The resource exploration firms I own

Deep dive into what exploration companies I own and why I own them

Introduction

I have been investing for years in mineral exploration opportunities. And I now hold 8 explorers in my portfolio. In my last report on gold miners, in which I went through over 800 gold firms, I found some good exploration opportunities so I decided to engage in a small buying spree. Aurion Resources and Goliath Resources are by far my largest holdings, with the other 6 explorers each making 1% or less of my portfolio.

Finding a deposit is already hard, but finding an economic deposit has worse odds than playing the roulette. So, buyers be warned: exploration is probably the highest risk investments out there.

As Rick Rule points out, if we put all the junior explorers into one company, it would lose $2 billion a year, in a good year. In a bad year it would lose $10 billion.

That said, the industry is necessary for mining to exist and the reward can be immense when an economic deposit is found. That’s why the industry itself still exists and there are investors willing to speculate on these opportunities.

These stocks do not conform to my usual investment philosophy as the results are very binary: if they find something big, the stock will rise rapidly and if it doesn´t it will plummet. That´s why I’m not looking for more exploration stocks. And when I sell them (depending on drill results), I will employ the capital elsewhere.

The data in this report I have obtained it from investor presentations, technical reports and most importantly from speaking directly to the management of each firm.

Summary:

· My picks in the sector, by size in my portfolio are: Aurion resources (top pick) (CVE: AU), Goliath Resources (top pick) (CVE: GOT), Azimut Exploration (CVE: AZM), Radius Gold (CVE: RDU), Inflection Resources (CNSX: AUCU), Hannan Metals (CVE: HAN), CopperCorp Resources (CVE: CPER) and Gladiator Metals (CVE: GLAD). On October the 25th I sold my shares in Gladiator Metals at an 80% return, I still hold shares in Gladiator through an account I manage.

· Aurion Resources is a play on the great discovery Rupert Resources has made in Finland.

· Goliath is promising explorer in the Golden Triangle of BC with a large drilling plan.

· Radius Gold is the explorer with the best management team out there in my opinion

· Inflection Resources has a massive land package in Australia and it´s drill program is being financed by AngloGold.

· Hannan Metals is one of the largest mining landowners in Peru.

· Coppercorp is a well-capitalized explorer, with land adjacent to several mines and projects in Tasmania, Australia.

· Gladiator Metals is carrying out a big drilling program in the Yukon with the help of its largest shareholder.

· All firms are planning on drilling in 2024 or have drill results pending of releasing. So, there are catalysts that may cause an appreciation in stock price if something is found.

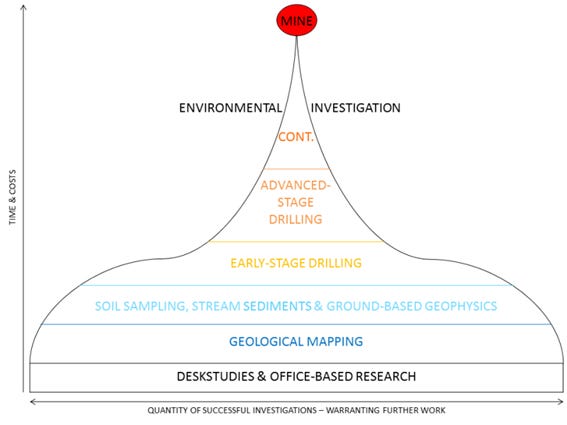

What is mineral exploration?

To mine a deposit, geologists must do prospecting activity. That is looking for mineral “anomalies” worldwide to find economically viable deposits. Without exploration there is no mining industry.

Geological Survey of Ireland. Prospecting process.

To explore, geologists carry out all kind of studies and mapping of areas that may be of interest. And once they find potential targets, they begin drilling.

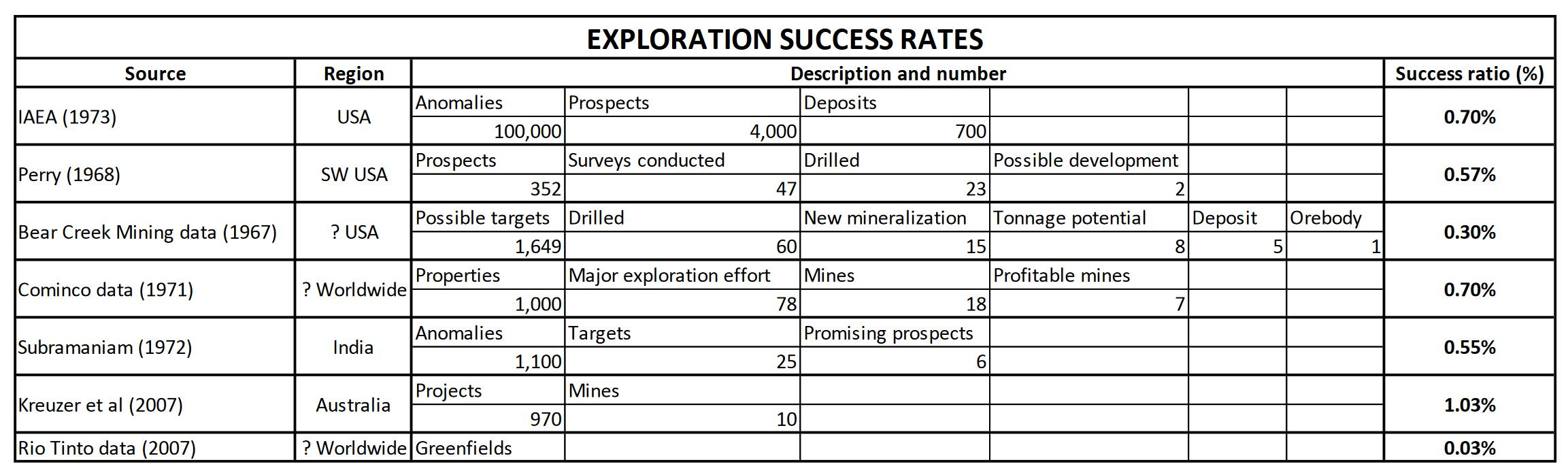

Chances of finding a deposit. Minerals Intelligence Capacity Analysis (MICA).

However, the probability of finding a deposit is extremely low. 0.03% to 1.03% of the targets drilled become deposits as you can see in the table above. That said, the probability of that deposit being economic (i.e. A firm being able to exploit it profitably) is even lower.

So why speculate in mineral exploration?

First and foremost, the big reason to speculate in exploration companies is the possibility of finding an economic deposit. If done, the returns can be enormous.

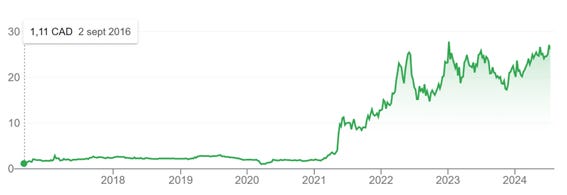

Filo stock price. Good finance.

Filo has returned 2,000%+ returns to shareholders since 2017 thanks to a big discovery in South America. Those who bought it at the bottom have had 2,500% returns.

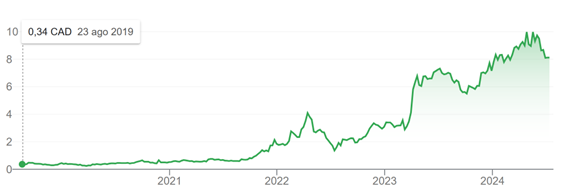

Another example is NGEx, which has also delivered a 2,000%+ return since its IPO. And a 2,700% return from the bottom.

NGEx stock price. Google finance.

However, these are the outliers. Most exploration companies have returned an 80% to 100% loss in the past 5 years or so. So, the risk is massive in these stocks, and their valuations are impossible to obtain, that´s why I consider them speculations, not investments.

Now that we are done with all the negatives, lets dig into the fundamentals of the industry. Especifically the fundamentals of the gold, copper and lithium exploration industries, since those are the segments that the exploration firms I own operate in.

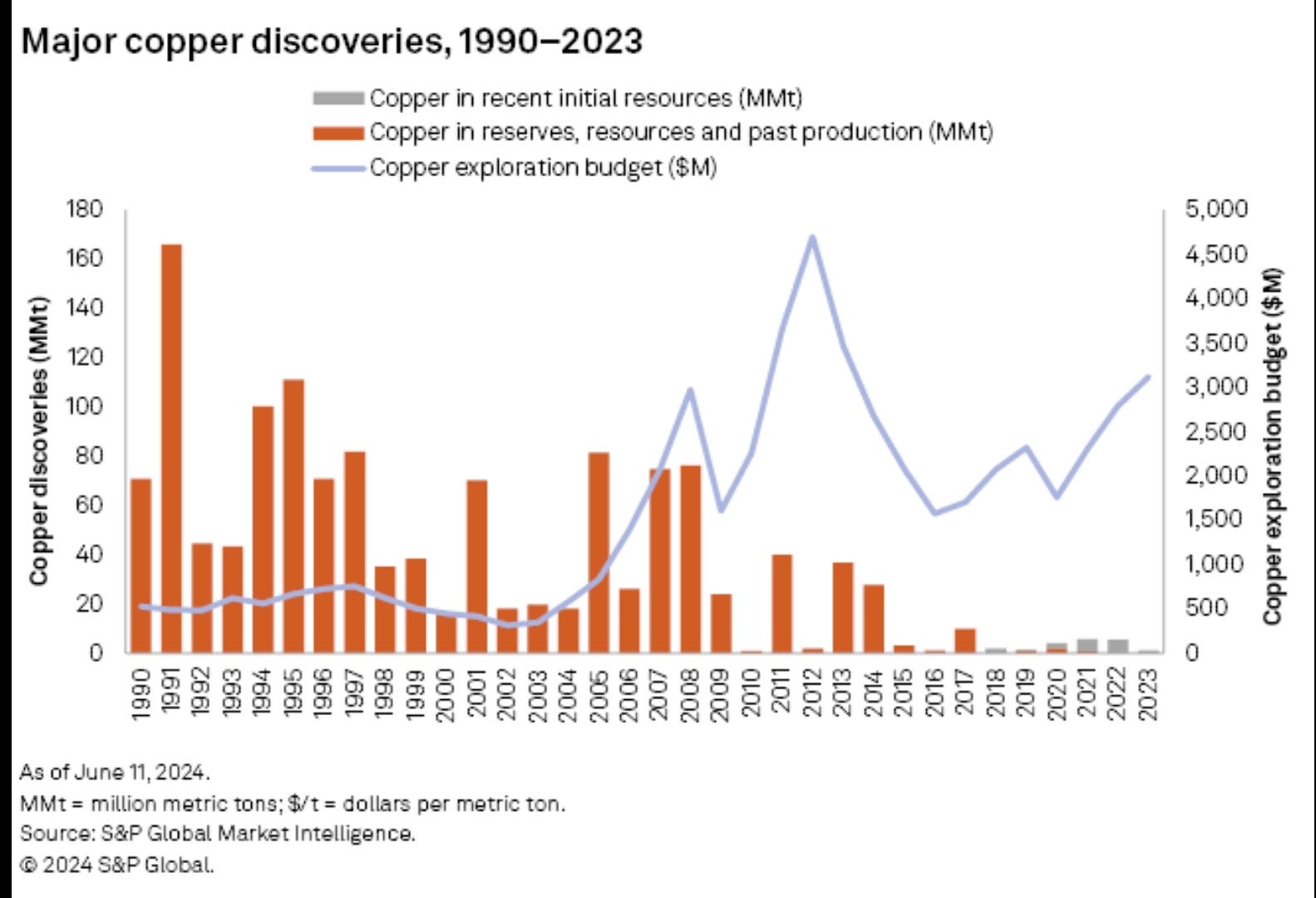

Exploration capex and discoveries in the copper industry. S&P Global.

The mining business has a very long cycle. By this I mean that to build a mine today, a firm had to spend time and money in exploration one or two decades ago. Rick Rule says that the mining industry has underspent in exploration since at least the mid 1990s. And the graphs above and below prove him right.

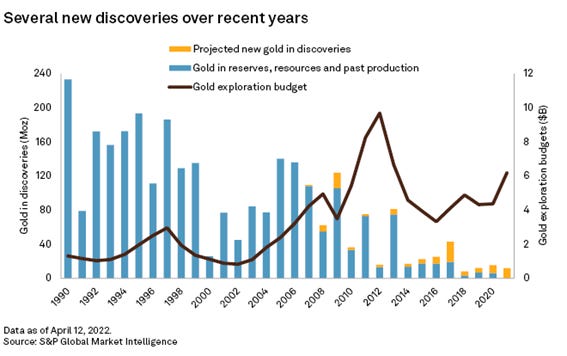

Exploration capex and discoveries in the gold industry. S&P Global.

Even though exploration for copper and gold deposits is almost at record highs, there are barely any discoveries of gold and copper deposits. And when there are, they tend to be small (with a few exceptions such as Filo). The industry should have spent billions of dollars decades ago to find deposits today. They have done the opposite: they are spending billions now to find deposits in 10 or 20 years.

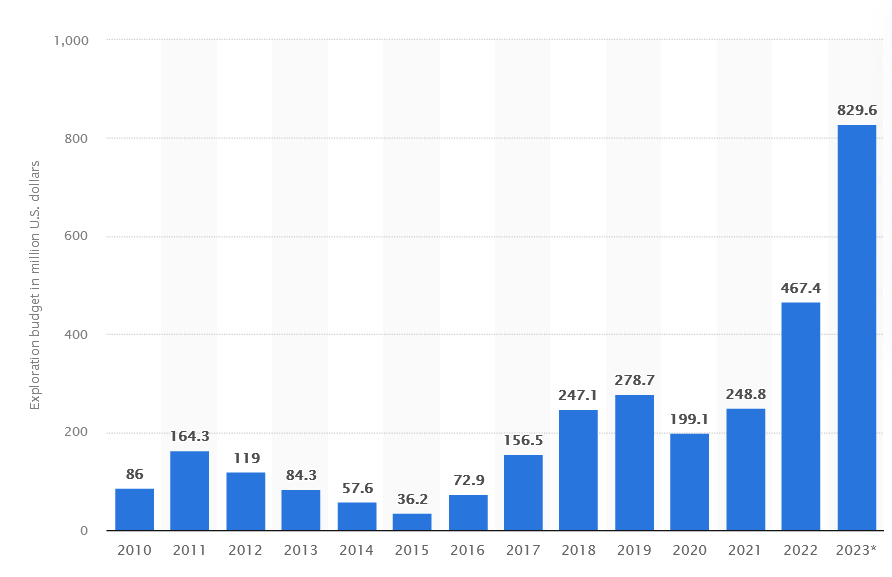

Lithium exploration capex by year. Statista.

Lithium exploration is at record highs. This is mainly due to the thesis of EVs and batteries taking over. One of the exploration firms I own is finding a lot of lithium in one of its properties, and is being financed by one of the largest lithium miners worldwide.

Historically speaking the major discoveries have been made by exploration companies, not mining firms. And big mining companies have been decreasing their JV activity and lowering their investments in small mining firms. And why are the small exploration firms the ones that make the big discoveries and not the large mining firms? Well, it makes perfect sense if you think about it deeply: its all about incentives. Imagine you are the head of exploration at a big firm like Barrick and you discover the next deposit that will produce 500k ounces/year for the firm. What will you get in return? A nice bonus and a round of applause from your colleagues at best. If you are the CEO of a small exploration firm and you hit a big deposit, you can make millions or even billions. People like Ross Beaty or Bob Quartermaine have become very rich thanks to exploration.

Another important factor to consider is that big mining firms will almost always come in late to the party. They have 3 options: find the deposit themselves, have JVs with multiple exploration firms or wait for a firm to make a big discovery. If they can´t make the first option work, they will go for the second or third option: takeover. These takeovers will happen once the big mining firm believes the deposit is economic and big enough, to move the needle in the bottom line of their financial statements. And those kinds of takeovers tend to be expensive.

I believe we are in the innings of a new capex cycle of mining exploration. And this time mining firms will go all out into a buying spree, as the supply deficits in copper and gold are looming.

Deep dive into Aurion Resources: The next Rupert Resources?

I already did an analysis on Aurion on my previous gold report. So, I will limit myself to pasting my previous research here. After that I will put specific data about their projects.

Here is what I wrote on my previous report:

Rupert resources stock. Google finance.

Rupert resources has one of the best gold deposits in the world. Hosting a $1B+ NPV (10%) deposit that will produce 200,000 ounces of gold a year for 22 years for $759/oz AISC. The CAPEX will be of $405M. The deposit is very high grade, and the recovery rate is of 95%, very high.

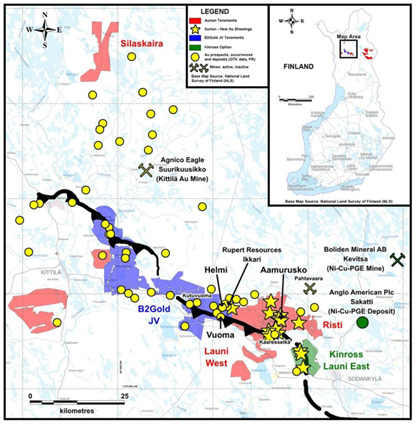

Aurion resources investor presentation. Aurion asset map.

My way to play this deposit is through Aurion Resources. Rupert owns the Ikkari deposit. And as you can see in the map above Aurion owns the land adjacent to Rupert. It owns it either through its 100% owned tenements or through a JV that Rupert has now acquired from B2Gold.

I am not going to try to give a valuation to Aurion because it would be impossible. But the chances of them continuing to find gold is extremely high.

They have 2 JVs. One with Kinross in which Kinross will have to spend $10M to earn 70% of the land. And another with Rupert. I think both Aurion and Rupert will consolidate sooner or later, and they will be taken over by a large mining company. But this is just speculation for now.

Management owns 12.7% of Aurion. Kinross, Newmont, and Eric Sprott own another 15.4% all together.

Just in January and March of 2024, the Chairman of Aurion David Lotan bought 200,000 shares. And he now owns over 13.4M shares of Aurion. He is a specialist investor in mining, he was the portfolio manager for the Ontario Teachers' Pension Plan for a year. And he is the CEO of LHI Capital. CEO is Matti Talikka, who is Finnish and knows the region better than anyone else.

I own shares in Aurion Resources.

Here is what is new:

Aurion project details. Investor presentation.

The B2Gold & Rupert JV has 4000m of drilling pending of releasing.

The firm has 2.01M in NCAV. They are funding the Launi West and Risti projects. While Kinross is financing the Launi East project. Since neither Launi West nor Risti are undergoing exploration programs I think they are well capitalized going forward.

Aurion has confirmed that Rupert is talking to them. So, a potential takeover or merger may be upon us.

Rupert Resources has delivered a 12,000%+ return from the bottom. And Aurion owns almost all the land adjacent to Rupert´s deposit. Considering the very good prospectivity of the properties owned by Aurion and the exceptional management team they have, I put Aurion as one my top picks for exploration firms.

Goliath Resources: The next Great Bear Resources?

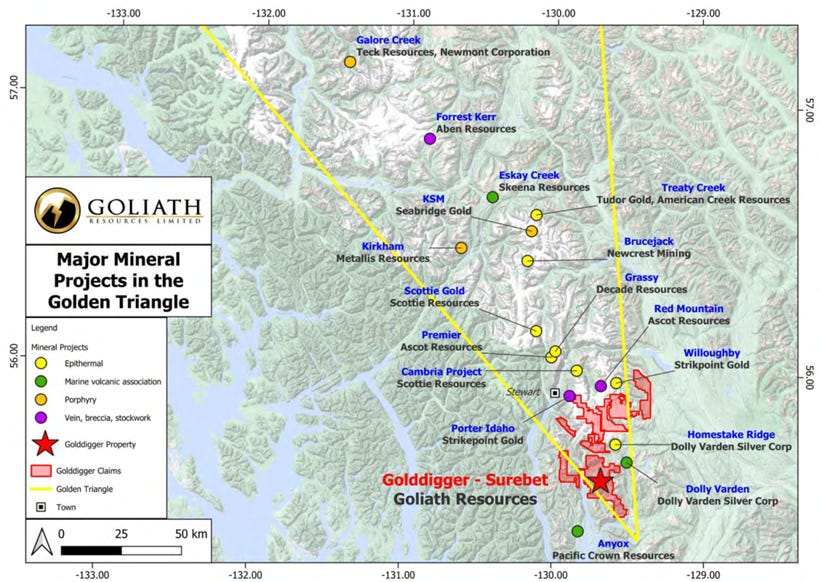

Goliath land holdings. Investor presentation.

The company´s flagship projects Golddigger sits in the middle of several projects. Namely two projects owned by Dolly Varden, another two projects owned by Strikepoint, and a project owned by Ascot Resources.

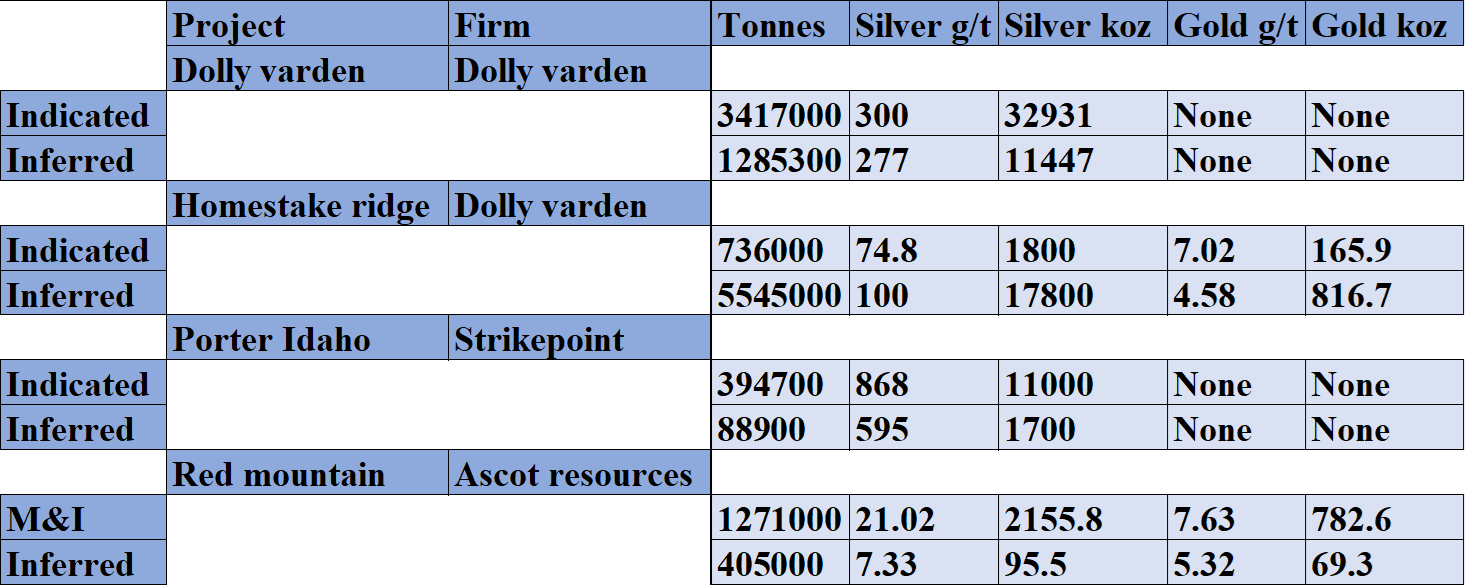

Projects adjacent to Goliath. Resource studies of the various projects.

As you can see in the table above. Goliath is surrounded by projects that already have a resource estimate. Dolly Varden and Ascot have medium sized deposits at a very high grade. Therefore, I expect similar results at Goliath.

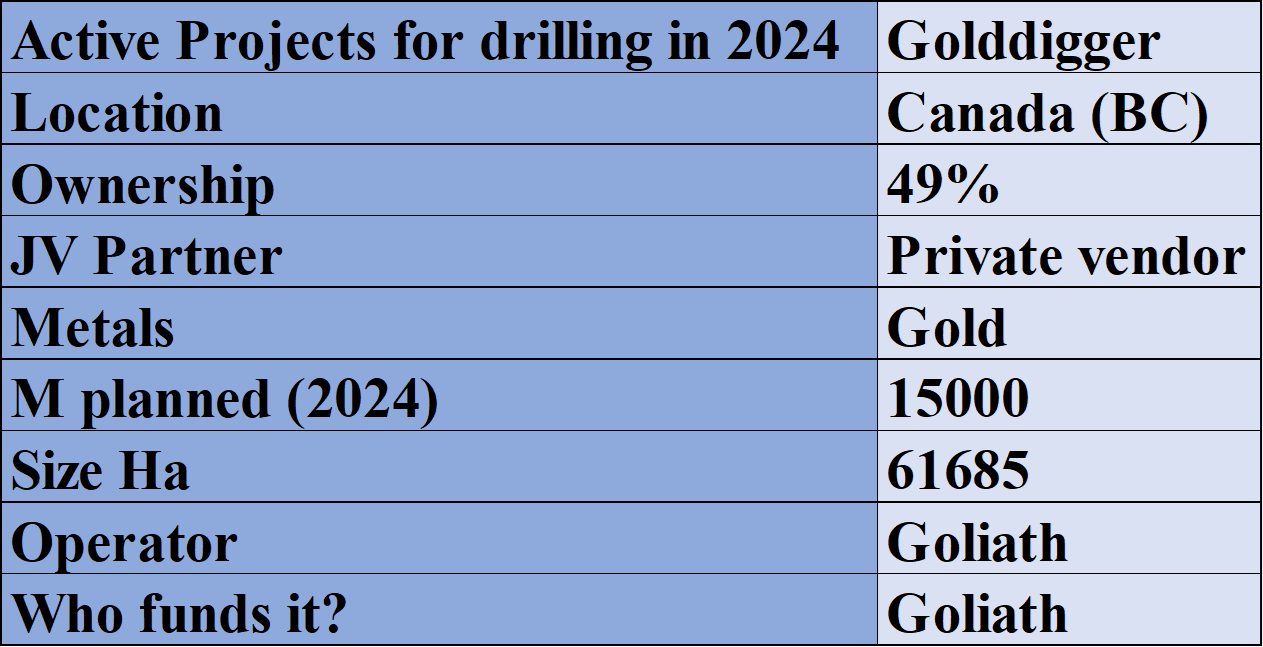

Goliath project details. Investor presentation and news releases.

The firm owns 49% of the project and will own 100% once they deliver a NI 43-101 maiden resource report outlining a minimum of 2,000,000 AuEq ounces (M&I, Indicated and/or inferred) on or before June 1, 2027.

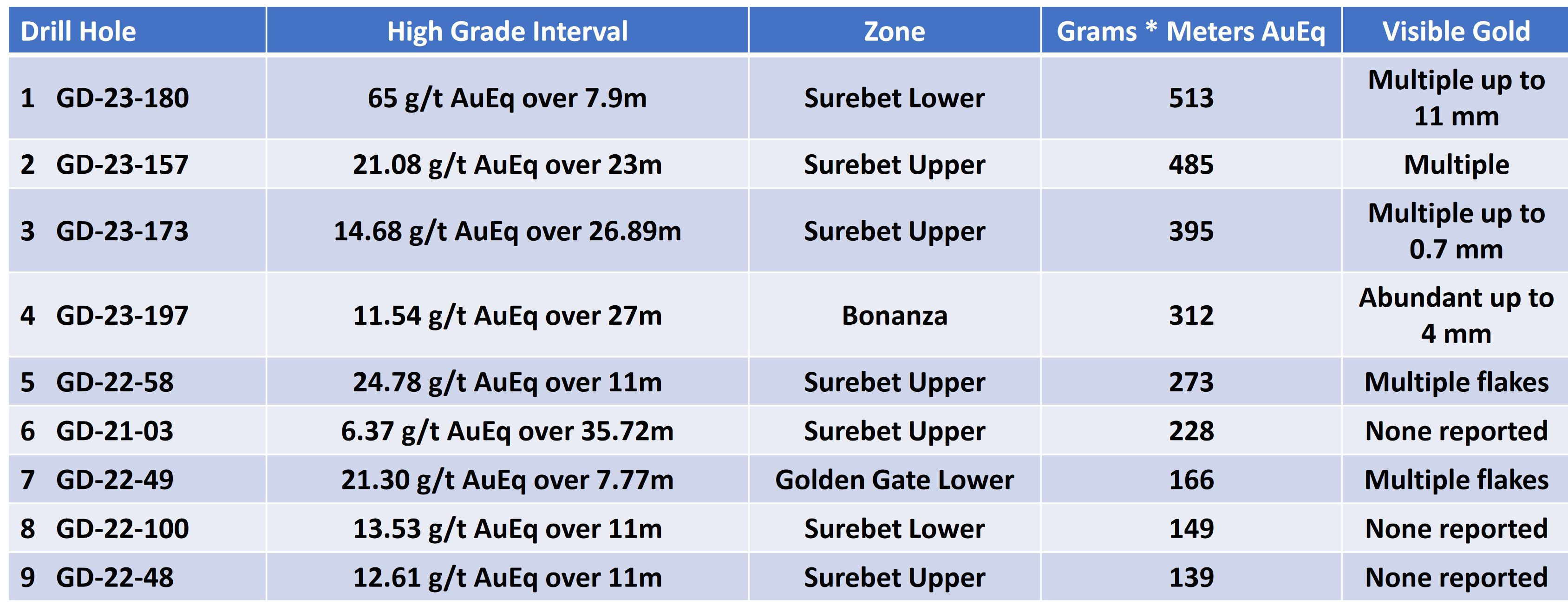

Goliath is planning an aggressive drilling campaign for 2024 of 15,000m. Considering the exceptional drill results they have obtained until now, and the projects adjacent to Goliath, I expect this drilling to result in a lot of value creation.

Goliath drill results.

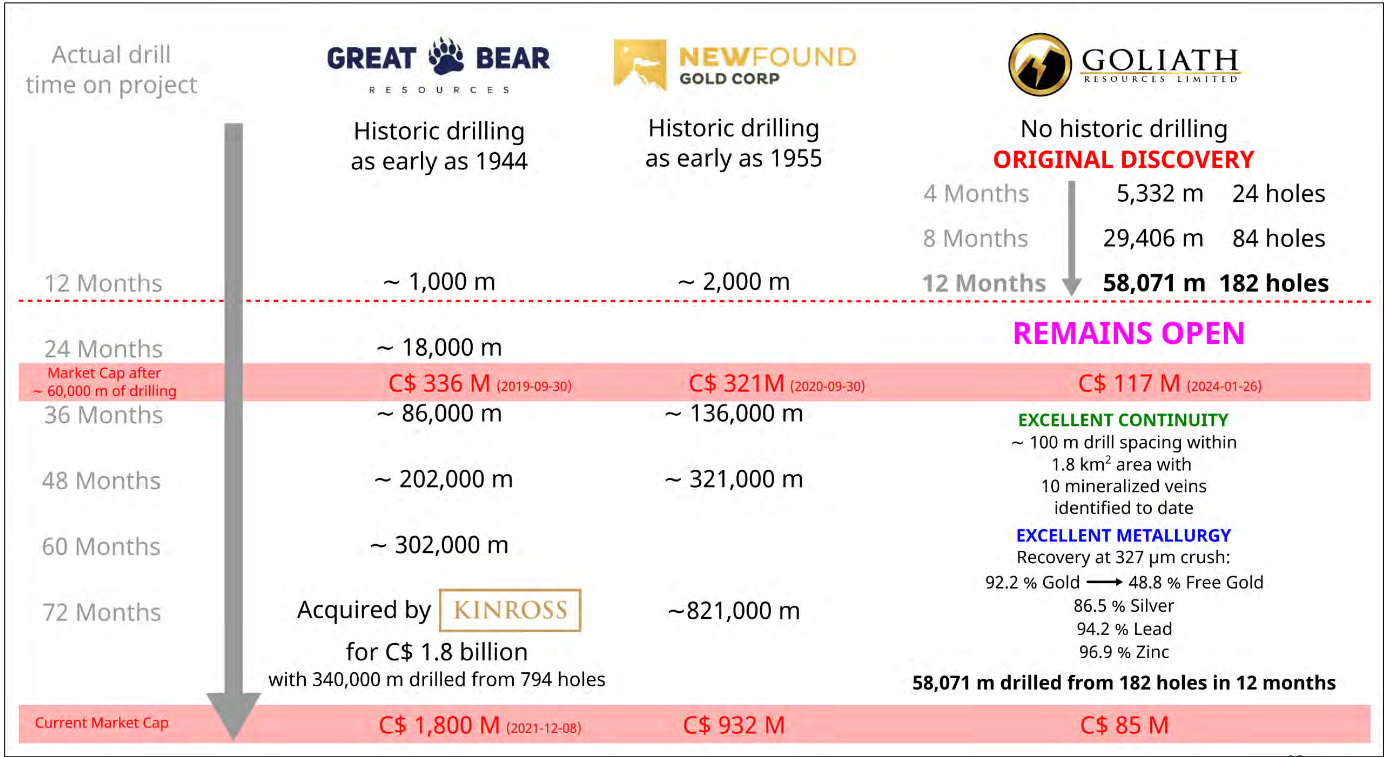

Great Bear was a great success, at least in terms of investor returns. From 2018 till its takeover in early 2022, Great Bear returned around 2000% to shareholders in stock appreciation. Their strategy was simple: drill and carry out no economic studies or resource studies. Goliath has a similar strategy. They are carrying out a very aggressive drilling program. As you can see in the table below, in terms of drilling activity, Goliath is trading at a discount to the situation Great Bear was at with the same drilling results.

Great Bear, New Found Gold and Goliath comparison. Investor presentation.

The company is advised by Dr. Quinton Hennigh, one of the best regarded geologists worldwide. I have had the chance to ask management some questions in a video call and I have been impressed.

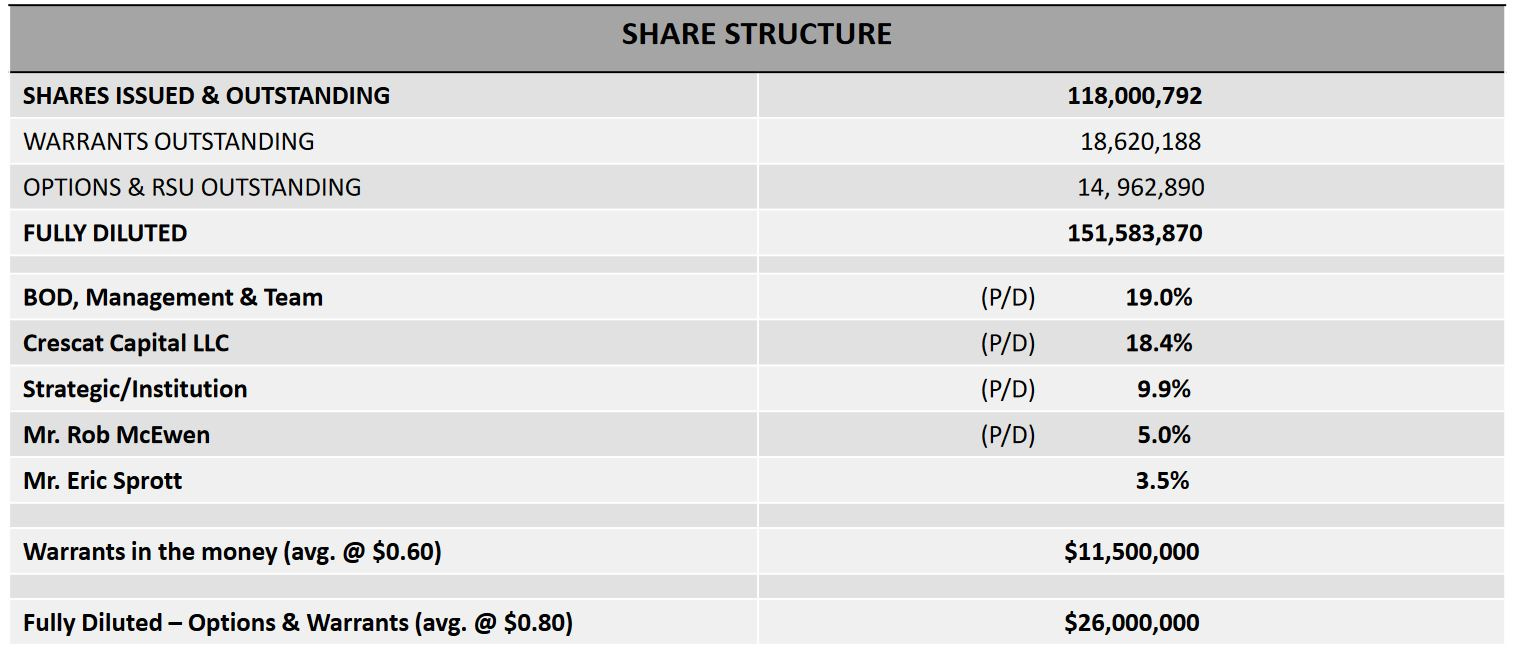

Goliath shareholders. Investor presentation.

Management owns 19% of the firm. And two mining veterans (McEwen and Sprott) also own shares in the business. Crescat Capital also owns a lot of shares, a firm specialized in precious metals and macro investments.

Deep dive into Radius Gold: A bet on exceptional management

My play on Radius Gold is mainly based on the “genius” that runs it: Simon Ridgway, he discovered Cerro Blanco (Bluestone Resources now) and one of the veins that ended up becoming Escobal (now owned by Pan American Silver). He founded Fortuna Silver and moved the company from CAD 0.17/share in the IPO in 2003, to CAD 9.73/share when he stepped down in February 2021. That is a 5,500%+ return.

He is self-taught. He moved to North America in the 70s with little money. He started learning mineral prospecting in the Yukon just from shadowing other geologists. He holds no degree in mining or geology, it´s one of the few prospectors out there who has had major success with no technical education, something I admire. He became a professional poker player back in those days, from which he learnt the basics of risk and reward.

Radius projects. Radius website and news realeases.

Radius gold has 3 JVs. One in Mexico (Amalia) with PAAS (65% PAAS & 35% RDU).

Another one also in Mexico: Plata Verde (drilling this summer). It is an old Mexican silver mine discovered by Radius. Drilling is funded by Fresnillo. The mine was in operation a hundred years ago and was abandoned most likely in the Mexican Revolution. Radius discovered the mine by itself, and I am expecting good results of the drill program.

Fresnillo can earn 70% into Plata Verde by spending $5M.

Radius has another 2 JVs in Guatemala with Volcanic Gold. There was a discovery at Holly, 40km away from the Cerro Blanco mine and 20km away from the Escobal mine.

Volcanic has an option to earn a 60% interest in the Holly project and the Motagua Norte project, by spending US$7M on exploration on the properties within 48 months from March 2021.

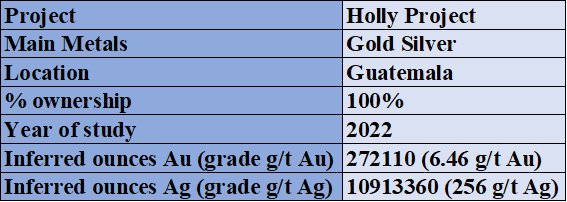

Holly Project details. Resource study.

Interestingly, Radius already has a resource done at one of its projects. Something rare for a firm so small. Even though the deposit is small, and the ounces are inferred, the grade is very high.

Radius has $1.13M in NCAV which is more than enough considering all the projects owned by Radius are funded by its partners.

Radius Gold shares outstanding. TIKR.

Something common among junior miners is the issuance of shares, diluting shareholders. Radius has done a great job at this by bringing partners into the projects. The partners have funded exploration for years. In fact, 2023 was the first time in 10 years that Radius issued shares.

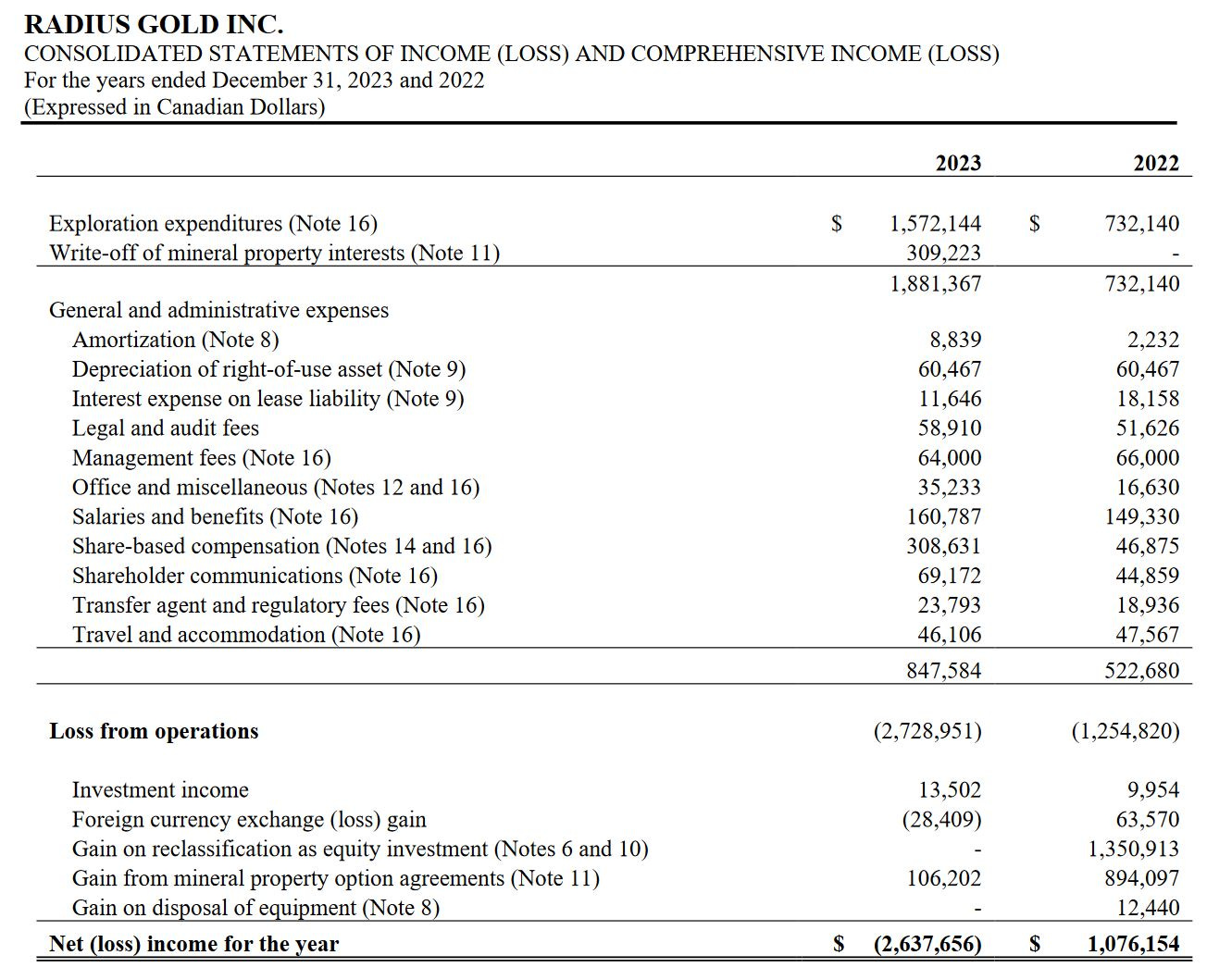

Radius income statement.

Another thing I like about Radius is that they spend a lot in exploration. It may sound obvious, but as Rick Rule often points out: most exploration firms waste their cash on executive compensation as opposed to exploring for projects.

Management owns 15% of Radius.

Deep dive into Azimut: Onto the discovery of gold and/or lithium

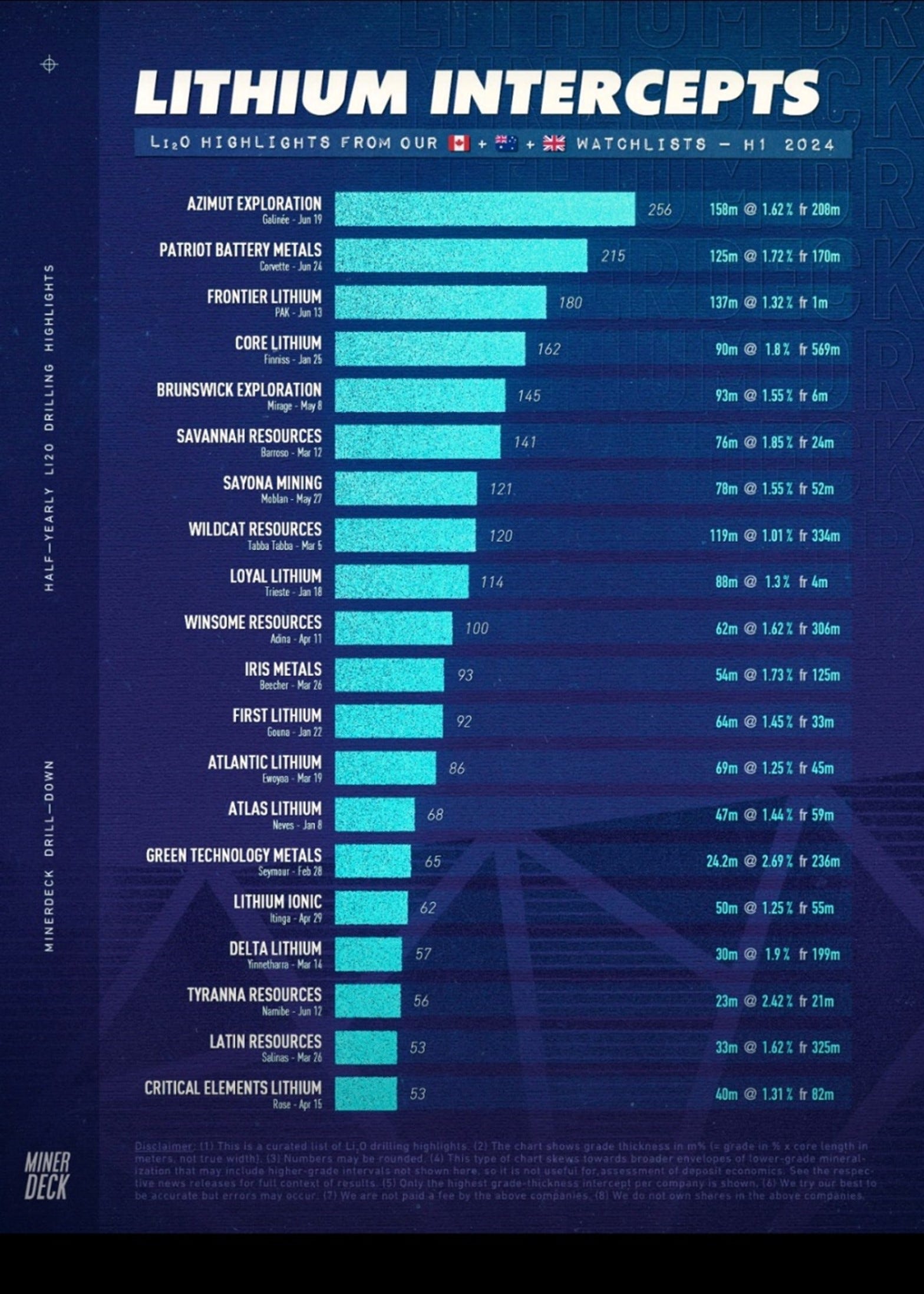

I initially bought Azimut as it seemed like it was going to find gold. However, it later made a good lithium discovery now funded by SOQUEM. In fact, they possibly made the top lithium drilling intercept worldwide in the first half of 2024.

Top lithium drill intercepts in the first half of 2024. Minerdeck.

The firm has an active 2024 with drilling planned at Galineé, Elmer and Pilipas properties.

Azimut properties and details. News releases and investor presentation.

Another thing I like about Azimut is that a lot of their projects are optioned to other firms, that cover a lot of the costs. This reduces the dilution of shareholders as less shares must be issued.

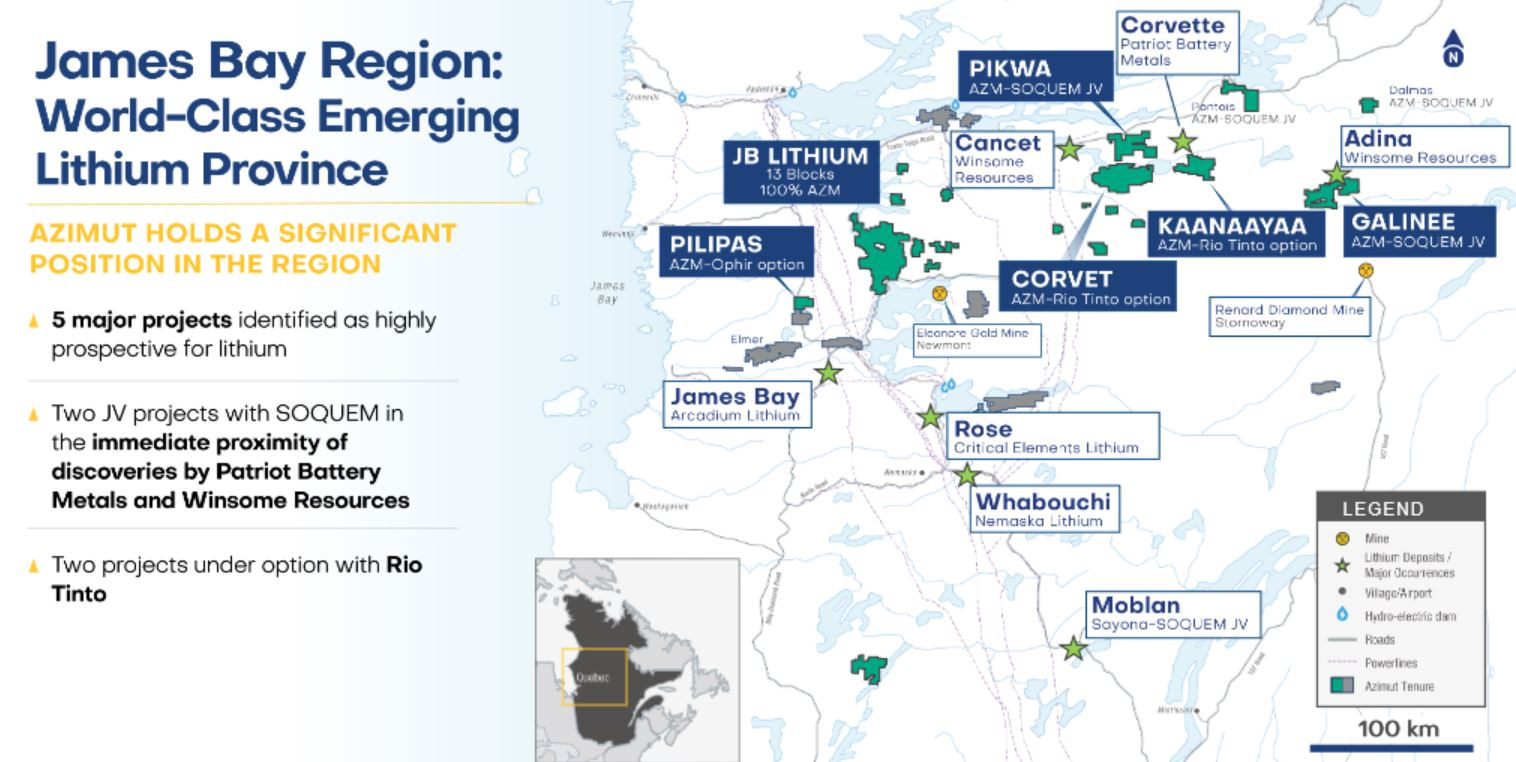

Im excited about what will they find at Galineé and Pilipas. The James Bay region in Quebec is turning out to be a great jurisdiction for lithium exploration. And this has attracted the attention of SOQUEM, KGHM and Rio Tinto, Rio and KGHM being two of the largest mining firms worldwide. SOQUEM and Rio have JVs with Azimut. KGHM has the option to enter a JV with Azimut.

James Bay map, Azimut properties. Investor presentation.

Azimut has a solid balance sheet with $6.6M in NCAV.

Management owns 5% of the firm and Agnico owns 12%.

The CEO Jean-Marc Lulin has ample experience in exploration. He has made several discoveries in Africa. And most importantly, he is an experienced geologist in Quebec. The Chair of the Board is the founder of Abitibi Royalties.

Inflection Resources: Massive drilling program in Australia

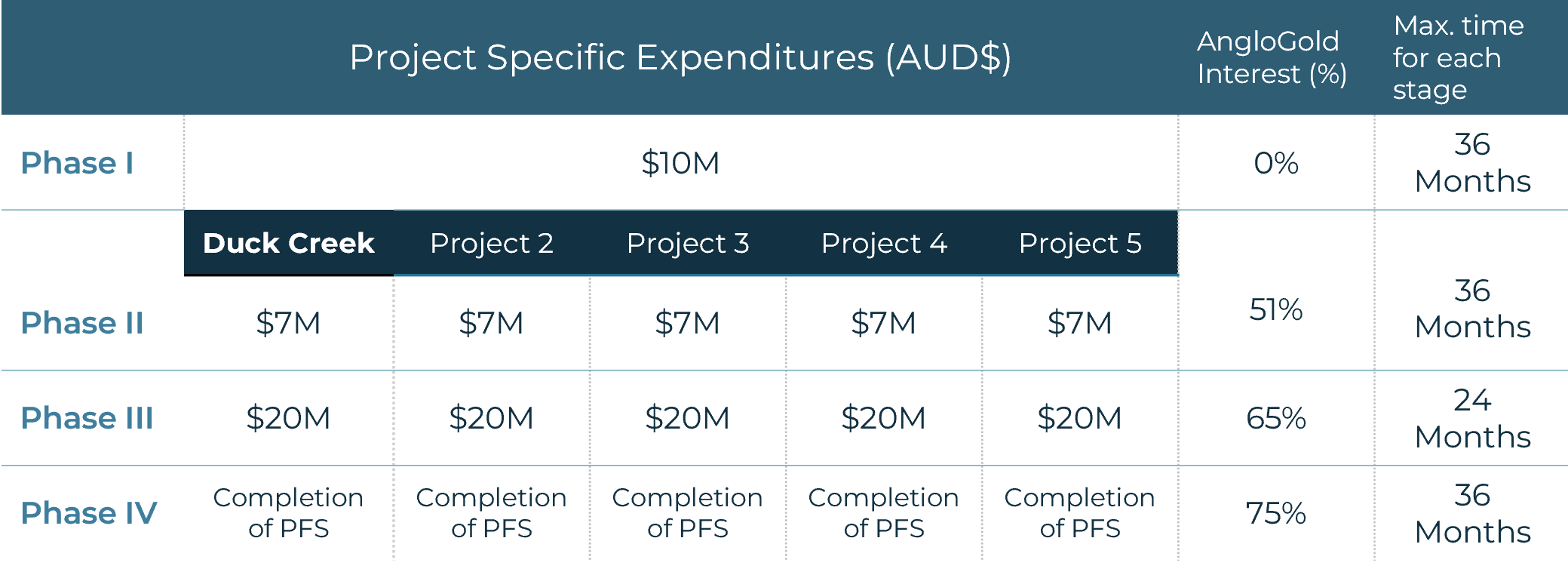

Inflection is undergoing a massive drilling program at their project in New South Wales. 20,000m to 25,000m of drilling is expected for 2024. The best part of it, is that AngloGold is fully funding the project. I expect more drilling in 2025 as AngloGold is very happy with the results so far.

Prove of this is, is that AngloGold is going into phase II for the Duck Creek project.

AngloGold-Inflection JV details. Inflection website.

Furthermore, Inflection is the operator of the JV. For which they earn a 10% fee. This helps the firm with the burn rate and keeping dilution low. Nevertheless, Inflection has $1.18M in NCAV, enough capital to avoid issuing more shares.

Project details of Inflection Metals. Investor presentation.

The company has a massive land package of over 700k ha, which attracted the attention of Anglo. With over 20,000m planned for 2024, all funded by AngloGold, Inflection has plenty of catalysts for a stock rise or the opposite if results aren´t good.

Wendell Zerb the Chairman was president of Exeter Resource which got taken over by Goldcorp in 2017. Which indicates he can create a project that gets the attention of major mining firms.

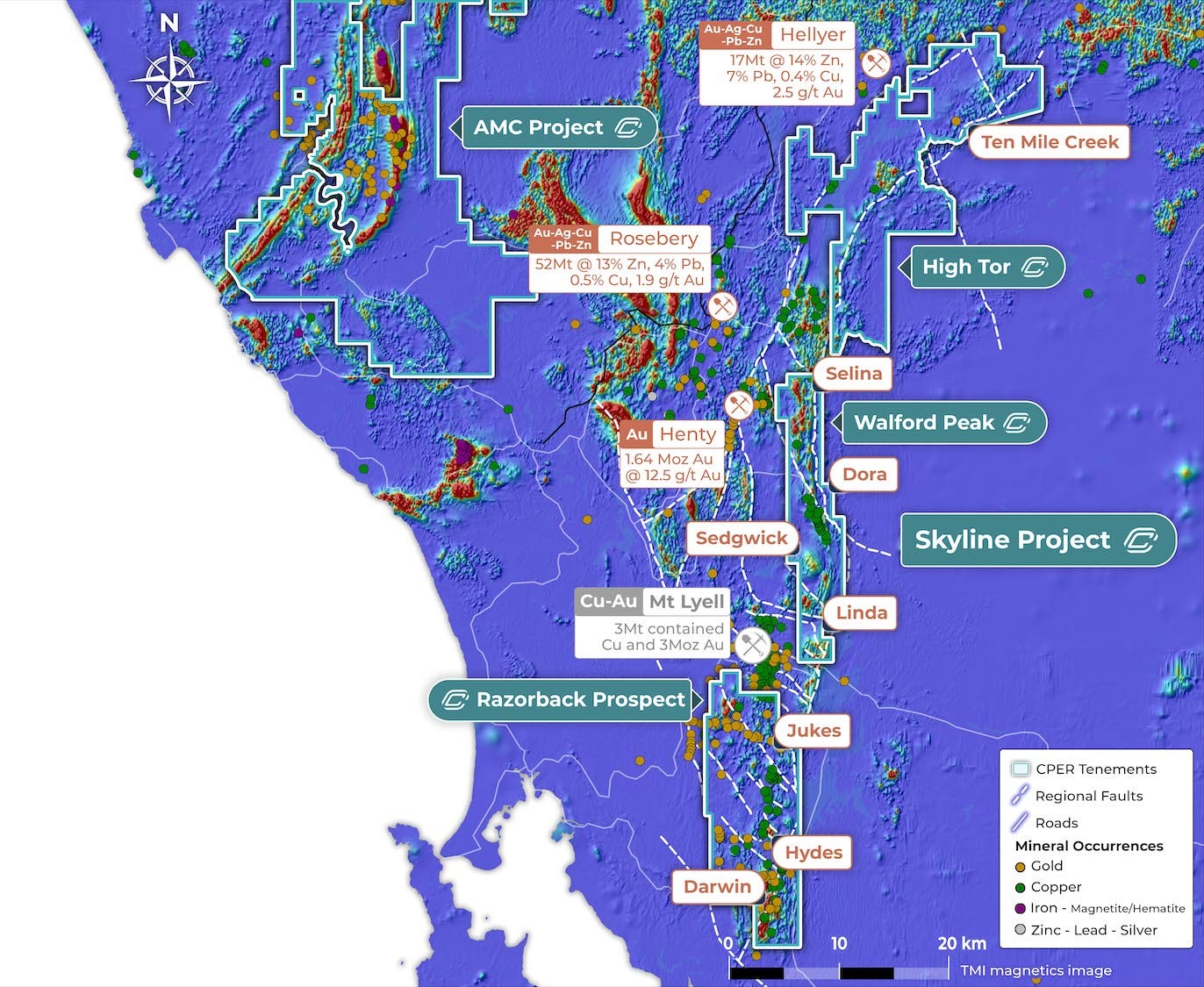

Coppercorp Resources: An explorer with a massive land package trading for almost net cash

CopperCorp project details. CopperCorp website.

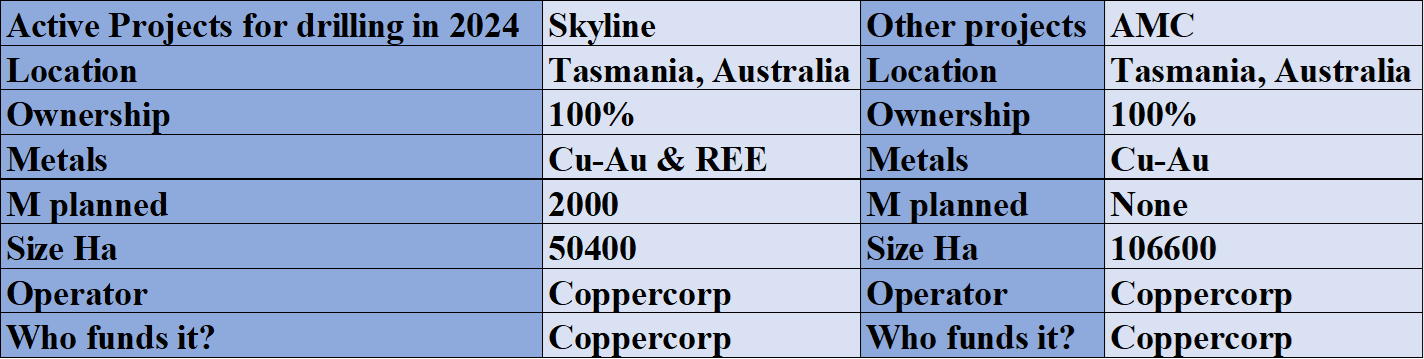

Coppercorp is planning 2000m for their Skyline project in Tasmania, Australia. Furthermore, the firm has $3.52M in NCAV.

CopperCorp map of projects. Corporate website.

The Skyline project, in which drilling is taking place is nearby the Mt Lyell project (Sybanye Stillwater), Henty project (Catalyst Metals), Rosebery mine (MMG) and Hellyer project (EnviroGold Global). Both MMG and Sibanye are large miners. Therefore, if CopperCorp finds some big copper, gold and/or rare earths deposits, there will be candidates for a takeover.

The CEO, Stephen Swatton, is an experienced explorer. He was the CEO of Fortress Minerals which eventually became Lundin Gold. And he was Head of GeoTechnical Division for BHP for over 3 years. Sean Westbrook, the VP of Exploration & Founder of the firm, is a local Tasmanian and has more than 20 years of experience on local geology.

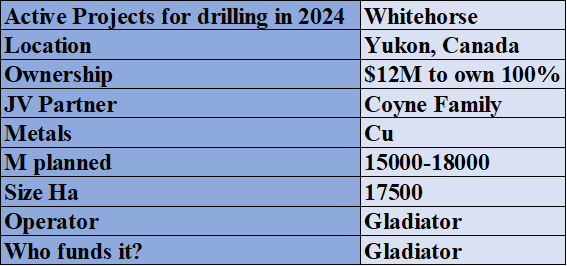

Gladiator Metals: Big drilling program in the Yukon supported by the Coyne family

Project details of Gladiator Metals. Corporate website, own estimates.

The company is fully funded to get 100% of the project by spending $12M in the project. And they are planning anywhere between 15,000m and 18,000m of drilling for this year.

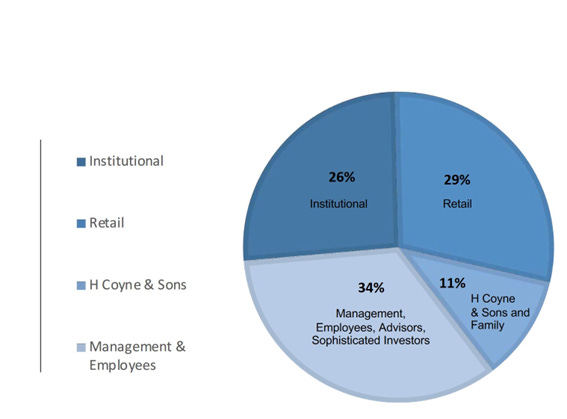

Ownership of Gladiator Metals. Investor presentation.

More importantly the company is owned 20% by management. And 11% by the Coyne family. A family who owns a mining business (kluanedrilling.ca) and is helping Gladiator with the drilling, thus bringing the drilling costs down.

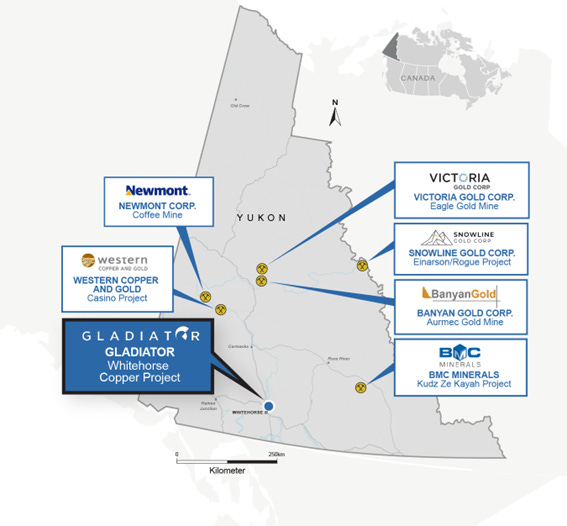

Yukon map. Gladiator Metals website.

Notice the project is far away from the Victoria Gold mine, which had an environmental disaster recently. However, I’m somewhat concerned the project is close to Whitehorse city. That said, the Coyne family is part of the Kwanlin Dün First Nation, which sits within the Whitehorse project. Therefore, I think the locals are in favour of the project.

Drill results released in December 2023. Gladiator Metals.

The company has already achieved great drill results. And with the large drilling program ahead, exceptional copper results could be obtained.

Kell Nielsen, the VP of Exploration has been involved in the discoveries of the Ngualla Rare Earth Deposit (Tanzania), the Selenge Iron Project (Mongolia), the Diamba Sud Gold Project (Senegal), and multiple projects for Placer Dome including the delineation of the Wallaby Gold Mine (~7Moz Au, Australia).

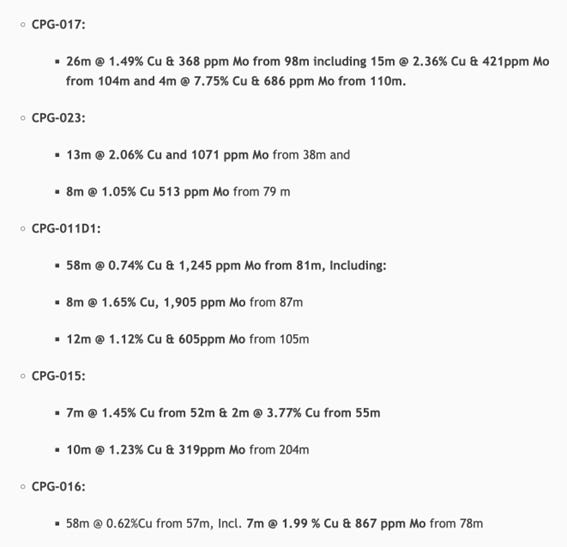

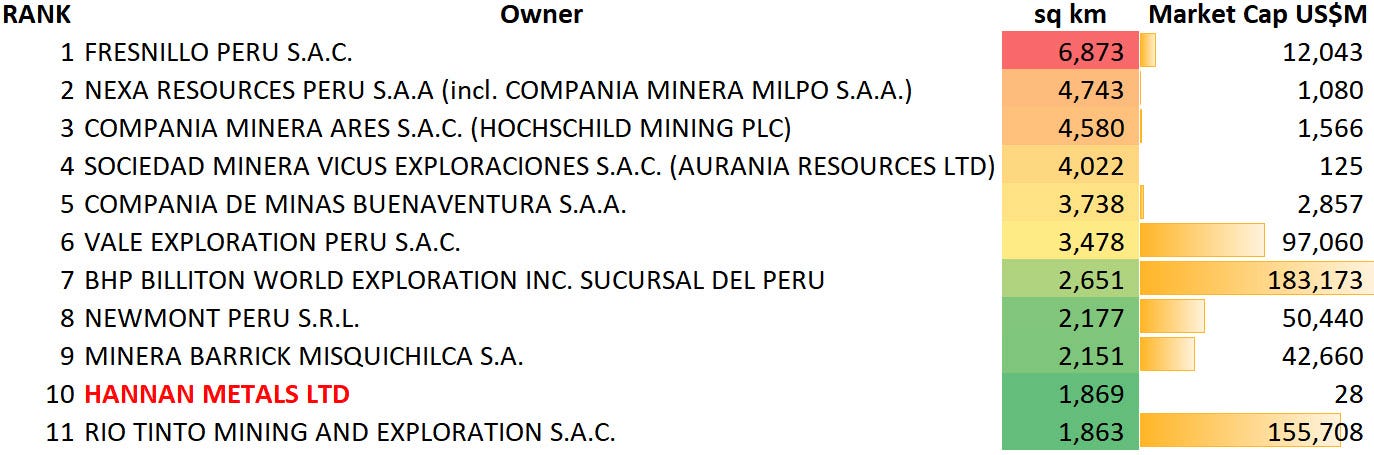

Hanna Metals: A micro-cap who is one of the largest mining landowners in Peru

Largest mining landowners in Peru. Old Hannan investor presentation.

The chart above is a bit outdated, now Hannan owns around 1686 square km in Peru. But it’s the only micro-cap in the list together with Aurania Resources. However, Aurania has since shifted its focus towards Ecuador.

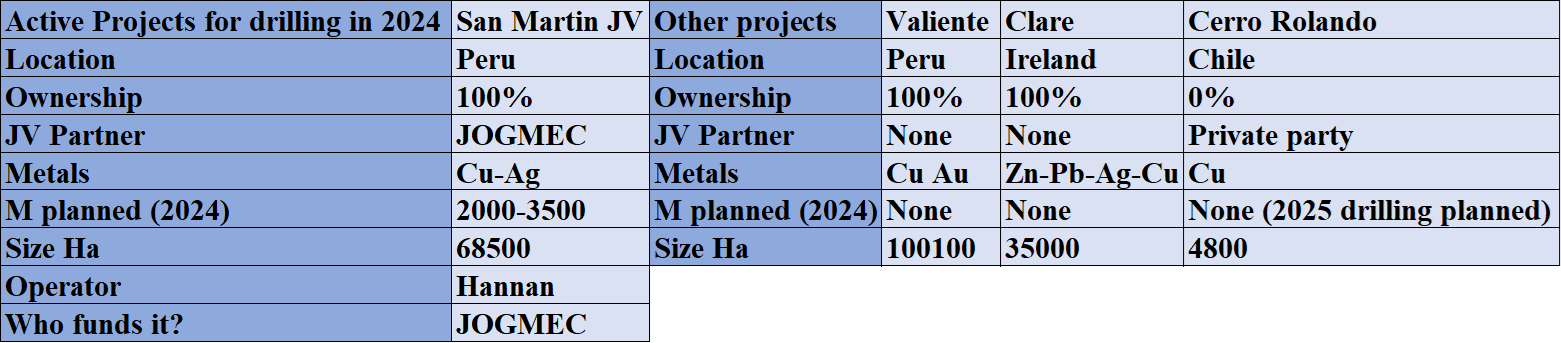

Hannan project details. Investor presentation.

The company is planning drilling at their San Martín JV. Anywhere between 2000m and 3500m is planned. This will all be funded by JOGMEC, the Japan Oil, Gas and Metals National Corporation. JOGMEC is one of the largest players in the mining business. They own smelters in Japan that require to constantly import copper for its refining. I think JOGMEC is one of the best partners a mining firm can have, as they plan decades ahead and are very patient.

Under the agreement between JOGMEC and Hannan, JOGMEC can earn 51% after spending $8M, and 75% after spending $35M to deliver to the joint venture a feasibility study.

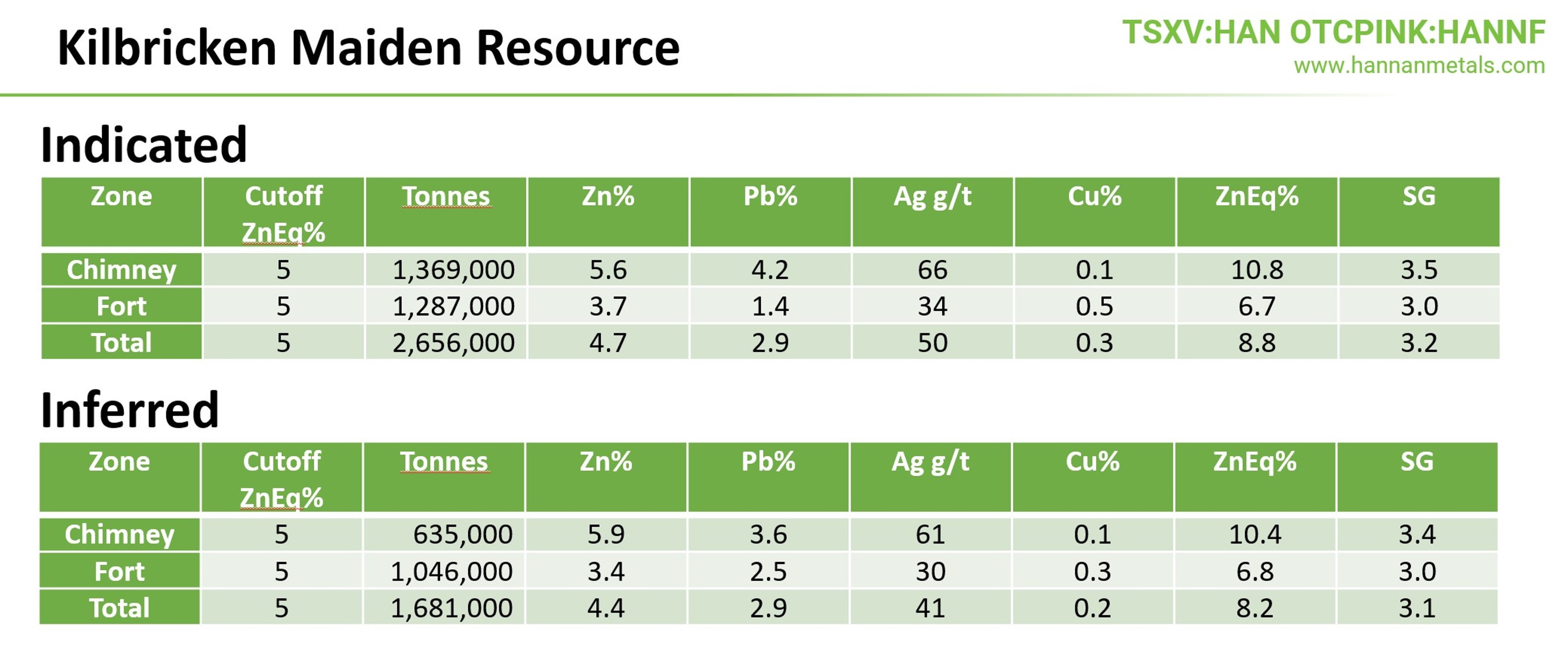

Kilbricken resource. Hannan website.

Like Radius, Hannan is one of the few explorers who has a resource already. It´s in Ireland, one of the few countries in Europe that are friendly towards mining. It’s a high-grade zinc and lead deposit.

Management owns 14% of Hannan and the firm as $3.46M in NCAV. Michael Robert Hudson, the CEO and Chairman of Hannan is a very experienced geologist. He has made several discoveries worldwide, including in Peru. He is Chairman at Mawson Gold, a $200M market cap gold firm.

Conclusion

All the firms mentioned in the report are part of my portfolio. I own 1% of my portfolio into each one (more or less) of them except Goliath and Aurion. Aurion is my largest investment in exploration followed by Goliath.

I am fully aware that in the long run exploration firms are very bad at capital allocation and investor returns. In that sense I will be very reactive to the results of their drill programs. If the results aren´t what I expected I will sell and I will let you know in the Substack chat.

Furthermore, I don´t like to have many firms in my portfolio as I don´t think diversification is wise for full time investors. Therefore, as I sell my investments in exploration firms, I will redirect that capital into my top picks (Manolete Partners, Ero Copper, gold stocks and Platinum Group Metals developers).

I want to thank my girlfriend Yeimy, who has helped me a lot at home while I was researching this by myself. This report and this blog would not be possible without her. Thank you.

Any feedback is welcome in the comments, or you can send me a message on Substack or through my twitter account @AAGresearch.

I hope this finds you well,

Alberto Álvarez González.

Gracias por compartirlo, tus trabajos son entretenidos... fascinantes incluso!

Thank you Alberto ,for the article! Great resource for learning about the mining industry.🙂