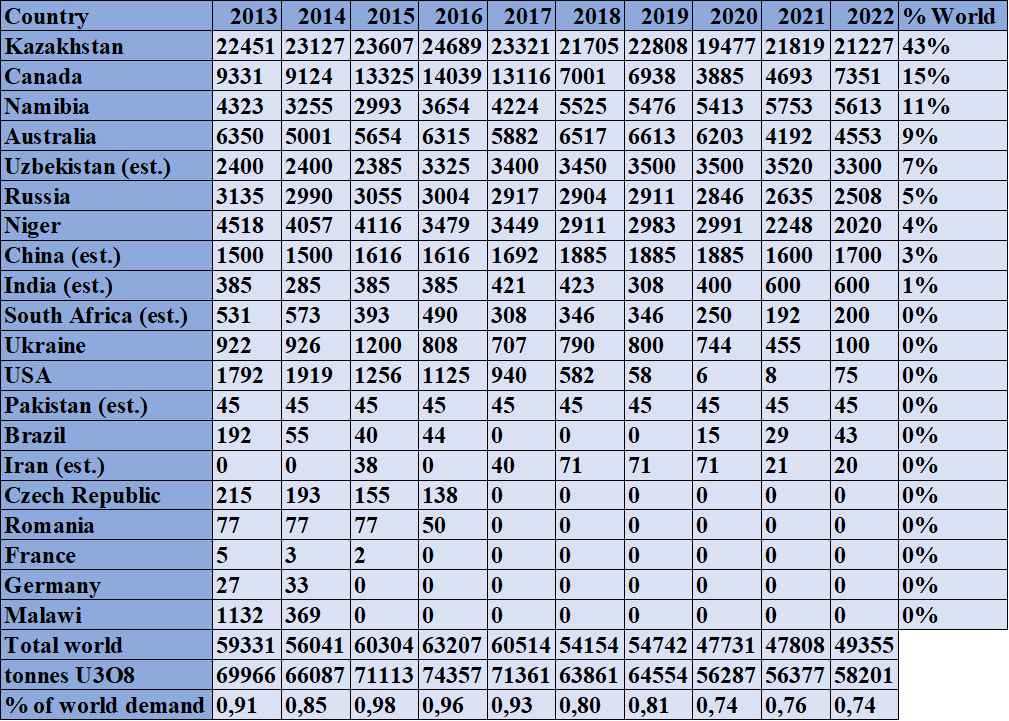

Uranium production by country. world-nuclear.org.

As can be seen from tables below and above, the uranium market is an oligopoly, because the industry is dominated by a few players: Kazatomprom (owned by the Kazakh government), Cameco, Uranium One (owned by the Russian government, just like ARMZ), Orano (owned by the French government) and CGN (owned by the Chinese government just like CNNC). These five players control 77% of the global production of uranium oxide (U3O8). Furthermore, they compete in a market of homogeneous product: uranium, and they have high entry barriers. All these features are very common in oligopolies.

Until 2020, Canada was the second country in uranium production. Not only that, but Canada also has 9% of the mineral reserves of uranium in the world. Most of these reserves are in the basin of the Athabasca, one of the most successful uranium mining regions in the world. Some investors call this region the “Saudi Arabia” of uranium due to the enormous purity of its uranium deposits, which have up to 20% uranium oxide in their ore. To put it in perspective, the purity of the uranium deposits in Namibia or in Niger is usually 0.01% or lower. However, in Canada the bureaucratic processes for the construction of a mine last until a point in which the investment becomes unprofitable. To illustrate with an example, the McArthur River mine owned by Cameco, the largest uranium firm in the world for years, took 11 years to approve all the procedures and constructing it. But the Cigar Lake mine, the highest purity mine in uranium in the world, also from Cameco, took 33 years to be permitted and built, 1981 until 2014.

Furthermore, the Athabasca basin has a difficult topography. It is covered with lakes which makes it difficult to drill and operate. For context, Saskatchewan, the province in which Athabasca is located has over 90,000 lakes. To put this into perspective, the entire continent of Africa has 677 lakes. Canada has more lakes than the rest of the world combined. This makes it difficult for exploration firms to find economic deposits. In fact, a lot of the drilling happens in winter, under freezing conditions because for the rest of the year the ore deposits are covered with water. Fission Uranium (FCU) for example, has a very high grade and shallow deposit in the Athabasca, but is covered by a lake, which has complicated their economics and logistics. Also, a lot of the deposits in Athabasca are covered by sandstone. In some cases, like the MacArthur River or Cigar Lake mines, they are under hundreds of meters of sandstone and overburden. Which makes the operating of the mines very complex.

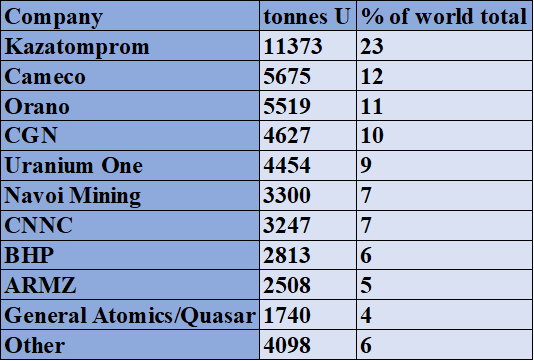

Uranium production by firm. 2022. world-nuclear.org.

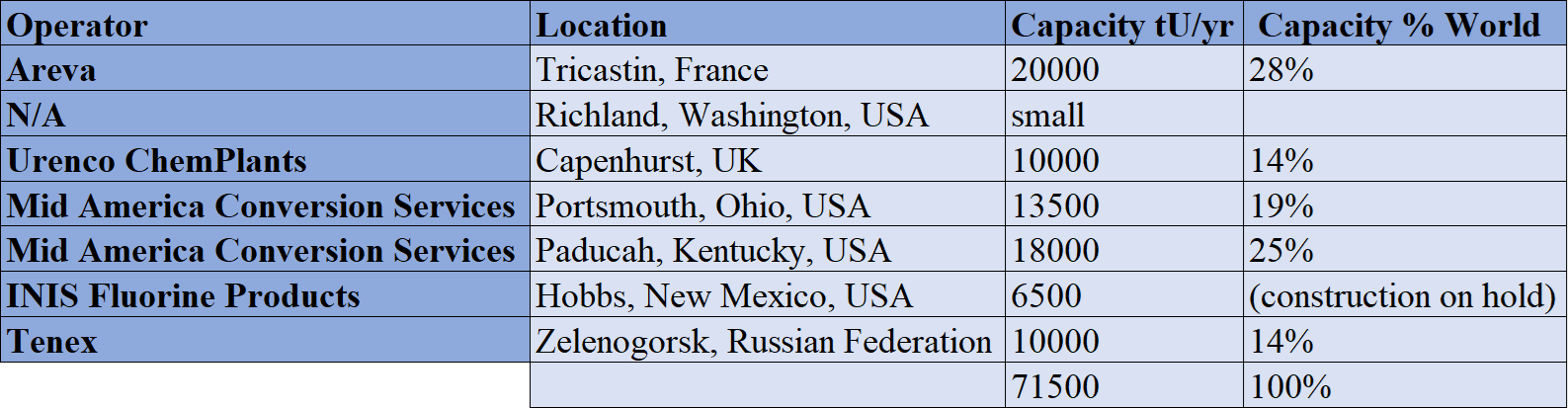

Market concentration is more intense when other phases of the fuel manufacturing process are investigated. For example, to transport uranium from a mine to a power plant, it is necessary to “convert” yellow cake into uranium hexafluoride (UF6), a process that takes place in a conversion centre. There are only eight conversion centres worldwide. But most of the capacity is in Russia, United States, Canada, and France. The Converdyn conversion plant in the United States closed in 2017 due to the bear market that the uranium market has experienced. However, following the uranium rise in 2020 and 2021, the company decided to reopen the plant in 2023.

As seen in table below, the global conversion capacity depends 22% on Rosatom, in Russia. This has caused conversion prices to go from about $10/KgU in 2021 to around $40/KgU by the end of 2023 due to the Ukraine conflict. Utilities don´t want to depend anymore on Russian conversion facilities in case Western countries sanction Russian uranium. In fact, a ban on Russian uranium from the US government seems imminent, therefore this will exacerbate the problem.

Uranium conversion capacity in the world, 2024. wise-uranium.org

The market concentration is even higher in deconversion plants (Deconversion of depleted UF6 to uranium oxide or UF4 is undertaken for long-term storage of depleted uranium, in more stable form). There are only 7 of these facilities in the world, which are in 4 countries: USA, Russia, UK, and France. In this case the dependence on Russia is 14%.

Uranium deconversion capacity in the world, 2022. WNA.

Deconversion plants are responsible for converting depleted uranium or uranium without 235U, in uranium tetrafluoride, a form of uranium that is easier to store and preserve over time. In this case the dependence on Russia is less than 14%.

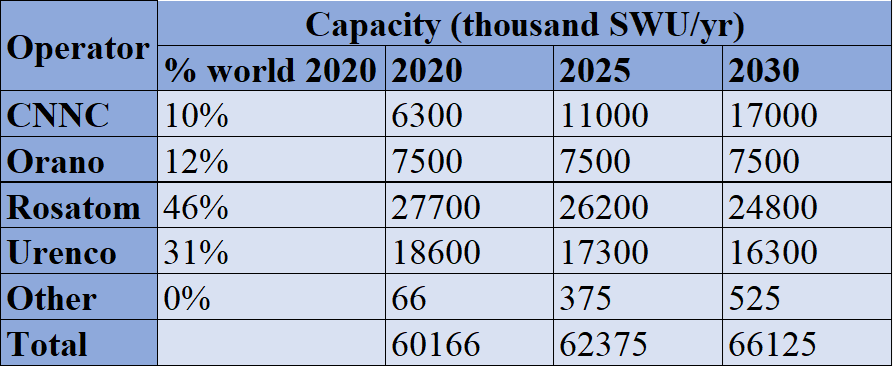

The table below shows the enrichment capacity. It is measured in Separative Work Units (SWU). The enrichment capacity of the world has increased since 2013 from 51,550 SWU/year to 60,166 SWU/year in 2020. The world's dependence on Russia in this aspect is enormous, in 2020 Russia accounted for 46% of the enrichment capacity of the world. Therefore, the invasion of Ukraine has had a huge impact on the sector. SWU prices have gone from $60/SWU at the end of 2021 to almost $160/SWU at the end of 2023. The dependence problem will only get worse as China will almost triple capacity by 2030, while Urenco (UK) will lower capacity.

Uranium enrichment capacity in the world, SWU/year, 2020 and planned. WNA.

Reasons why uranium has remained below $45-50/pound for so long (AISC of the world):

One of the fundamental causes of the current and future shortage of uranium is that the price has been below the cost of production for a decade. Therefore, it is worth examining the causes of this situation that has lasted since almost 2009 until the 2021.

Bad publicity for nuclear energy and uranium:

Since the Chernobyl accident and more particularly since the Fukushima accident (which only had one fatality due to radiation), the nuclear industry has had a bad reputation.

This image of a dangerous and polluting energy has been publicized by NGOs such as Greenpeace that have not considered the result of their policies: the over dependence on gas and coal, which pollute a lot and have caused geopolitical problems in Europe. Regarding uranium mining, it is considered a dangerous activity and very polluting but that is not the reality. The uranium contained in mines does not pose a health risk, even in high concentrations. In the Cameco mines the concentration of uranium oxide sometimes reaches 20%, and its workers do not need any type of special protection that a copper or gold mine does not have.

Regarding pollution, thanks to the mineral purity of the mines of uranium (0.01%-20%), the use of acids and solvents to extract uranium is less than in the gold industry. For example, miners extract gold from the ground in concentrations of 0.5-1 g/t gold. The lower the purity, the more chemicals and processes must be used, that implies more cost and pollution. Not to mention the strict safety rules followed in uranium mines, and there is rarely an accident. In coal mines however, worker deaths are frequent, particularly in China.

The short-term minded electricity companies are still in the market, the long-term ones are not:

European, American, and Canadian utility companies tend to contract their uranium 2-5 years in advance. They do this because they prefer to strictly adhere to the law, which in many countries dictate that electricity companies must have at least 2 years of uranium to consumption of its reactors. The Japanese electricity companies, however, are known to contract their uranium 20 years in advance or even with more time. The departure of Japanese companies from the market and of Rio Tinto, which had been in business for decades, has meant a paradigm shift in the sector.

Considering it takes between 5 and 30 years to build a uranium mine, the utilities aren’t being sensible in their uranium purchases. This gap between the term of the contracts and the time of construction of the mines has been one of reasons responsible for the destruction of supply of the last 9 years. This behaviour on behalf of utilities has caused downward pressure on the price of uranium, because customers were no longer planning decades in advance, but with a few years.

The uranium pricing system is highly inefficient:

There are two markets for uranium: the spot market and the long term contract market.

Per Jander of WMC, the Technical Advisor to Sprott Physical Uranium Trust, when asked about the uranium spot market he said: “But there's not necessarily a transaction every day [in the spot market]. Most of the time, there are a few. You have a few price points, but reporting is on a voluntary basis. You have a few price reporters who objectively collect this information and then publish a price at the end of the day. It’s very hard to get an intraday price.” This involves an important information asymmetry between those who are present in the spot auction and the rest of the market. This hurts the market because it is not receiving information on the true price of uranium.

The other pricing mechanism (long-term contracts) is also ineffective in revealing the true price of uranium. This is because long-term contracts are negotiated and signed privately, between the uranium miner and the electric company. These contracts are not usually published to the public. And it is almost never known which electric company is the one that has signed the contract, nor its price. A good example is Global Atomic, a Canadian company developing the Dasa project in Niger. Global Atomic has signed a contract for the future sale of uranium with a utility company setting a floor and a ceiling for the contract price. But the company has not been able to publish even the name of the electric company, neither the floor nor the ceiling of the price. This implies an opacity that means that the uranium price is difficult to determine.

In fact, the long-term price of uranium that appears published on various websites, is an estimate that consulting companies, like UxC or TradeTech do. But it is still an estimate, because UxC and TradeTech do not have access to many of the long-term contracts that are being signed.

Ludwig von Mises wrote: “Without a price mechanism, there can be no economic calculation.”

This is the problem that this poses for uranium producers. Due to the inefficiency in the price mechanisms, they cannot react rationally to the price because it is distorted due to lack of information.

The miners won't/can't stop producing:

Although for nearly a decade the average uranium producer has not been making money, uranium production reached its peak in 2016. This is even though since 2009 the uranium price had only risen above $50/pound one year. In fact, 2016 saw the price hit a decade low of $18/pound. This reluctance on the part of the miners to reduce production has led to a prolonged oversupply in the market. And has put downward pressure on the uranium price.

The fundamental reason why the miners did not want to shut down output despite losing money, is that they preferred to continue paying their debt and employee salaries (only part of the salary in some companies). All this while they would finance the losses by issuing shares and diluting the shareholder. It has also been the case that long-term contracts signed before Fukushima were generating some free cash flow to the miners. But as these contracts expired, miners had to renegotiate at lower prices.

Kazatomprom, the real Saudi Aramco of uranium:

Kazatomprom, the uranium miner owned by the Kazakh government was created in 1997. Back then their market share of the uranium market was around 2.5%. By 2014 it had skyrocketed to over 40%. Given that their costs are the lowest among its peers and the size of the reserves that Kazakhstan has, their role in keeping the uranium price low is not something that we should ignore. Kazatomprom has made money all through the cycle and therefore their production has not been hit. However, their uranium output was down 10% in the first report released in 2024. And their logistics are getting difficult as they can´t export their uranium for Western customers through Russian ports after the sanctions placed after 2022 on Russia.

Uranium investment thesis

As has been analysed so far, uranium serves as fuel for the nuclear industry, which generates clean energy all year around, something the world needs. Uranium fuels operations of some 440 reactors, which produce 10% of the world's energy. And there are 60 reactors under construction, with another 110 already planned and another 300 reactors that are proposed.

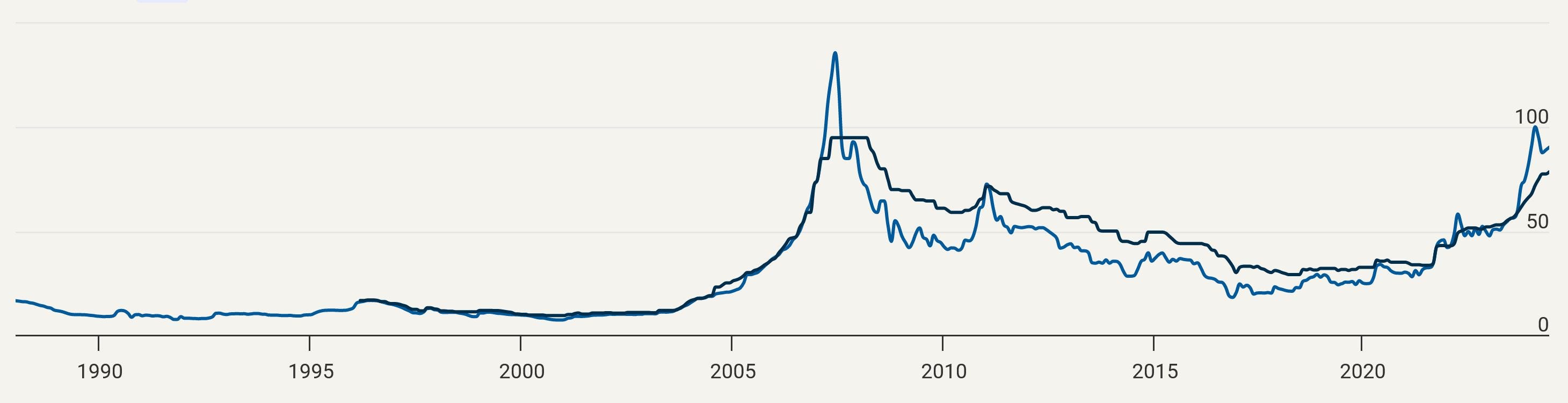

However, only one significant uranium mine has been opened outside of Kazakhstan in the last 10 years. The reason is that the average cost of production of uranium worldwide is around $45/pound, the EIA even mentions that in countries like the US, the average cost of production is $67/pound. And as shown in the table below, the price of uranium has been below $45 since mid-2012 until a few years ago. The fact that uranium has been below its production cost for 9 years in a row has led to destruction very important production capacity. In fact, uranium production is at its lowest since at least 2013.

Price of uranium (USD/lb). Spot (blue line), long term contracts (black line). UxC, TradeTech, Cameco.

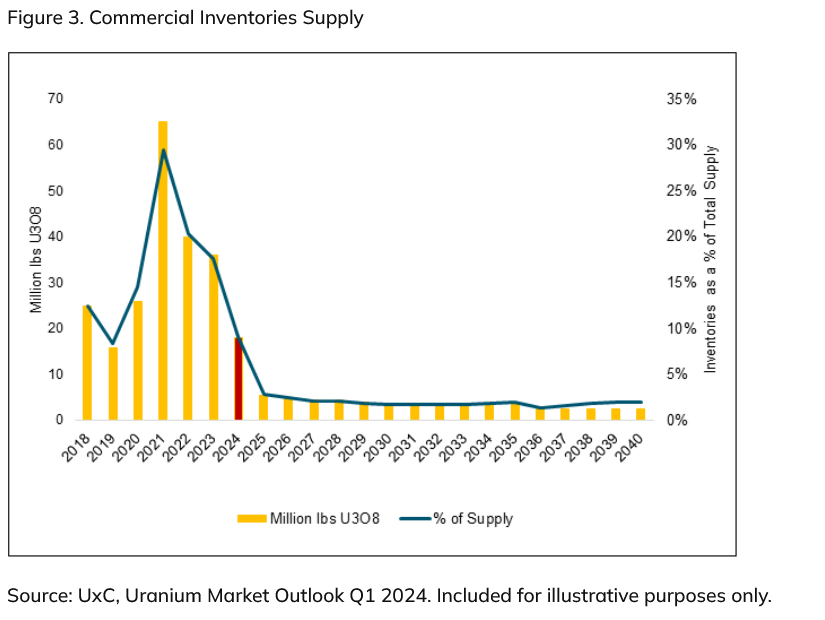

Uranium inventories in millions of pounds of U3O8. UxC.

Mines are only producing 74% of the global demand for uranium, this has only been possible thanks to the consumption of inventories. Another source of uranium has been the program between the US and Russia called Megatons to Megawatts, which was dedicated to convert Russian nuclear warheads (with concentrations of around 80% uranium235) into uranium for civil consumption (with 3-5% uranium235). This program generated important quantities of uranium for electricity companies, but it ended in 2013.

However, there is uranium that comes from the so-called secondary supply, this supply comes primarily from nuclear fuel recycling and tailings re-enrichment (recycling of uranium mine waste). However, this last source is increasingly less important because it is a very expensive process and requires waste from uranium mines, whose production is in decline. It is especially relevant that the electric companies have very low uranium in their inventory, because these are the ones that generate a large part of the uranium consumption through long-term contracts (5, 10, 15 or more years in advance) with uranium producers.

These contracts are essential for the proper functioning of this industry. This is because building a uranium mine often requires hundreds or billions of dollars, and 5 to 30 years of permitting and construction, depending on the type of mine and which country it is located in. It is worth mentioning that in this industry the margin of error is very small, because an electric company cannot afford to run out of uranium, this is due to several reasons: To begin with, there is no substitute that utilities can use instead of uranium and therefore if they run out of uranium, they cannot operate their plant. Furthermore, they cannot afford to close their plants because they spent billions of dollars in investments, which electricity companies must make profitable.

As an example, the only significant uranium mine that has opened in the last 10 years outside of Kazakhstan was the Husab mine in Namibia, built by the Chinese government. This mine was built in 2015 with uranium trading at $40/lb, even though Namibia has production costs between $60/lb and $70/lb. The Chinese government needs uranium for their reactors, regardless of what it costs them to produce that uranium.

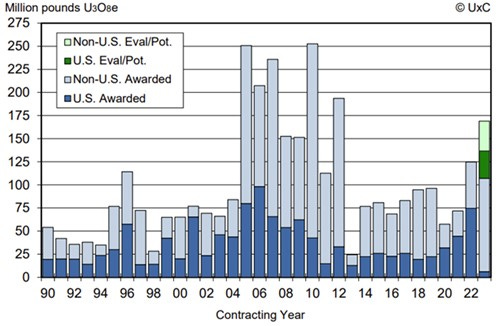

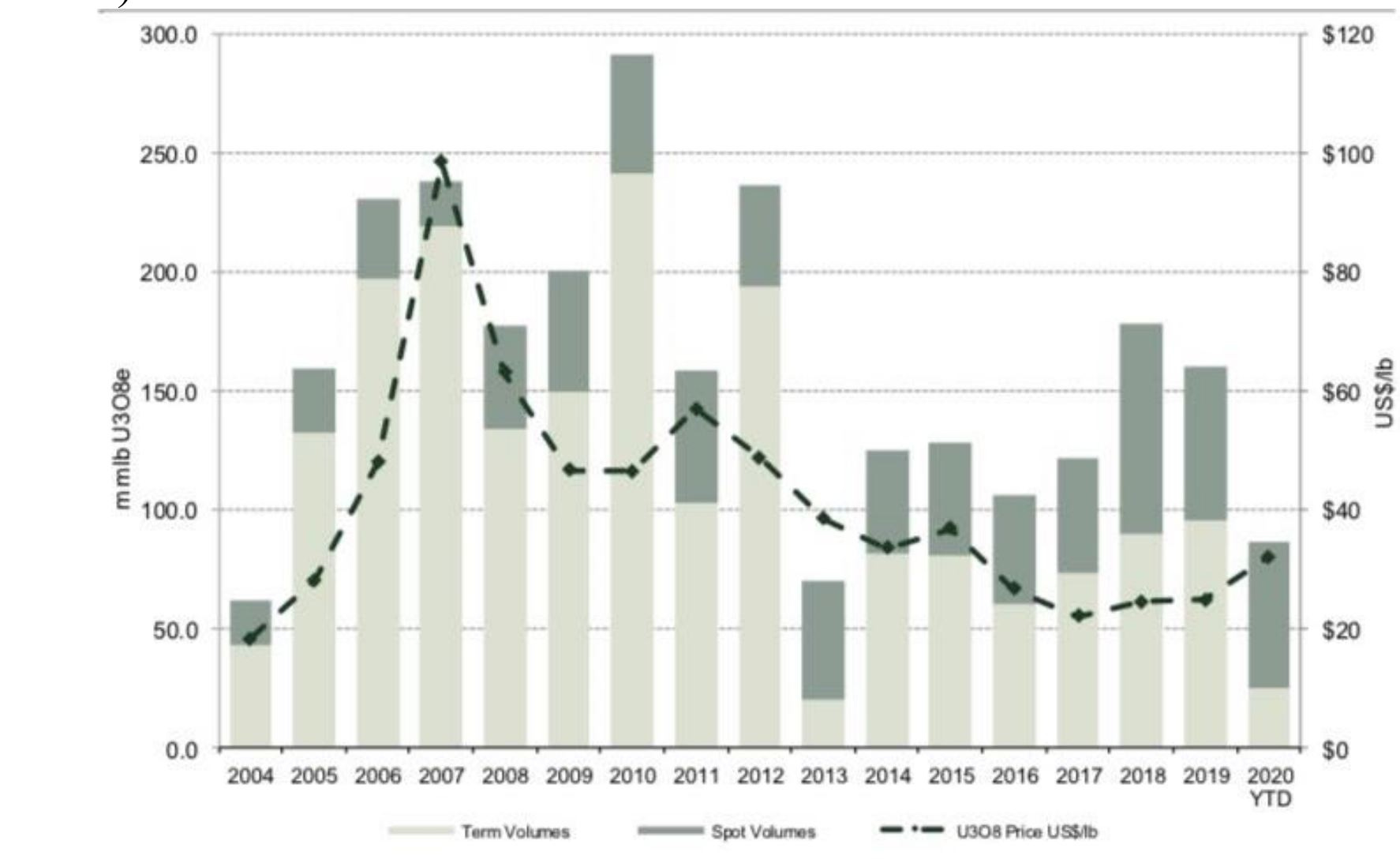

Uranium demand through contracts. UxC.

Demand for uranium originates in long-term contracts or in the spot market. As seen in the table below, most of the demand volume occurs in the long-term contract market, that is, a promise to deliver uranium in the future. This dynamic has changed in the recent years with the appearance of new uranium investment vehicles such as Yellow Cake or Sprott Physical Uranium Trust (formerly Uranium Participation Corp). These 2 investment vehicles routinely acquire their uranium inventory through acquisitions in the spot market. This table is a good indicator of how inelastic the demand for uranium is with respect to the price. The second largest year in terms of demand (2007) also coincides with the peak in the price of uranium at about $100/pound. This implies that utilities do not consider the price of uranium when demanding it. The main factor for the demand for uranium is the supply risk, that is, the risk that the electricity company cannot receive its uranium on the agreed date. Given this risk, the electric company is willing to pay practically any price, because the risk of not having uranium would imply the closure of the nuclear power plant.

Uranium demand through contracts and spot market. UxC.

Specifically, the rise in the price of uranium between 2004 and 2007 is because a Cameco mine was flooded. This caused panic among uranium consumers, who saw their supply of fuel for their reactors at risk. Given this shock to market, electricity companies began to acquire uranium at any price, which is reflected in the hiring volume that appears in table 24 between 2007 and 2010.

In 2020 Cameco shut down the Cigar Lake Mine due to the Coronavirus (COVID-19) pandemic. The market quickly reacted, and the price moved from around $30/lb in 2020 to $100/lb in 2024 when it peaked. Uranium has since moved back to $90/lb in the spot market but I’m expecting higher prices, as Kazatomprom is running into supply issues and Cameco is slowly running out of ore.

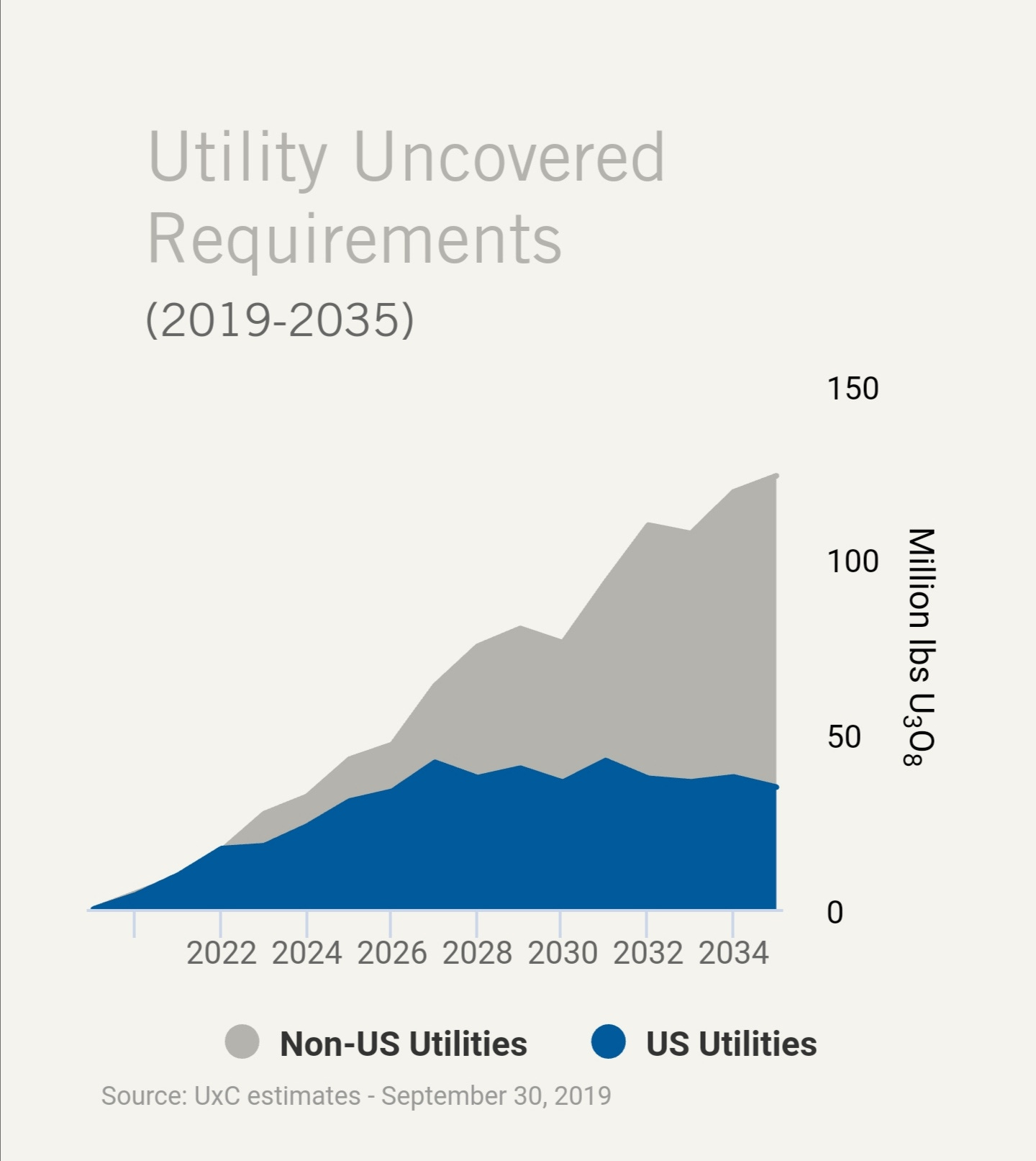

Unmet uranium requirements, millions of pounds. UxC.

The uranium requirements are the demand for uranium generated by the nuclear reactors. It is called requirements because it is a measure that can be predicted and calculated, because each nuclear reactor consumes a certain amount of uranium. What the table shows is the number of pounds of uranium that are going to be consumed by reactors and that have not been contracted by electrical companies. The table shows the amount of uranium that electric companies must acquire over the next few years to power their nuclear power plants. Electricity companies are going to have to acquire tens of millions of pounds from uranium for years, to be able to keep its plants operating. To achieve this, the electricity companies will have to make contracts with uranium developers, so they can build the mines. Without these contracts, uranium developers will find it hard to find financing for their mines.

This will happen because Kazatomprom, Cameco and the other state-owned mining companies do not have the capacity to satisfy all the uranium that will be contracted in the coming years.

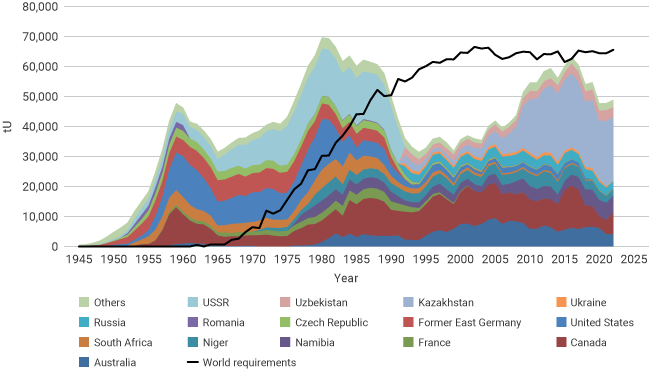

Uranium demand and production. OECD-NEA, IAEA, World Nuclear Association.

The IEAE shows in this table that the sector has been in a deficit since the 1990s. That is, the sector does not produce enough uranium to meet demand, and the difference is supported by uranium inventories and secondary supply. The Cigar Lake mine is scheduled to close in 2031 and McArthur River will foreseeably close operations around 2040. And Cameco does not have any mine under construction to replace these two mines. Cigar and McArthur have provided the world with around 20% of the world uranium for almost the past two decades.

In fact, they are now switching their business into the reactor building business. In 2022 Cameco bought Westinghouse with Brookfield for $8.1 billion. So, I don´t expect them to purchase any further mines. This is a paradigm shift as many were expecting Cameco to takeover Nexgen Energy and/or Fission Uranium. As Cameco exits the uranium business over the next decades it will be interesting to see who takes over its role as the major Canadian uranium miner. In my opinion, it was a mistake on behalf of Cameco not to do M&A in the years prior to 2021. Some countercyclical takeovers would have been very accretive in terms of shareholder value creation.

As the table below shows, uranium deficits increase from the year 2030, which is when the Cameco mines begin to run out of uranium in their deposits. By 2035 there will be at least 100 million pounds of uranium deficits per year. For context, Kazakhstan produces 45-50 million pounds of uranium per year, and they produce almost half of the uranium of the world. So, by 2035 the world needs twice the production of Kazakhstan. And there are no projects of that size out there, nor are there numerous projects to replace them.

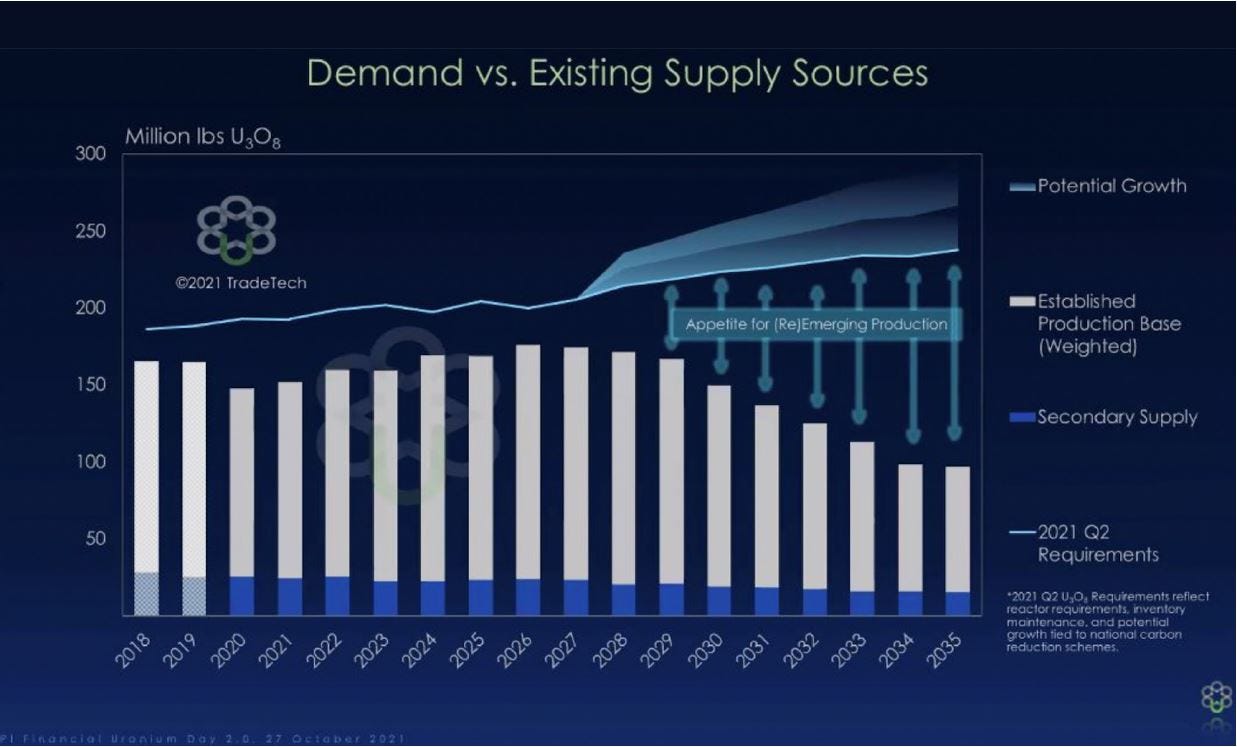

Uranium demand and production forecast. TradeTech.

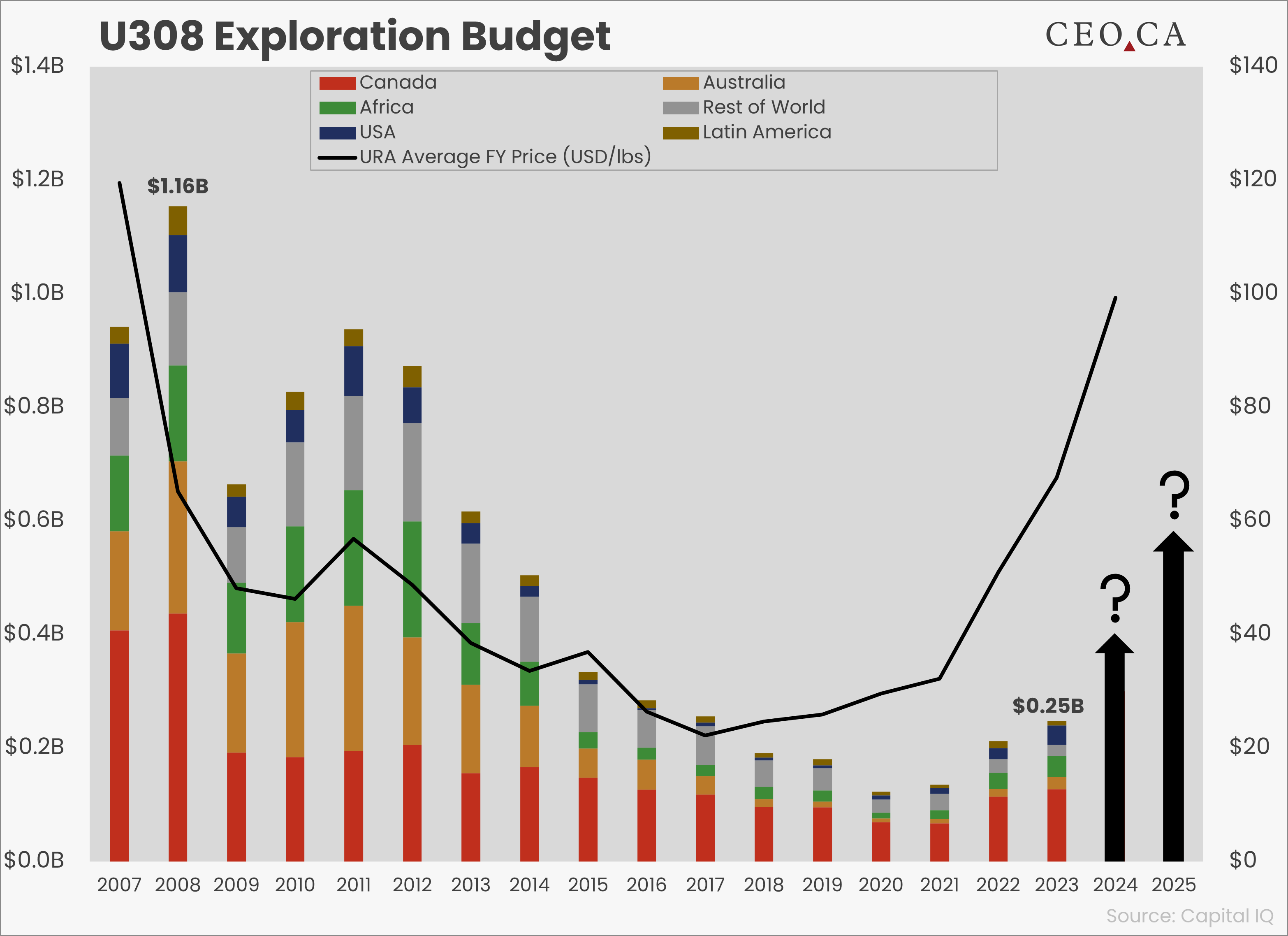

A mine is built because a deposit has been found and it is considered economically viable. To find these deposits, it requires the activity of exploration or prospecting for mineral resources. An expensive and risky activity but fundamental for the mining industry. As can be seen in table below, spending on uranium exploration has plummeted since Fukushima accident in 2011. This means that firms are not searching for or finding new uranium mines. And the mines that are being discovered are not sufficient to offset the enormous demand for uranium and the uranium requirements that have not been covered.

Exploration budget for uranium in different regions. Capital IQ.

A significant consequence of this sustained lack of investment is the lack of human capital in the uranium business. Most geologists work in the oil and gas world because it is a much larger sector than conventional mining. Of the few geologists who enter mining, the bulk of them enter the gold, aluminium, iron, or copper markets due to their size. So only a minority of qualified geologists are dedicated to more specialized metals such as tin, cobalt, lithium, manganese, or uranium. This reality of the job market for geologists, combined with the bearish dynamics of the uranium sector, have resulted in the current situation of the sector: shortage of qualified and experienced workers. This is easily seen after having analysed all companies in the uranium sector. Of the 500 companies dedicated to uranium inn 2011, today there are only about 50 companies that are really dedicated to something related to uranium. This has led to the dissolution of hundreds of companies and the dismissal of hundreds or thousands of employees. Of the 50 companies that today operate in the sector, there are only a handful that have been operating since before the Fukushima accident: Cameco, CGN, Kazatomprom, Goviex, Bannerman Resources, Paladin, Encore, Goviex, Denison, Energy Fuels, Uranium Energy Corp, and Ur Energy. These companies I mentioned are uranium miners or developers. There are also some explored ones that have survived the bear market: ALX resources, Forum Energy Metals, CanAlaska, Skyharbour or Purepoint. That is, of the 50 companies in the sector, only 18 companies have operated for more than 10 years. This implies that finding a good uranium geologist, or at least one who has a decade of experience, is another barrier to entry to compete in the sector.

Image of the Rolls Royce reactor design. Rolls Royce.

Until now, the construction of nuclear reactors was carried out in the place where they were to operate the reactor, just like a building is built on the same site where it is going to be located. However, for years the Small Modular Reactors (SMR) technology has been developing quickly. It offers better guarantees of security and non-proliferation of nuclear technology, better economics, and improved safety. But what is revolutionary about this technology is that the reactors will not be built at the site of operation, but will be built in factories, assembling them just like in a car factory. Some analysts compare this evolution of the nuclear technology with the innovation of Henry Ford, with his factories at the beginning of the 20th century, which made car manufacturing enormously cheaper. One of the most advanced firms in this technology is Rolls Royce, which plans to build a factory for reactors in the United Kingdom, with financing from the Qatar sovereign fund.

In the late 19th century and early 20th century oil had little demand and few applications. Just a few years later oil had become the major commodity in the market, and tycoons like Rockefeller had made a fortune out of it. This was all thanks to Henry Ford, which made cars affordable. I believe we are on the brink of something similar with uranium. Once SMRs are deployed and factories get built, cheap nuclear will de deployable anywhere in the world within a few months. I believe this will make uranium the new oil in the 21st century.

However, other companies such as Terra Power, owned by Bill Gates, or NuScale, which has gone public, also have SMR nuclear power plant designs. In fact, Terra Power is already building a demonstration reactor in Wyoming that will replace the Naughton coal plant, thus taking advantage of the existing electric grid infrastructure. The Terra Power design is especially interesting, because the reactor has safety mechanisms that cool the reactor, in the event of a sudden shutdown in the energy supply. So, in the event of a catastrophe such as a hurricane or an earthquake, which leaves the infrastructure without electricity or in worse conditions, the reactor shuts down automatically.

Russia's invasion of Ukraine has had a significant impact on the uranium market as could be seen in the section on the Structure of the uranium market, earlier in this report. This has contributed positively to the uranium thesis. This is because the increases in conversion and enrichment prices will encourage plants to reopen or increase production or capacity. Conversion plants consume uranium oxide to produce uranium hexafluoride. And the enrichment facilities consume uranium hexafluoride to produce high concentrations of uranium235. Therefore, this demand will be transferred to the mills that produce uranium oxide, and these mills will demand more uranium from uranium miners. So, this demand that is being generated at an intermediate point in the chain supply of uranium (conversion and enrichment), will result in an increase in the demand for uranium miners.

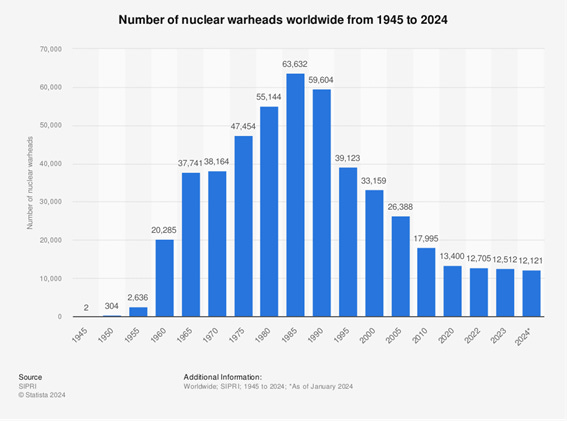

Number of nuclear warheads worldwide. Statista.

Since 1985 the world has been dismantling nuclear warheads. In 1985 there were over 60,000 nuclear weapons and today there are just over 12,000. I believe that due to the escalation of conflicts in Eastern Europe and the Middle East, there is a high probability of this trend changing. This is unfortunate for humankind, as I think peace is very prosperous for us. But this could exacerbate even more the uranium market. There are in fact rumours that Russia is developing a new kind of nuclear weapon deployable in space. This kind of developments could spark a new arms race.

Also bear in mind that a lot of tactical weapons are now hydrogen bombs. However, these bombs also require of uranium to work. Therefore, an increase in construction of these weapons will also increase demand for uranium.

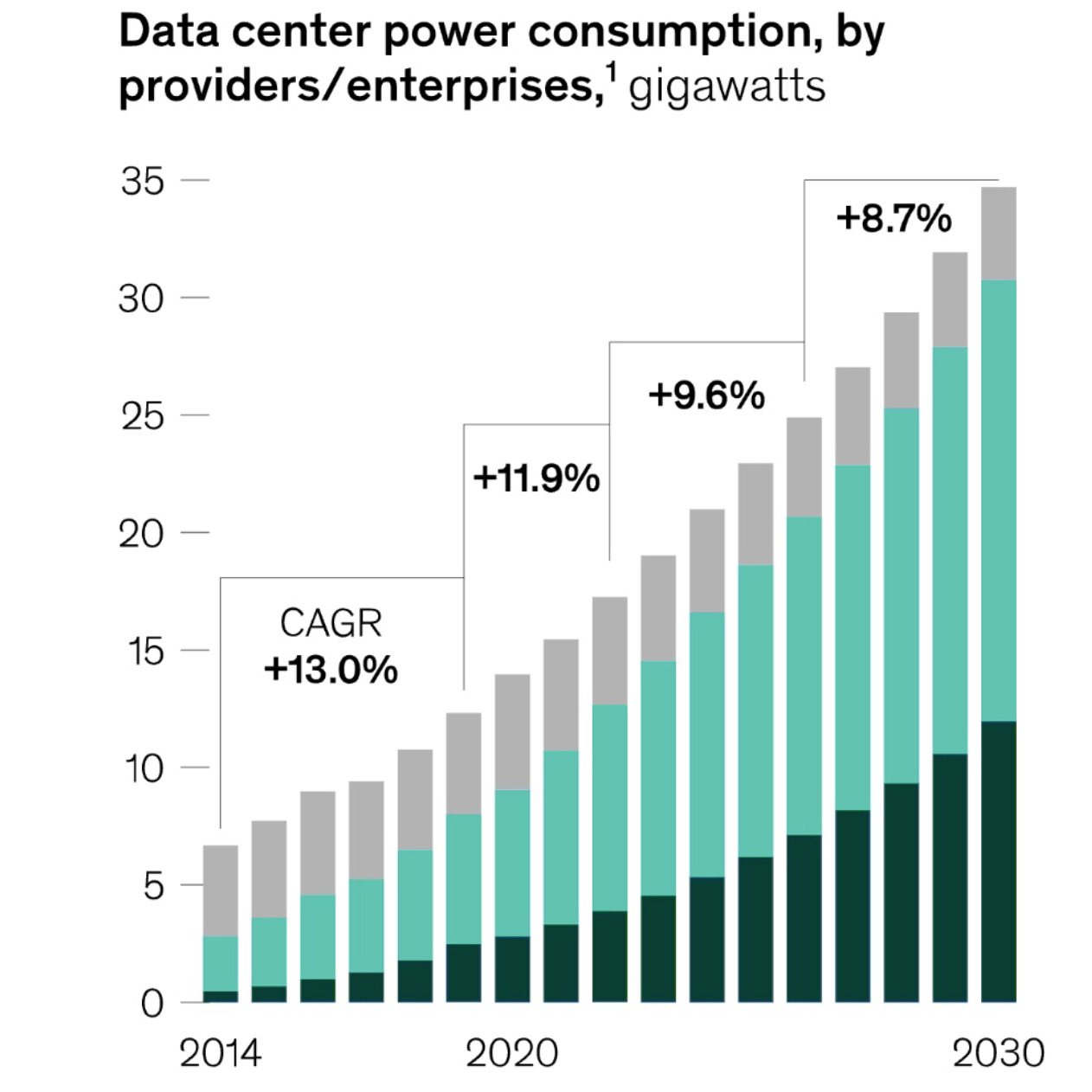

Data centre power consumption. McKinsey.

Artificial intelligence and such developments have taken the world by storm lately, With Nvidia becoming the worlds largest company by market cap for a short period of time. These new developments in technology require massive amounts of data. In fact, the larger the amount of computing power, the “smarter” the AI can become. McKinsey predicts that the power required for data centres will explode by 2030. This will result in more baseload energy required. Therefore, increasing the need for nuclear energy. I think uranium is a great way to play the AI thesis.

Regarding Yellowcake PLC and Sprott Physical uranium trust, they have been buying millions of pounds in the past few years. Yellowcake PLC holds 21.68M pounds of uranium which has bought and kept in their inventory. When Sprott bought Uranium Participation Corp they had 16.3M pounds of inventory, now Sprott holds over 65.5M pounds of uranium. Therefore there are tens of millions of pounds that the utilities don´t have access to, increasing the deficits.

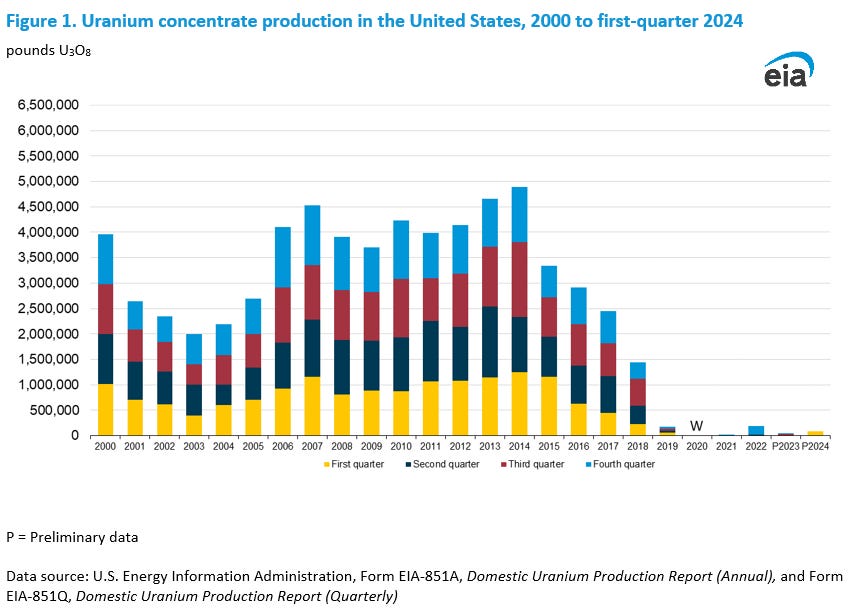

US production of uranium. US Energy Information Administration.

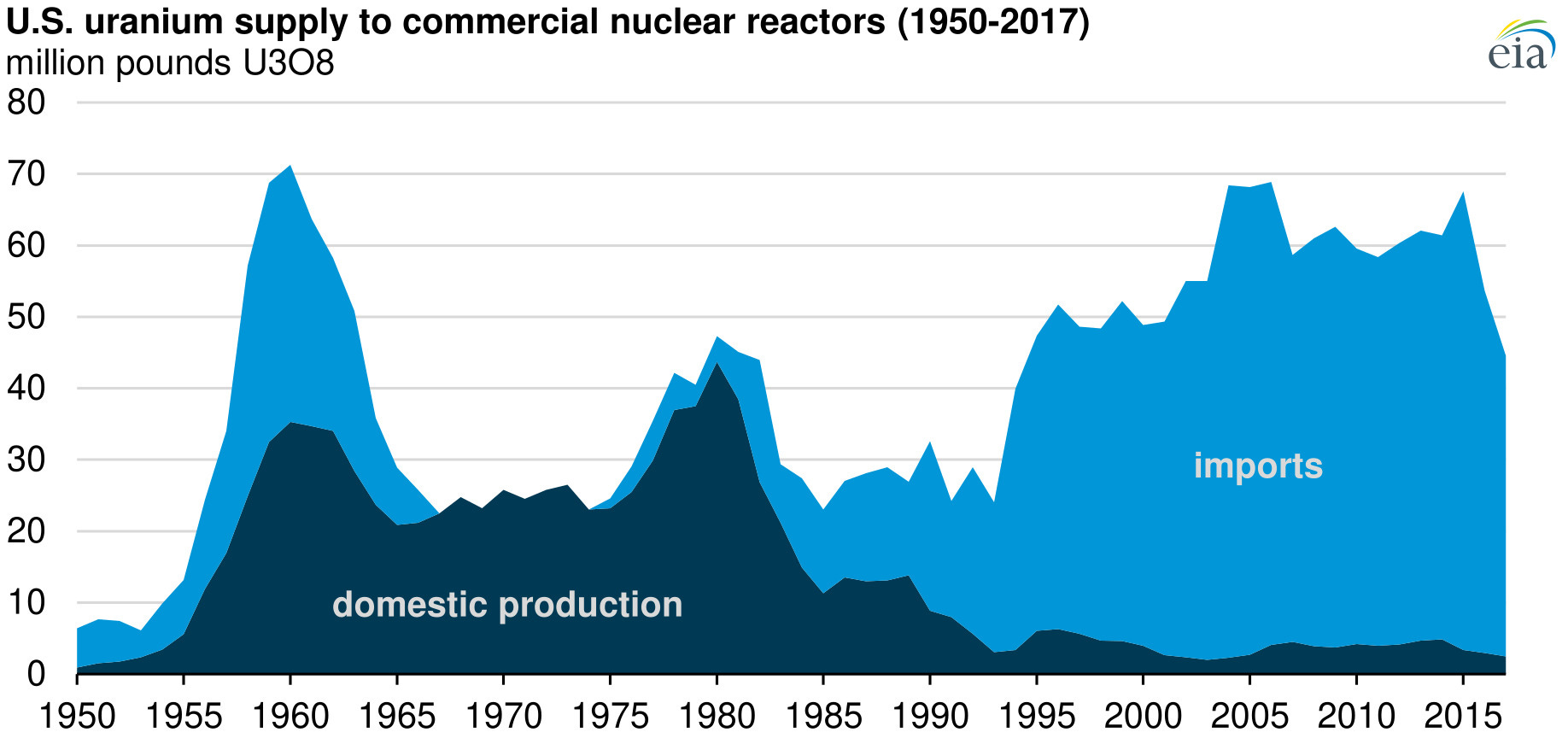

The United States is the largest consumer of uranium in the world. And back in the 1970s and 1980s they were self sufficient in terms of uranium consumption. Now the US produces almost nothing and they have to import almost everything. This has created an interesting dichotomy in which the US is the largest uranium consumer, while the largest uranium producers are old Soviet States or African countries. These are regions in which the US has little influence.

This situation has created somewhat of a security threat to the US. And the government just announced a $2.7 billion plan to buy domestically supplied enriched uranium. Congress has also passed a ban on uranium coming from Russia, which will likely create bottlenecks through the uranium supply chain. It is yet to be seen how this ban will affect Kazakh uranium, which could lead to further supply issues.

US production of uranium and imports. EIA.

Finally, I would like to comment on the utility companies, the ones responsible for purchasing uranium for their nuclear reactors. People wonder why they weren´t buying when uranium was below $20/lb. And to solve that conundrum, you must first put yourself in the shoes of a fuel buyer at a utility firm. The fuel buyer does not care if the firm must spend $1 million on uranium or $10 million, because that number is insignificant in comparison to the billions they spent building the power plant. All that a fuel buyer cares about is supply risk: will my reactors have enough uranium to feed them? If the answer is no, the buyer will purchase uranium, even if it’s at $400/lb. That´s why this thesis is so enticing to me even if I’m only holding physical uranium. We could see the price of uranium quadruple from here and demand would increase, not decrease.

Summary of the uranium thesis:

· Uranium is a metal with a constant and predictable demand, which has no substitute and is therefore inelastic to price, because it is perceived as essential for its consumers (electricity companies).

· This inelasticity greatly benefits miners in a situation of clear uranium shortage, such as the actual situation.

· It is a recurring consumer good because light is a product consumed daily and which also usually represents a small percentage of income, more so if we consider that uranium is a small percentage of the cost of a power plant.

· Nuclear energy is present in about 30 countries, making it a global industry, which benefits uranium producers because they are not dependent on the economic situation of a particular country. The uranium industry foresees an increase of demand for years, this increase will be sustained by new plants in China, India, and the Middle East.

· The development of SMRs will reduce the cost and complexity of nuclear energy. And it could lead to a development of the nuclear industry similar to what happened with cars after Henry Ford.

· Uranium production is subject to very high barriers to entry. So, solving the supply deficits won’t be easy. Meaning that we will face higher prices for longer.

· Uranium consumers (utilities) have also spent years without entering into new long-term contracts with miners, which will force them to demand more in the years to come.

· The industry has not invested in new mines or uranium exploration for years. And now there are uranium firms (YCA and SPUT) buying uranium in the market.

· All this makes the uranium thesis solid and offers an interesting margin of safety.

· The only negative observed in this market is that it is highly regulated. This is a disadvantage because there are situations like the one in 2007 in which the utilities asked the US government to set a price (at $95/lb) ceiling in the price of uranium alleging national security problems. However, this measure had limited effectiveness because it only affected the long-term contracts, the uranium “spot” market recorded prices of $136/lb.

Conclusion

I think we are in the middle of a bull run for uranium. Furthermore, I believe we are on the brink of a paradigm shift in nuclear energy. As I mentioned earlier I believe SMRs will do to uranium what Henry Ford and his Model T did to oil: it will make nuclear affordable and make uranium the oil of the 21st century.

However, due to the massive capital inflows into uranium stocks, I believe the wisest move is to buy physical uranium, not the miners nor the juniors or the explorers. I am sure a few firms will outperform physical uranium prices, but they are now a lot more expensive than in 2020 or 2017 when I got into the uranium sector. And I don´t think anyone can spot with certainty which firms will outperform the uranium price. And I don´t think they are worth the risk.

My top pick is Mongolia Growth Group, which holds 40% of its assets as uranium.

For those not interested in YAK, you also have available Yellocake PLC and the Sprott Physical Uranium Trust as ways to invest in physical uranium.

As a speculative bet I think District Metals is worth a shot. Even if Sweden doesn´t legalize uranium, they have many other mining assets. If uranium does get legalized in Sweden, I think the stock price could easily go multiples higher from here.

I own YAK in my personal portfolio and through an account I manage. And I own DMX in my personal portfolio.

Kind regards,

Alberto Álvarez González.

I´m really impressed about your work. Well done! Congratulations !

As a "STEM" professional, and knowing a lot of STEM professionals, all that I know who do investing consider the idea that volatility = risk to be stupid. Maybe you were thinking of the wannabe-STEM people.