Analysis of every medium sized gold company worldwide & AMRK

Analysis of every medium sized gold company worldwide & AMRK

Deep dive into the details of every medium sized producer, developer and gold broker

Introduction

On April the 4th I wrote a report on gold and my thesis about its scarcity. I also touched on the important macroeconomic and historical situation the metal is facing and all these factors were very bullish for gold. Since I wrote my report on April, I have not been very active on Substack nor Twitter (X). In fact, I have only written 2 reports: an update for Ero Copper (my top pick for the copper thesis) and an update on Manolete Partners, a value investing opportunity, and my largest holding in my portfolio.

On that report on April the 4th I promised you a report on mining firms, which is what has taken most of my time for the past 2 months. I have research over 800 mining firms in all segments of the mining business: mining services, brokers, metal producers, developers, and exploration firms. From these 800 firms I have selected and bought shares in 4 companies. However, I have included dozens of them in this report for all of you to be better informed about various projects and firms.

Important side note: all the companies you will see in the report fit all the criteria I have set. Furthermore, when selecting which data to present to you, I chose to be extremely conservative: I chose the highest range of the operating costs, from the range presented by each company and the lowest production guidance in the range each company shows. All the numbers in the report are in US Dollars. When reading the 400 page long economic studies of each company in this report, I always chose the highest interest rate possible, since I know the banks will not lend money to junior miners at less than 10% interest rate. When investing I like to see upside, but even more than that I like to see very little downside. So, I always prefer to take the role of the devil’s advocate and assume that the company will produce less than guidance, and have costs higher than guidance. I hope you agree with me.

Summary

In this report I have analyzed every small and medium sized gold miner and developer worldwide I have found. I have also analyzed the two main precious metals brokers that trade in the stock market. I am sure I have missed some firms, if you think I have missed a stock that fits the criteria mentioned in the first section of the report, please let me know in the comments and I will add them.

To reduce the number of firms in my investing universe I decided to set some boundaries, which you can find in the next segment of my report. If there is interest among subscribers and I can find something interesting, I am more than happy to explore opportunities outside those boundaries.

My picks for the sector from less risky to most risky are A-Mark Precious Metals (NASDAQ: AMRK) (top pick), Liberty Gold (TSE: LGD),

Medallion Metals (ASX: MM8)and Aurion Resources (CVE: AU). I have since sold Medallion to buy into Boab Metals (ASX: BML), click here for report on the sale: Selling a gold stock to buy into a silver projectAMRK is by far the best option to play the gold thesis, as it offers a lot of leverage on gold prices increasing and demand rising.

Liberty Gold has 2 gold projects in the US and is about to release the PFS on their Black Pine project. Even if they underdeliver on the PFS I believe Liberty trades at massive discount to NPV.

Medallion trades at a 95% discount to NPV which is not reasonable considering the quality of the project and its location (Western Australia).

Aurion owns almost all the land adjacent to Rupert Resources, who owns possibly the best project worldwide in terms of economics and size. I´m expecting similar results from Aurion.

Unfortunately, I have found no gold producers worth investing in. Gold producers are either overleveraged, losing money at these prices or their reserves are diminishing, which will force them to spend money on CAPEX or M&A, instead of shareholder returns.

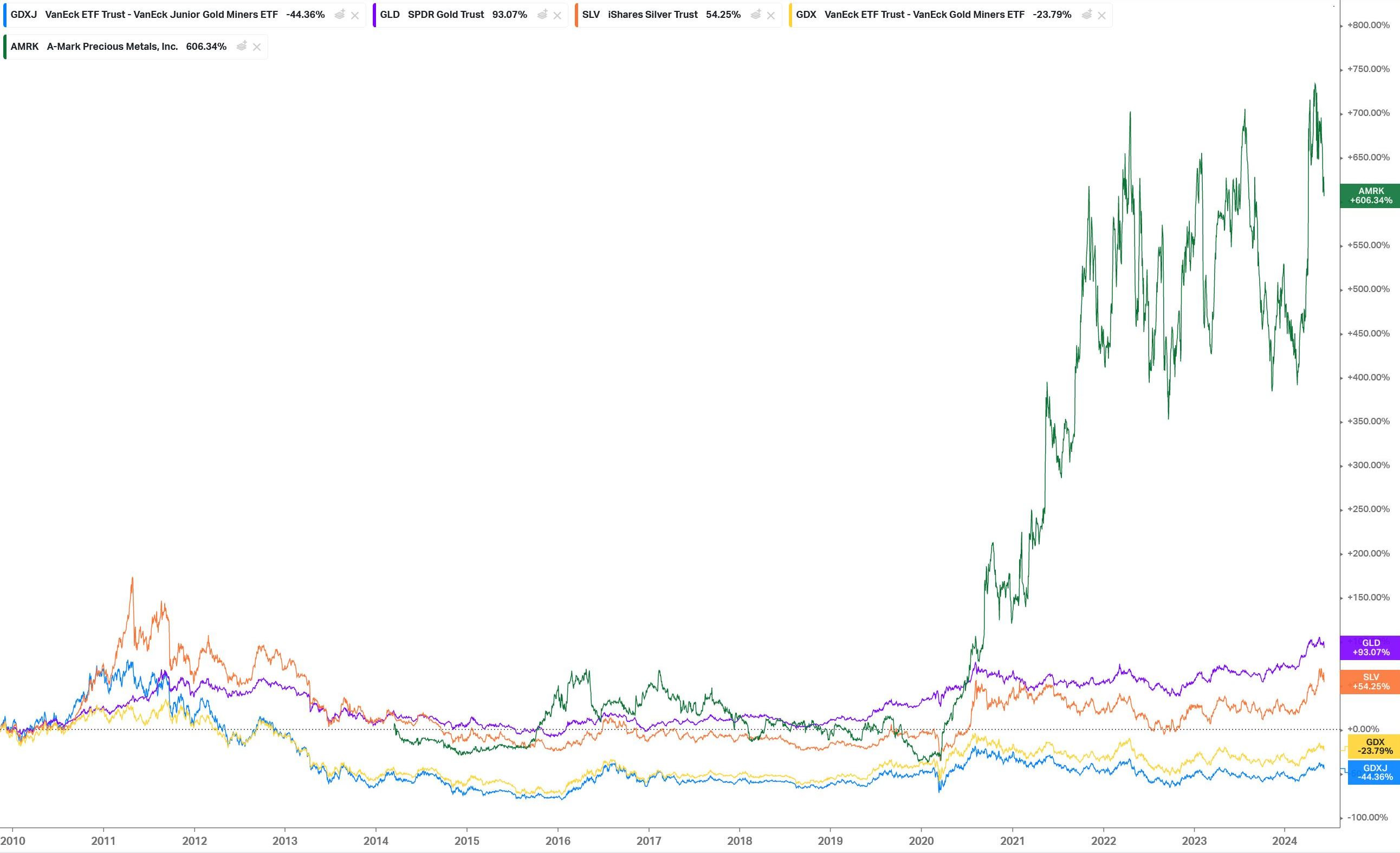

Returns of gold, silver, GDX and GDXJ vs AMRK. Koyfin.

Glossary of terms

Glossary of terms.

Boundaries/criteria of my analysis

Boundaries/criteria of my analysis. And some companies I excluded.

Before explaining my boundaries, I would like to remind you of the thesis I explained on my report of April the 4th. Although I highly recommend reading that report before continuing the reading of this report. Here is my thesis: Mining companies are running out of reserves very soon, possibly in less than 10 years depending on output. Therefore, there is massive scarcity of medium to large sized projects. I believe soon there will be a bidding war for this kind of projects and I want to position myself accordingly.

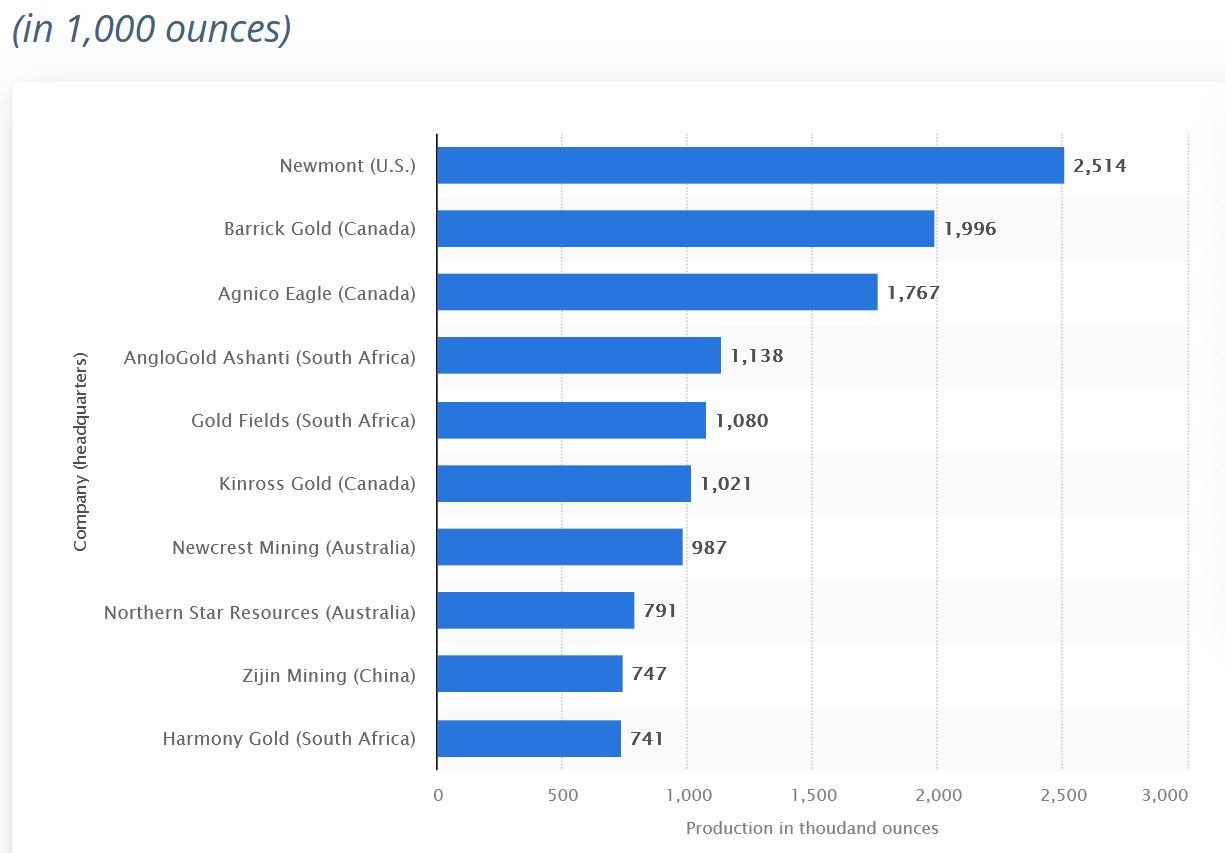

The first limit I set to my analysis was that the companies I found needed 40,000 a year of production, either future production (development project) or present production (miner). The logic behind this limit is that the largest mining companies, which have the deepest pockets, produce anywhere between 1.5M ounces (like Harmony or Zijin) and 5M ounces a year (Barrick or Newmont). And for this companies to buy a firm or a project or producer that will produce less than 40,000 ounces a year really doesn’t make sense, because it won’t move the needle in the bottom line of the income statement. I want to own a project for which many mining companies will be interested in once reserves deplete. Under each limit or premise I have listed which companies have been excluded. Of course, a lot more have been excluded than those that appear there. But I just mentioned the ones I thought were worth mentioning, or the ones that subscribers asked me to analyze.

Top gold mining firms by production. Production data of H1 2023.

The second limit in my report was to set a boundary on the market cap of the firm. This was a tough one because large miners will seek large projects in development and these projects often have large market caps behind. However, the larger the firm the more followed it is. And therefore, it’s tough to buy it at a good price. As a result of this I decided to set a boundary at $1 billion market cap (give or take).

Thirdly, I set a limit for the life of mine of the development projects I was looking at. As Rick Rule says: “A large mining project and a small mining project have exactly the same risk, so why bother with small projects.” I guess the same logic crossed my mind when I set the limit at 40,000 ounces of production per year. Bear in mind that large miners will also have the same logic when taking over a firm. Why would they be interested in a project that will only last 4 or 5 years? Building mines is almost rocket science and the execution risk is massive, so I doubt takeovers will have as target firms that own projects with a short life.

To value the firm, I needed an economic study done. Therefore, any firm in development but without an economic study couldn´t come into this report. I do own some exploration firms and development projects, but I prefer to analyze those on a different report as they are different beasts. Therefore, exploration companies aren’t included in this report either. Aurion is somewhere in between exploration and development, therefore I decided to include it in the report.

Another important premise I set, was that revenues from the project or the miner had to be at least 50% sourced from gold. We are looking for gold leverage here so companies like Endeavour Silver just did not fit the report.

Finally, I decided to exclude firms that posted their results on a pretax basis only in their economic reports. I believe the true economics of a project is measured after tax, so I don’t agree with the philosophy of companies posting results pretax.

A-Mark Precious Metals vs GoldMoney (TSE: XAU)

The two main publicly traded brokers and gold custodians in the precious metals space are AMRK and XAU.

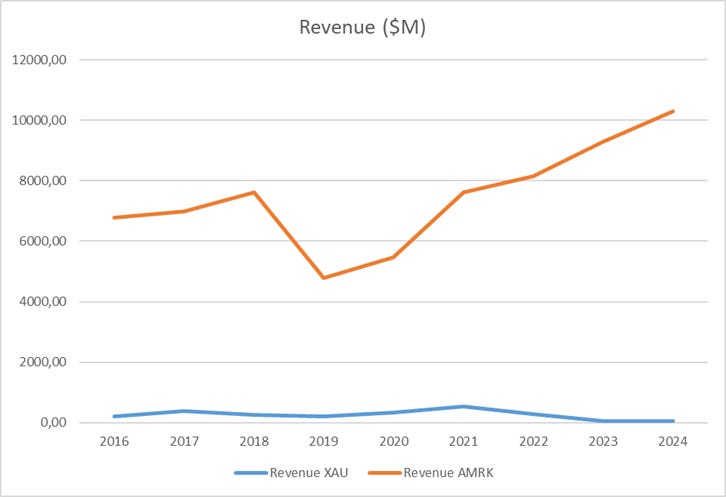

Revenue of GoldMoney vs A-Mark Precious Metals. Financial statements and own estimates.

In terms of size there is no doubt that AMRK is the largest one, both in terms of revenue and market cap. AMRK has grown very aggressively through the past 6 years and XAU has not. I have known XAU for many years, and I always liked their model and their services. However, they have now diversified into Real Estate, and they sold their partnership with Schiff Gold which I think are both big mistakes. AMRK has instead invested in M&A to takeover other gold brokers. I believe Schiff Gold was a good partnership for XAU as Peter Schiff is very well known in the gold space and has a good brand.

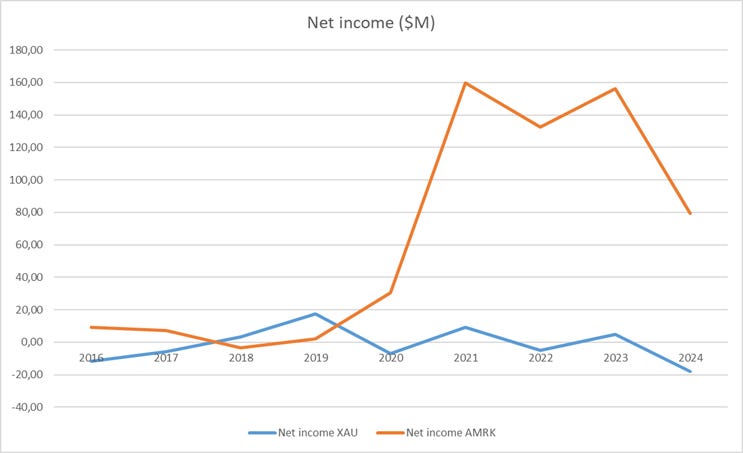

Net income of GoldMoney vs A-Mark Precious Metals. Financial statements and own estimates.

In terms of profitability AMRK has overtaken XAU as can be seen in the image above. AMRK has grown their net income at a hoping average of 117% per year. XAU on the other hand has grown net income at an average of 8% per year. When it comes to historical margins XAU has somewhat better margins, but this doesn’t justify the lack of growth, nor the lack of shareholder returns. XAU trades near all-time lows whereas AMRK trades near all-time highs.

When it comes to balance sheet, XAU has a better Debt/EBITDA at 2.09 whereas AMRK has 6.75. However, AMRK has gone into debt to grow their core business, positioning themselves to exploit the increase in gold demand. Furthermore, the net current asset value (NCAV) of XAU is of $-19.2M which can lead to problems in the short term if their operating income does not do well. AMRK on the other hand as an NCAV of $266.7M which gives them great margin of safety and flexibility if more growth opportunities arise. As a result of this, I chose AMRK for my valuation.

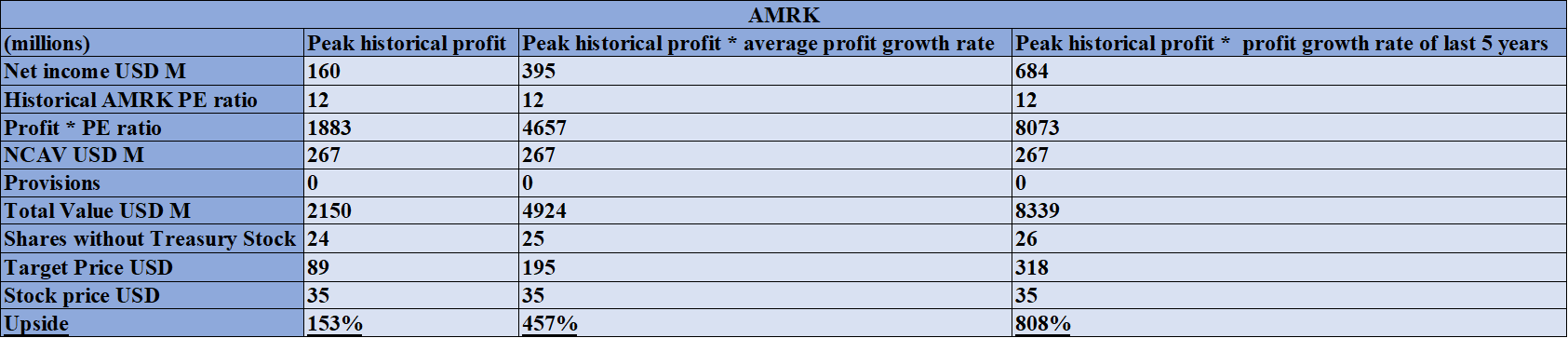

Valuation of A-Mark Precious Metals. Financial statements and own estimates.

My valuation above offers 3 scenarios: 1. Assumes AMRK will have their peak historical net income (Upside of 153%). 2. Assumes AMRK will have their peak historical net income plus their average historical growth rate: 117% (Upside of 457%). 3. Assumes AMRK will have their peak historical net income plus their average net income growth of the past 8 years: 371% (Upside of 808%).

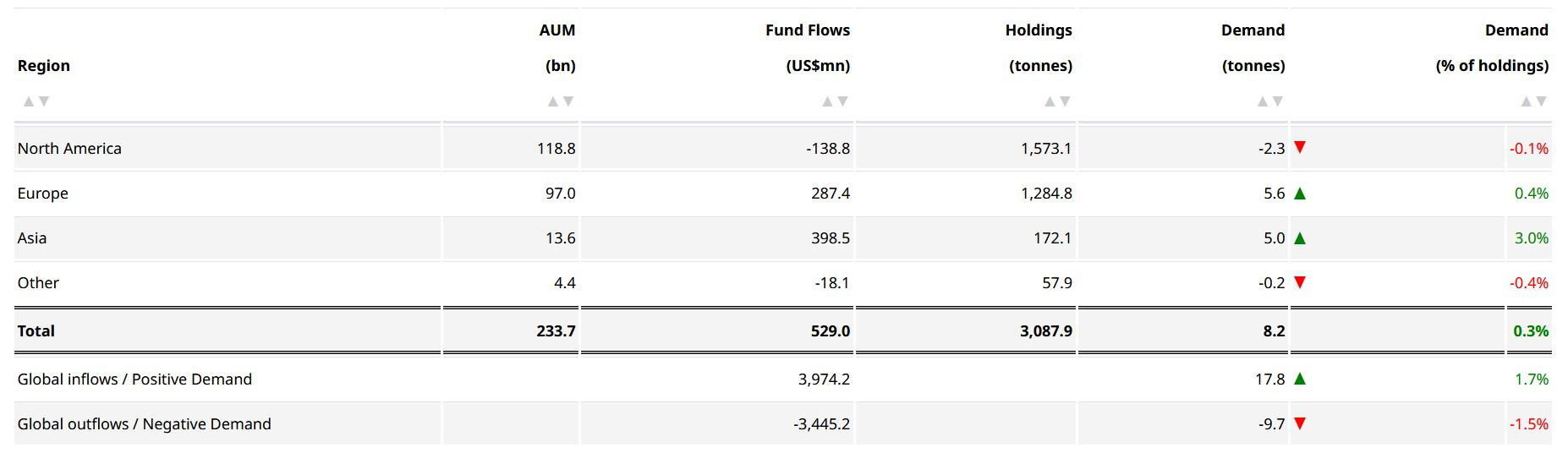

Flows in gold ETFs. World Gold Council. May 2024.

Gold ETFs have enjoyed inflows recently and I believe this is just the beginning of the cycle for precious metals. Therefore, I think that the possibility of AMRK growing at the rate shown in scenario 3 is not too farfetched.

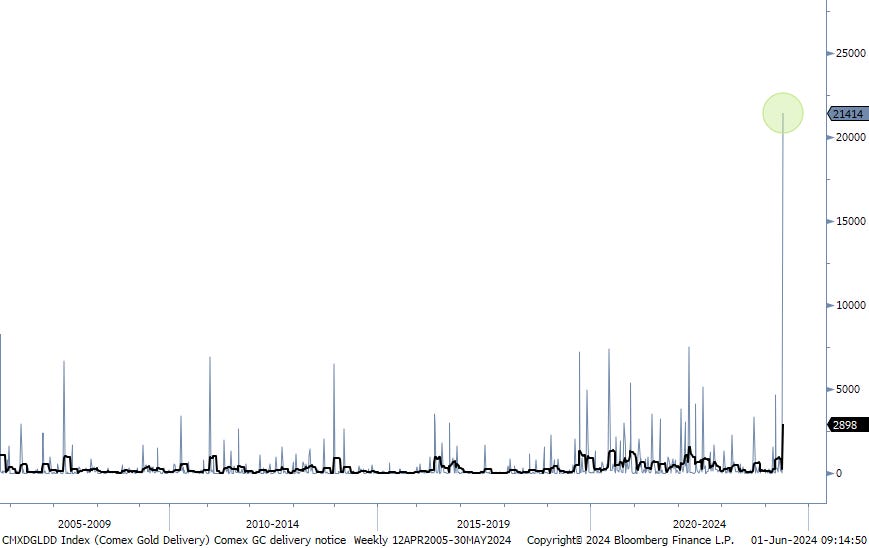

Gold deliveries for gold futures. COMEX, Bloomberg.

For decades gold futures were settled in dollars as holders did not wish to have gold delivered to them. On Friday the 31st of May the largest delivery ever occurred at the COMEX: 2.14M ounces. This further supports the evidence that investors are seeking physical gold. Which will help the business of AMRK. I hold a large position in AMRK through an account I manage, and I also own it on my personal account.

Deep dive into Liberty Gold

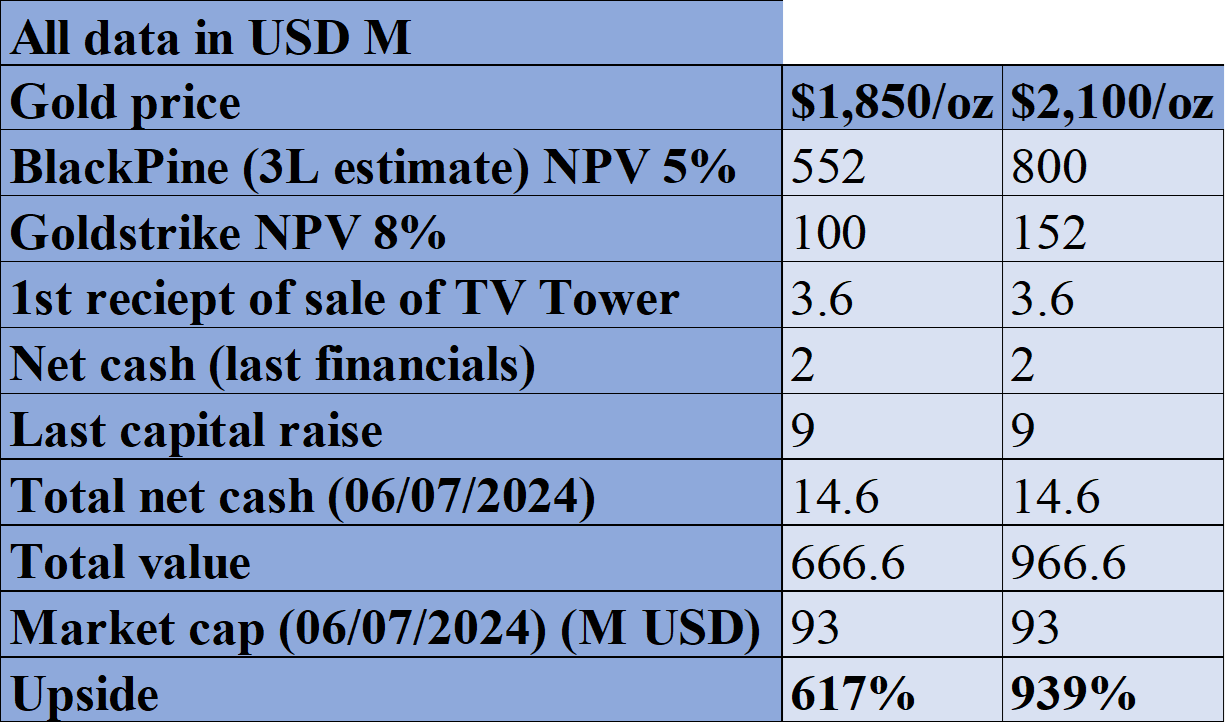

Liberty Gold valuation. Mining economic reports, own estimates. 3L Capital.

Liberty owns 3 projects: Black Pine, Goldstrike and TV Tower. They just sold TV Tower in Turkey for $8.3M since it was not a core asset for Liberty.

Above you can see an analysis on the Black Pine project from 3L Capital, a firm specialized in metals and mining.

I have placed two scenarios for Liberty, one at $1,850/oz and another one at $2,100/oz. As you can see in both scenarios the upside is huge: 600%+ and 900%+ respectively. Even if Liberty underdelivers with the economic study at Black Pine, the upside is still large and the downside very limited. I expect the delivery of the economic study in Q4 2024.

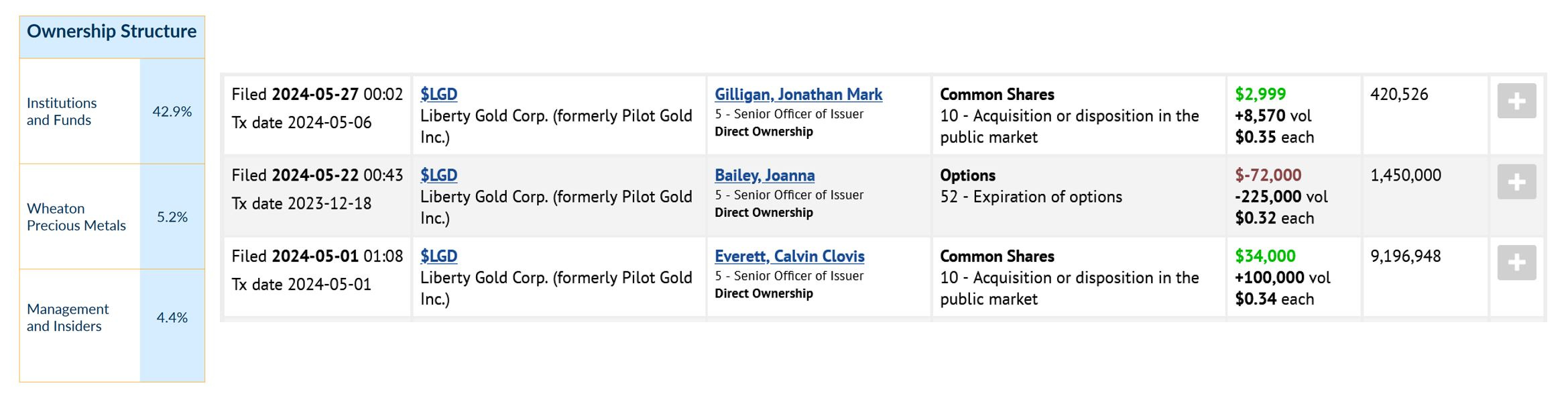

Ownership of Liberty Gold and insider purchases. Liberty investor presentation & SEDI filling.

Management owns over 4% of the business and they have been buying recently. It’s always positive to see an insider buying shares. More so considering management has not purchased shares for a while.

I own shares in Liberty Gold.

Deep dive into Medallion Metals

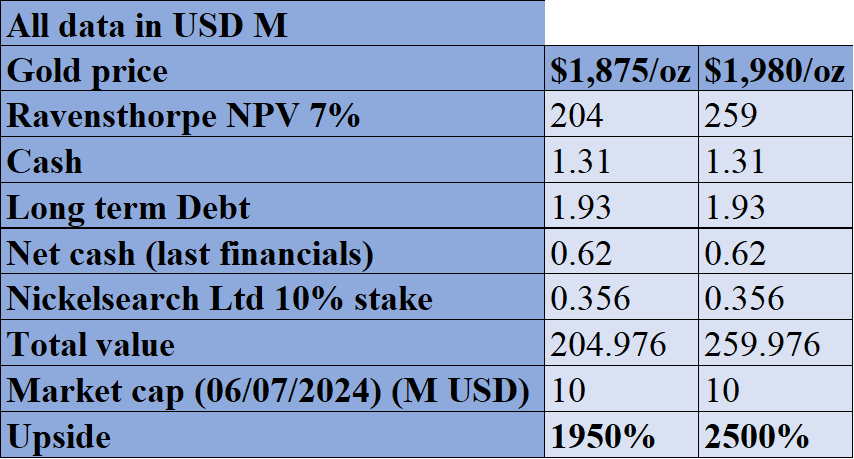

Medallion Metals valuation. Mining economic reports and my own estimates.

Medallion Metals owns two projects: Ravensthorpe and Jerdacuttup. Ravensthorpe has an economic study done on it and has an NPV after tax of $204M at $1,875/oz and it will produce gold at an AIC of $1,263/oz of gold. It will produce both gold and copper and I don’t think the market is giving Medallion any value for this project. Medallion trades at a 95% discount to NPV. The discount is even higher if we factor in net cash and their stake in Nickelsearch, a lithium and nickel explorer.

Medallion annual report. Insider ownership.

Insiders own around 3% of the company. And the top 20 shareholders (not including Paul Bennett) own over 71% of the company. John Fitzgerald is the non-executive director of Northern Star Resources a $10B market cap miner.

This company reminds me of Vimy Resources in 2020. A uranium company that was trading at 90%+ discount to NPV. I ended up making a 1229% return on Vimy. And later, it got acquired by Deep Yellow. I’m not sure if Medallion will deliver similar returns but that upside sure gives us a lot of downside protection.

I own shares in Medallion Metals.

Deep dive into Aurion Resources: The next Rupert Resources?

Rupert resources stock. Google finance.

Rupert resources has one of the best gold deposits in the world. Hosting a $1B+ NPV (10%) deposit that will produce 200,000 ounces of gold per year for 22 years at $759/oz AISC. The CAPEX will be of $405M. The deposit is very high grade, and the recovery rate is of 95%, very high.

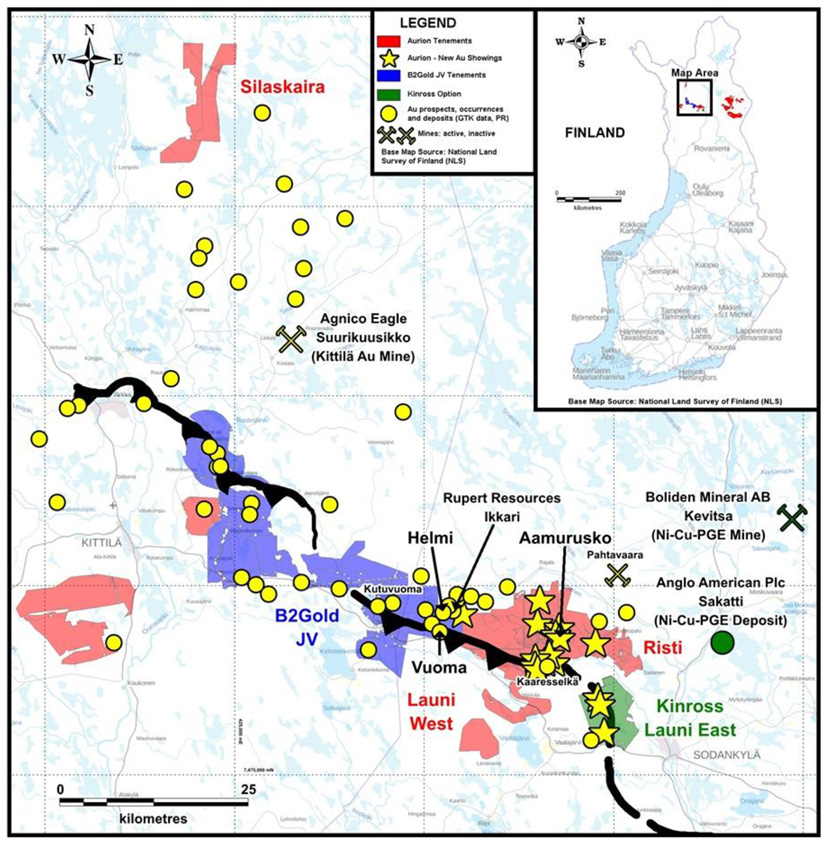

Aurion resources investor presentation.

My way to play the thesis of Rupert is through Aurion Resources. Rupert owns the Ikkari deposit. And as you can see in the map above Aurion owns almost all the land adjacent to Rupert. It owns it either through its 100% owned tenements or through a JV that Rupert has now acquired from B2Gold.

I am not going to try to give a valuation to Aurion because it would be impossible. But the chances of them continuing to find gold is extremely high.

They have 2 JVs. One with Kinross in which Kinross will have to spend $10M to earn 70% of the JV. And another one with Rupert. I think both Aurion and Rupert will consolidate sooner or later, and they will be taken over by a large mining company. But this is just speculation for now.

Management owns 12.7% of Aurion. Kinross, Newmont, and Eric Sprott own another 15.4% all together.

Just in January and March of 2024, the CEO of Aurion, David Lotan, bought 200,000 shares. And he now owns over 13.4M shares of Aurion. He is a specialist investor in mining, he was the portfolio manager for the Ontario Teachers' Pension Plan for a year. And he is the CEO of LHI Capital.

I own shares in Aurion Resources.

For those of you not familiar with David Lotan I highly recommend you his presentations at the PDAC in 2024. Link Below.

Keynote Speaker: David Lotan | Red Cloud's Pre-PDAC 2024

Gold development firms

Due to the sheer number of firms I have analyzed, I have had to separate them by listing location (NYSE, ASX, LSE and TSX) and ordered them by market cap. For you to read them more easily I have decided to put around 4 stocks on each table, please bear with me because I have put the data of dozens of companies into my report. Consider that when you see 5% interest rate in my tables that means that the company didn’t do interest rate analysis in their PEA, PFS or scoping study. Otherwise, I always chose the highest interest rate possible, searching for margin of safety.

Canada listed gold developers

Canadian developers <$30M market cap

Data on Canada listed developers<$30M market cap. Mining economic reports (PEA, PFS) and my own estimates.

From this first list the only one that struck my interest was Goldsource (now taken over by Mako). It interested me because of the high gold recovery rate and the low CAPEX relative to NPV (10%). Furthermore, I always like when a company uses sensitivity analysis of interest rates in their economic studies. However, the company has a high NSR on their property which reduces future profitability. And I am not familiar with Guyana as a mining jurisdiction, so I decided to pass on this opportunity. That said, Mako has probably made a good purchase, as they aim to become a geographically diversified mid-tier gold miner.

Canadian developers <$50M market cap

Data on Canada listed developers<$50M market cap. Mining economic reports (PEA, PFS) and my own estimates.

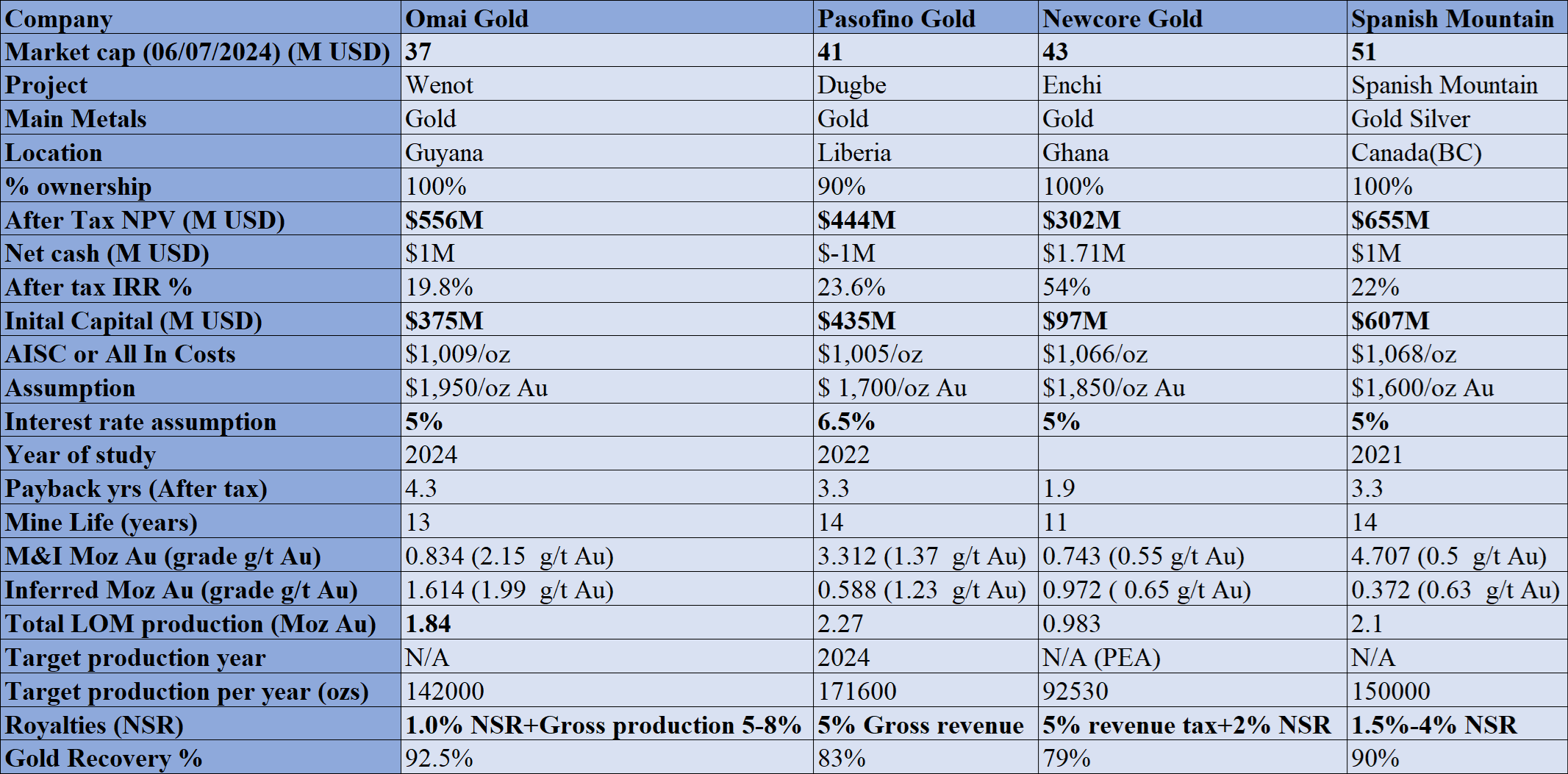

The table above has some very interesting data, specifically from Newcore Gold. Their project has a very large NPV relative to CAPEX albeit at a 5% interest rate discount. However, their economic study had a huge typo, which makes me wary of management and the engineering team behind the economic study. In their economic study they mistakenly put a “k” behind ounces, implying they will produce 89M ounces a year, which is insane if you consider that the entire world produces 110M ounces per year. A big mistake which made me lose my trust in them.

Pasofino has an interesting project, but I don’t trust Liberia as a jurisdiction.

Omai has too many royalties on their asset, which hampers the economics of the project.

Economic study of Newcore gold. Newcore Gold report.

Canadian developers <$80M market cap

Data on Canada listed developers<$80M market cap. Mining economic reports (PEA, PFS) and my own estimates.

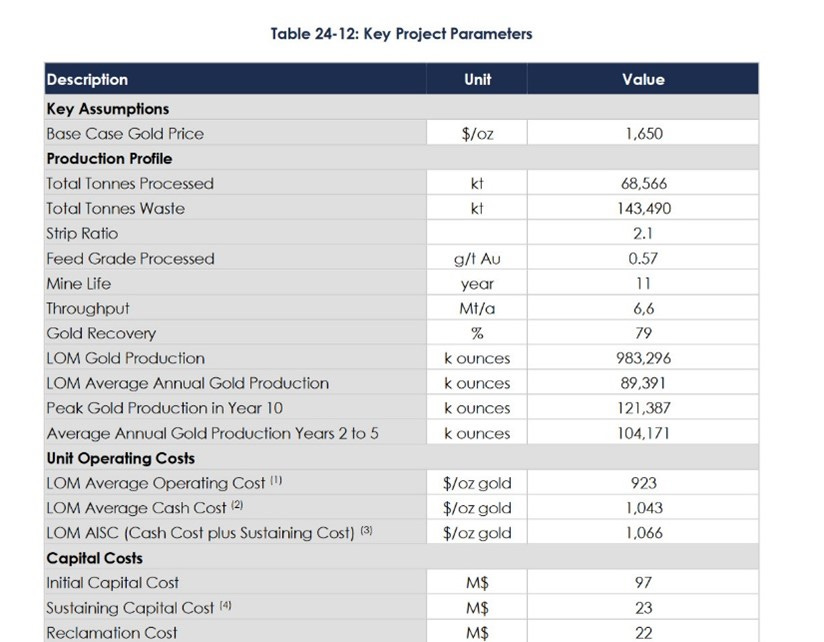

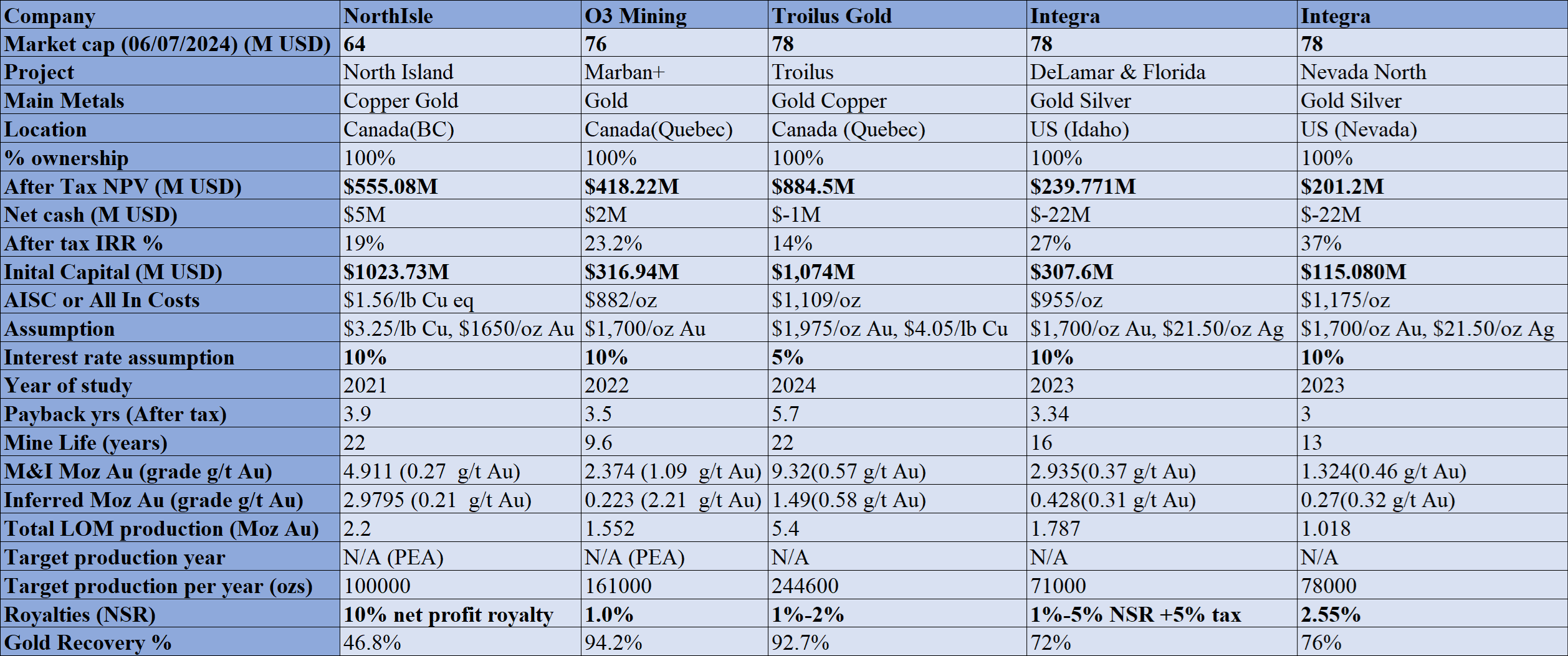

From this set of companies, the most interesting one is Troilus Gold given its long-life span and the 5.4M ounces they will produce in their life of mine. However, their large CAPEX and low market cap, may indicate the market does not believe they will be able to finance the CAPEX of the mine.

I have in very high regard the management of Integra since they show the results of every drill hole. It’s also nice they show interest rate sensitivity in their economic reports. However, I don´t like their balance sheet as they have a convertible bond and a very high burn rate.

Canadian developers <$95M market cap

Data on Canada listed developers<$95M market cap. Mining economic reports (PEA, PFS) and my own estimates.

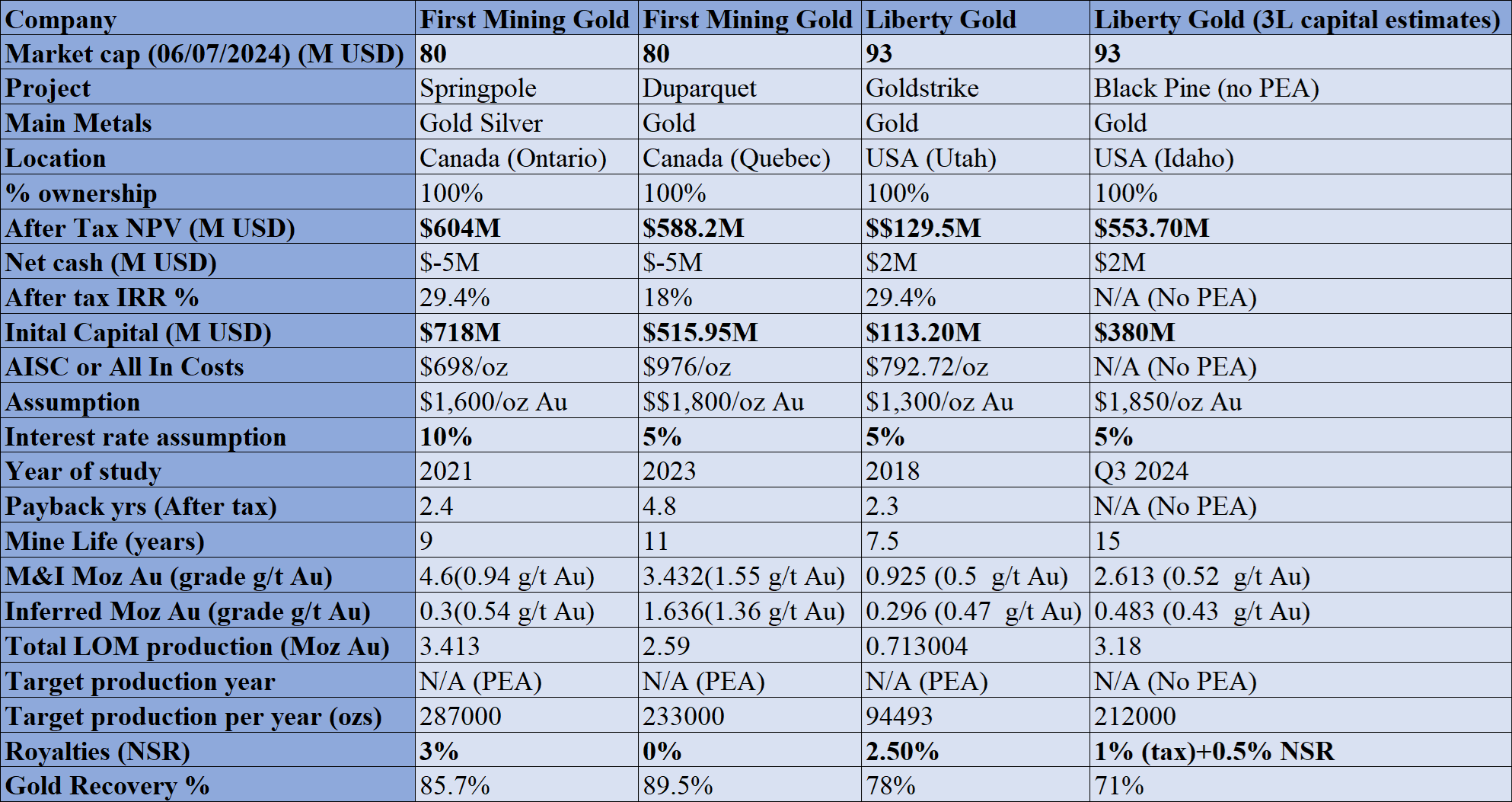

In this set of companies, the one I like the most is Liberty Gold. They have a solid balance sheet and two projects in the US, which is a jurisdiction I like although their politicians sometimes hamper the construction permitting of mines. The Fraser Institute, the most reputable when choosing mining jurisdictions, just named Utah the number 1 mining jurisdiction in the world. I went deeper into Liberty Gold earlier in this report.

First Mining Gold has good projects, but the management of their balance sheet is somewhat deficient as they just issued shares with the stock at all-time lows. And I don´t like the high CAPEX requirements of their projects considering their market cap.

Canadian developers <$110M market cap

Data on Canada listed developers<$110M market cap. Mining economic reports (PEA, PFS) and my own estimates.

From this list my favorite project is Cerro de Oro, owned by Minera Alamos. However, they seem to be trading at a fair value and the royalties on the project will lower profitability.

Rio2 had environmental problems in Chile which explains the performance of their stock. It is a pity because their project looks very promising. I hope the project goes forward as the world needs those metals, however, Chile is becoming a problematic jurisdiction.

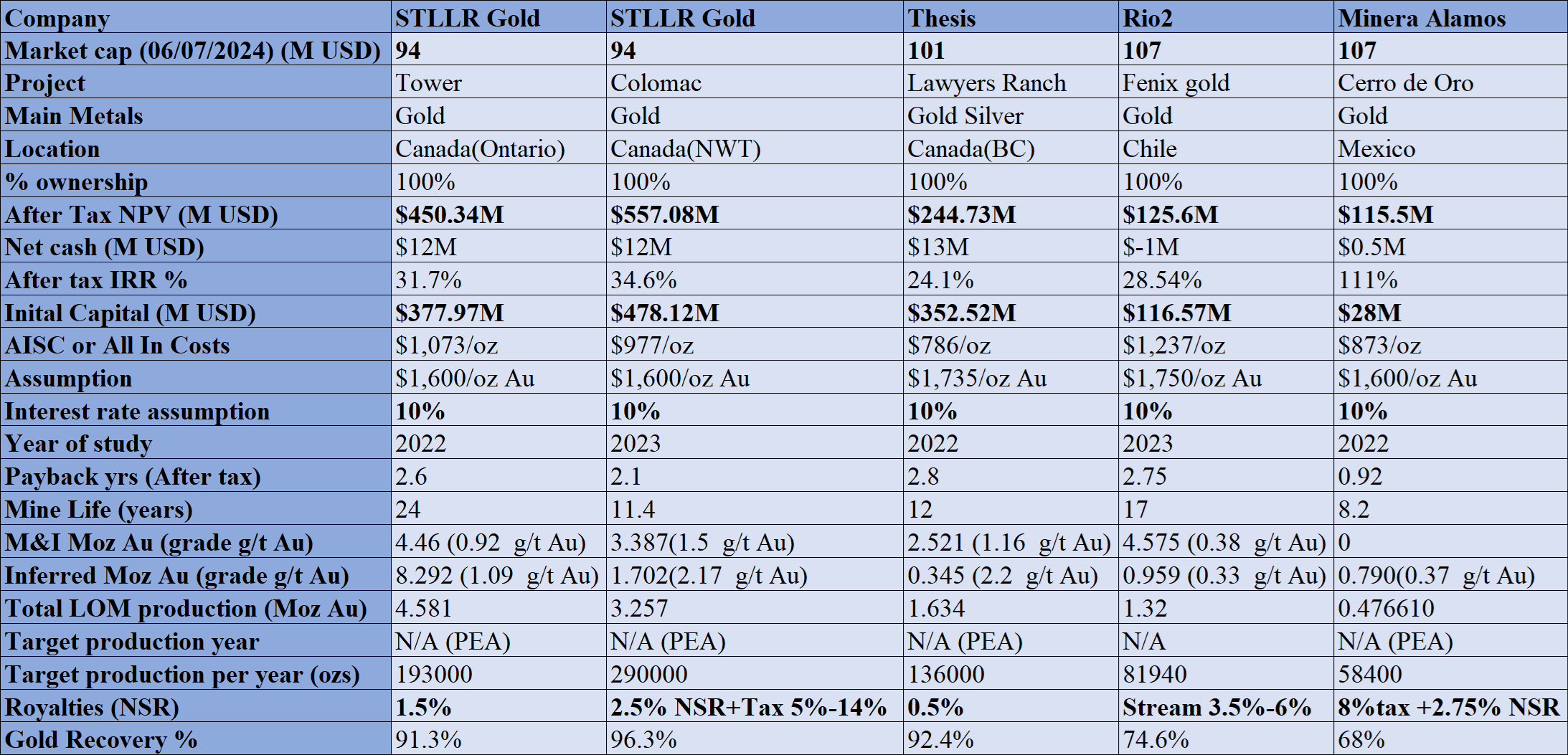

STLLR is very unknown but the CAPEX on their projects is too high for their financing capabilities. However, for those willing to take the risk, it’s probably the type of company that offers a lot of leverage to the gold price, if metal prices perform better than expected.

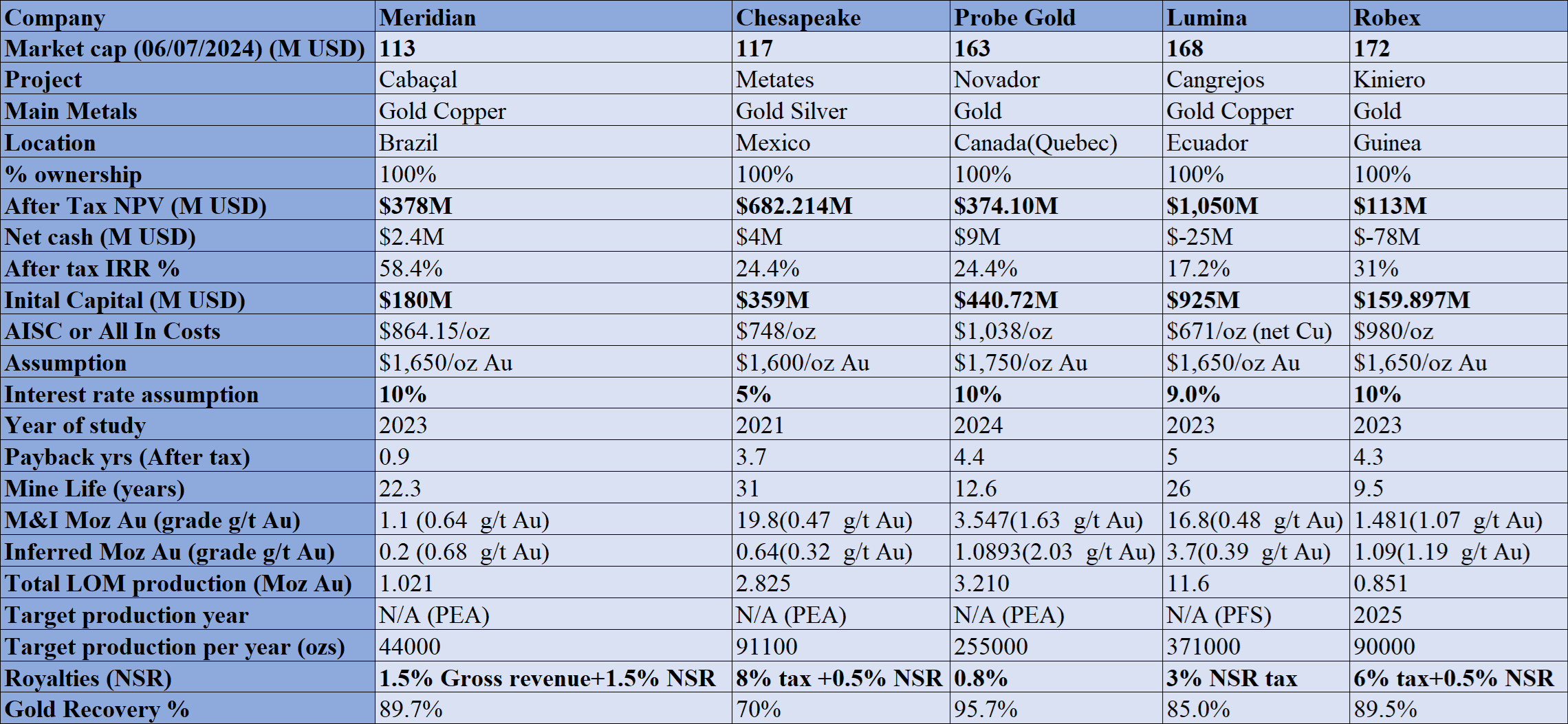

Canadian developers <$180M market cap

Data on Canada listed developers<$180M market cap. Mining economic reports (PEA, PFS) and my own estimates.

The list above has some very good projects. Probe gold will produce a staggering 255,000 ounces per year; however, their CAPEX is massive. Lumina will also produce a great amount of gold per year: 371,000 per year but their CAPEX is even higher than that of Probe Gold.

My favorite one here is Meridian. They trade at a massive discount to NPV (10%), their life of mine is long, and CAPEX is reasonable. However, they will produce 44,000 ounces per year, which isn’t much. They are also in Brazil, in which I already have a very large investment through Ero Copper. I’m not sure I want more mining exposure to the country, although I’m considering a PGM investment in Brazil.

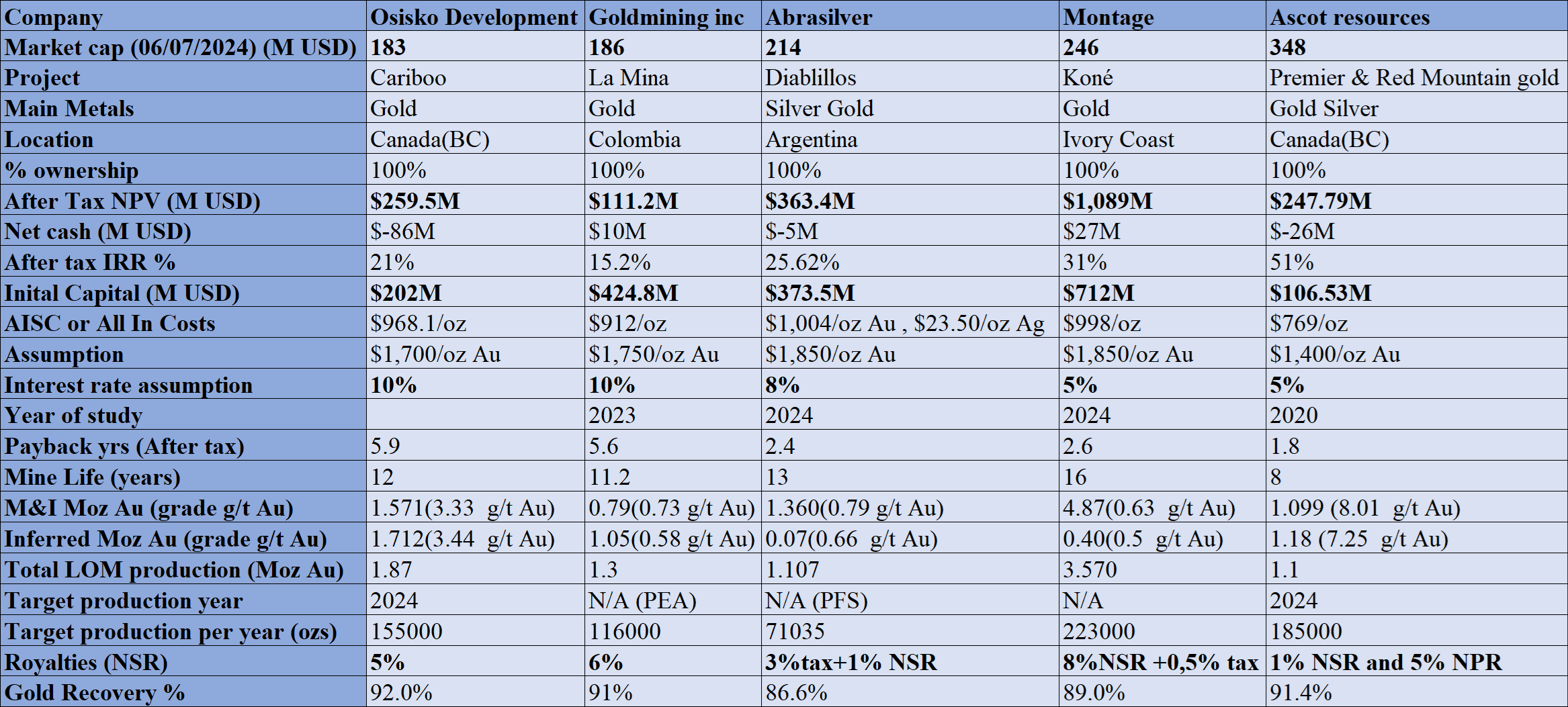

Canadian developers <$350M market cap

Data on Canada listed developers<$350M market cap. Mining economic reports (PEA, PFS) and my own estimates.

From the projects above my favorite projects are Montage and Ascot as they will be very significant projects. However, I’m not comfortable investing in Ivory Coast and Ascot has a very high NPR which will reduce the profitability of the project.

The worst project I have seen by far is La Mina, owned by Goldmining Inc. The ratio of NPV to CAPEX just makes no sense.

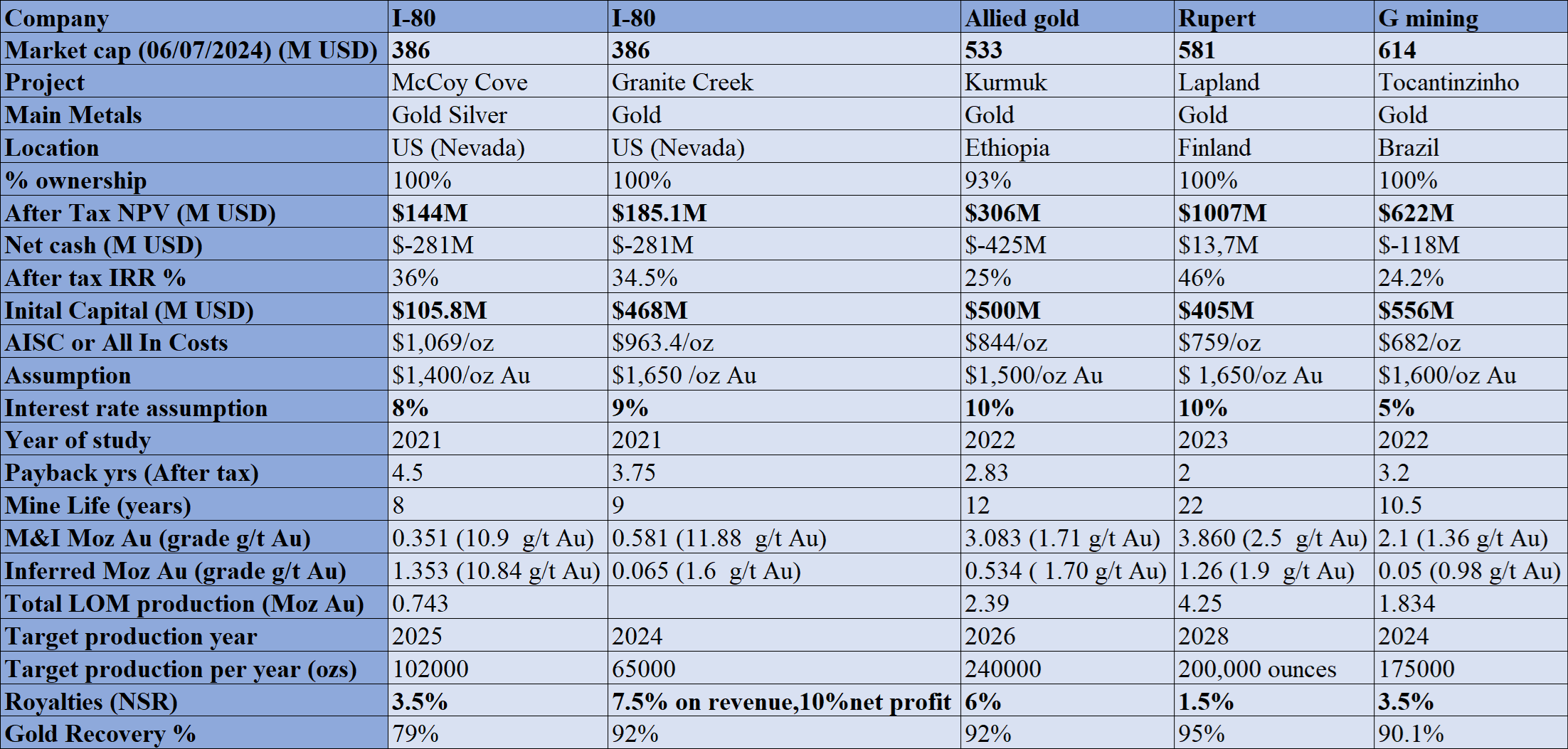

Canadian developers <$620M market cap & Aurion

Data on Canada listed developers<$620M market cap. Mining economic reports (PEA, PFS) and my own estimates.

From the projects above my favorites are the ones owned by Allied Gold and Rupert Resources. In the case of Allied I don’t like their CEO, Peter Marrone, due to the simple fact that he was way overpaid in Yamana, and he didn´t deliver much shareholder value if we include dilution. In 2014 he was the best paid CEO in Canada. This makes no sense to me considering Yamana was nowhere near the largest company in the country. Also, I dont like about Allied the fact that they operate in Africa.

In the case of Rupert, I have found a “creative” way to get exposure to their asset. I own shares in Aurion Resources, an explorer that owns adjacent land to the project owned by Rupert. B2Gold got into a JV with Aurion years ago and made some gold discoveries. Now B2Gold has sold the JV to Rupert resources in exchange for shares in Rupert. I expect consolidation in that area very soon. I went into more details on Aurion ealier in the report.

Canadian developers <$1,000M market cap & Aurion

Data on Canada listed developers<$1000M market cap. Mining economic reports (PEA, PFS) and my own estimates.

The table above has some interesting projects, more so considering they are the largest Canadian projects in my list. The best project is probably Hod Maden, owned by SSR mining. Unfortunately, SSR has had environmental problems in Turkey and therefore I don’t want to own them. The liabilities arising from this environmental issue are unknown and could be very expensive for SSR.

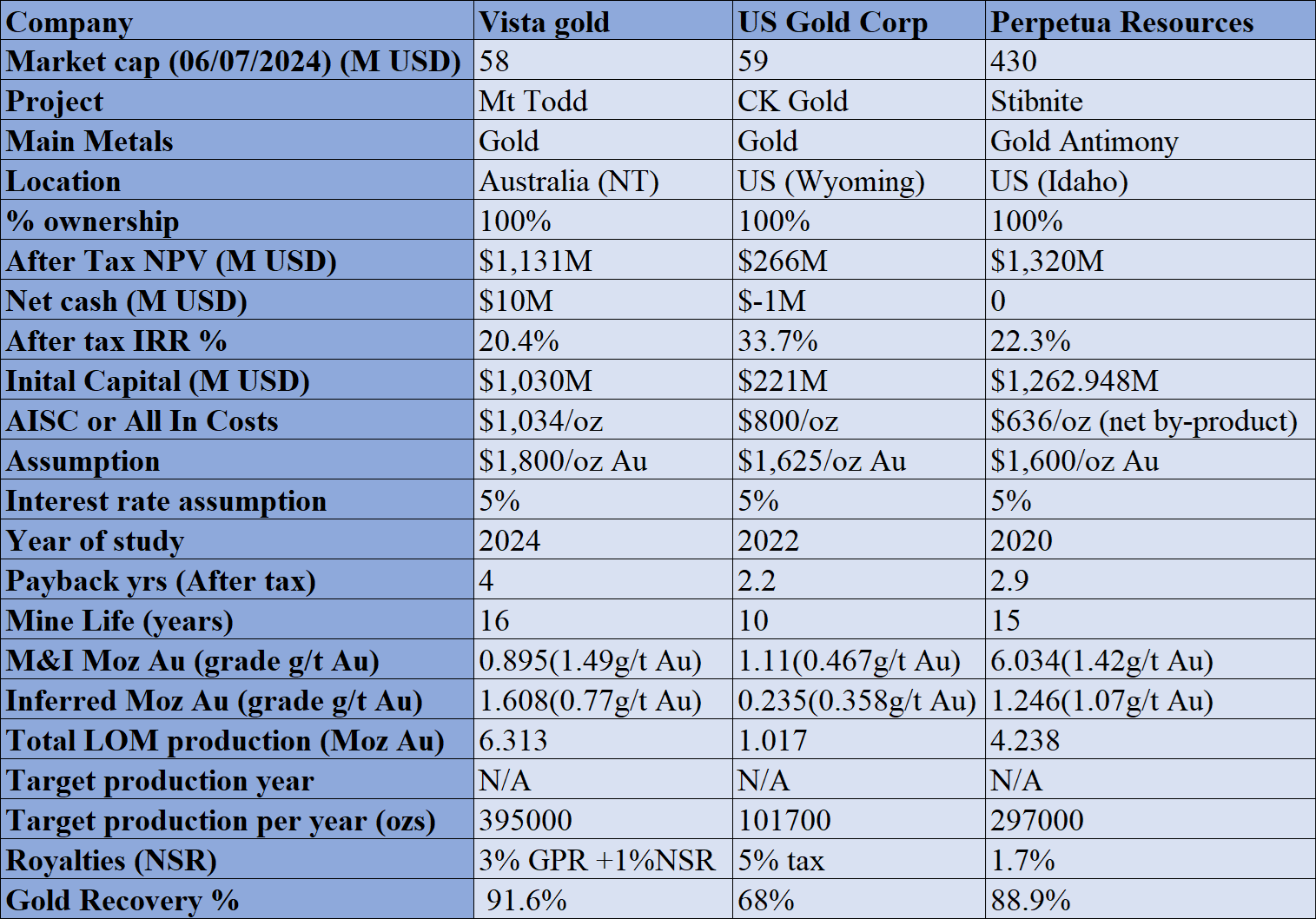

US listed gold developers

Data on US listed developers. Mining economic reports (PEA, PFS) and my own estimates.

The US listed projects I have found are all large, with 100,000+ ounces per year production profile. Probably the most interesting one is Vista Gold, but their CAPEX is too high relative to the market cap.

UK listed gold developers

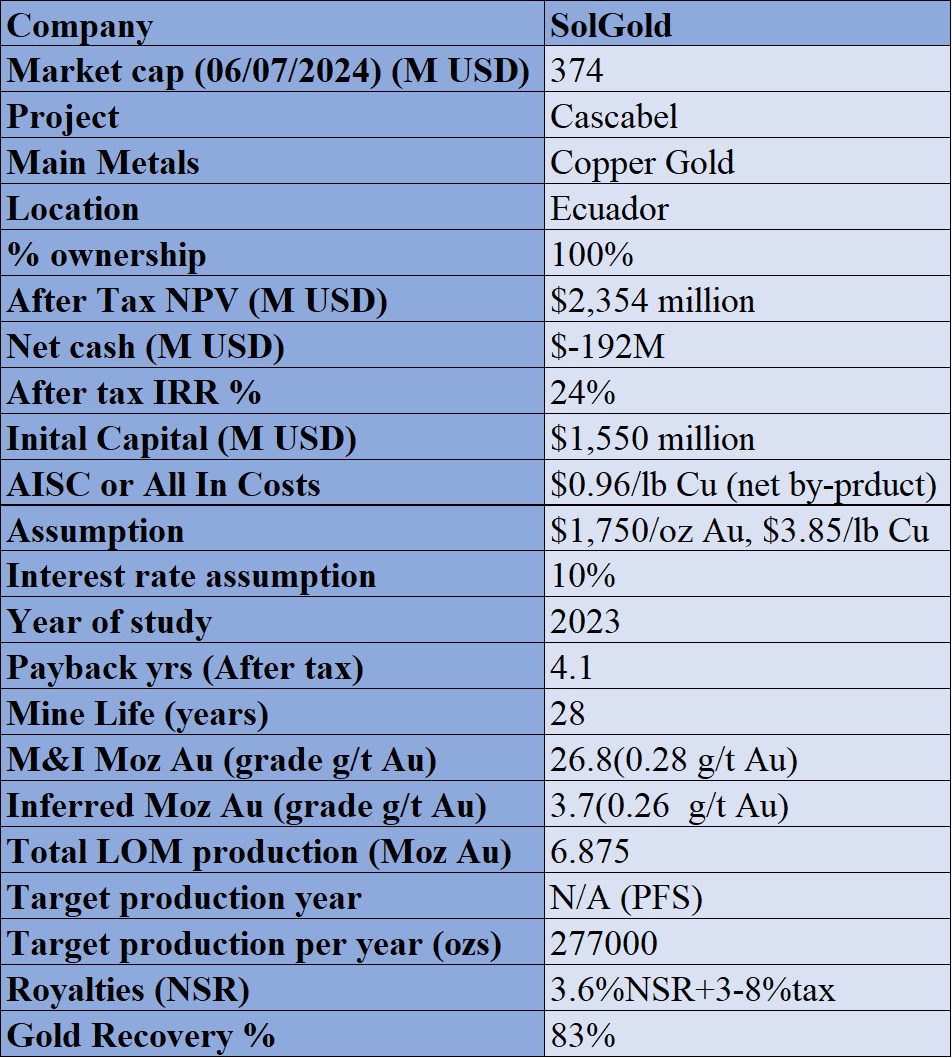

Data on UK listed developers. Mining economic reports (PEA, PFS) and my own estimates.

SolGold is the only significant developer trading in the UK with a lot of gold in their deposit. The only negative I see on SolGold is the fact that it is still trading. By that I mean that as far as I can see it’s an exceptional deposit, with great economics even at 10% discount rate. It seems like the Ecuadorian government is helping SolGold with the financing, but I don’t want to expose myself or my managed account to that kind of risk. It seems odd to me that SolGold has not been taken over yet by another larger miner.

ASX listed gold developers

ASX developers <$70M market cap

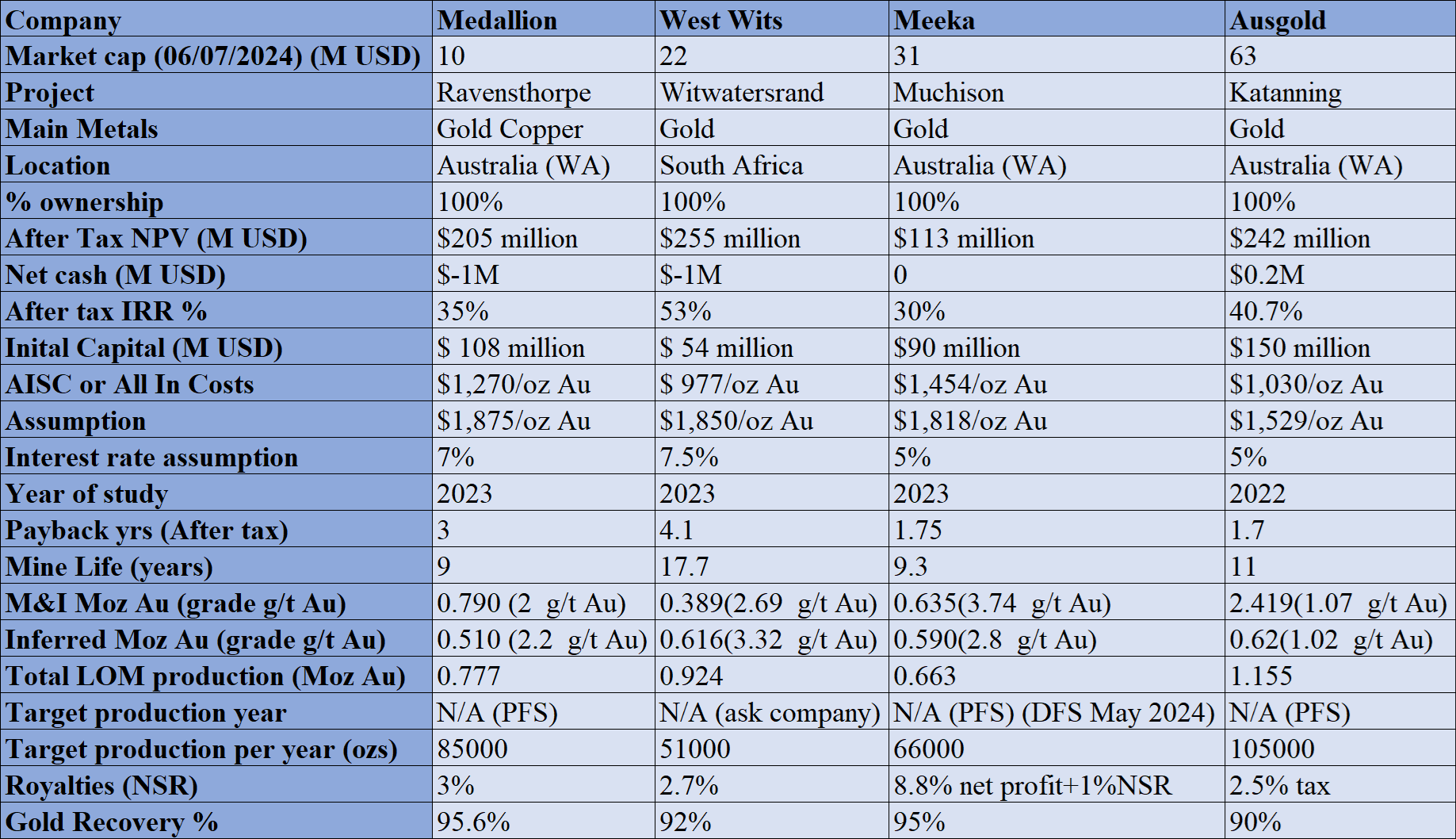

Data on ASX listed developers<$70M market cap. Mining economic reports (PEA, PFS, scoping studies) and my own estimates.

It has been very interesting exploring the universe of ASX listed gold stocks. Their approach to developing assets is more straightforward than that in Canada or in the US. Also, some of them use a stricter measure of costs: All in costs (AIC), which includes more costs than the typical AISC. The main negative I have seen is that they display measured and indicated resources separately, therefore I had to weight the size and grade of the resources to get to a M&I grade and resources size, which meant a lot more work.

In the first table there are some projects which I find very attractive. Firstly, Medallion Metals, which is one of my top picks, they use AIC and AISC, which I appreciate. The cost in the table is the AIC, therefore it’s a low-cost project. Its discount to NPV is massive. I already did a deep dive on Medallion earlier in the report.

West Witts has one of the best projects I have ever seen, but I’m not willing to invest in South Africa. However, if you are fine investing there it’s a very good option. I would wait for their next capital raise though; they seem to be a bit light in working capital.

ASX developers <$1000M market cap

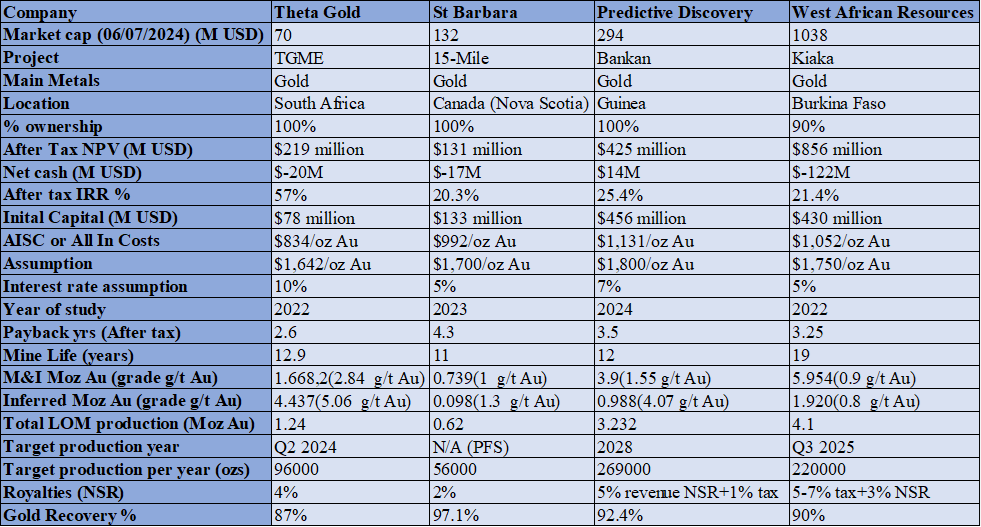

Data on ASX listed developers<$1000M market cap. Mining economic reports (PEA, PFS, scoping studies) and my own estimates.

I like all the projects in the table above except the one owned by St Barbara. I don´t like the balance sheet of St Barbara either.

The other projects are in jurisdictions I’m not happy investing in.

Gold mining firms

Canada listed gold miners

When looking at average revenue growth bear in mind that miners like Orezone just started producing recently. Therefore, their average annual revenue growth is unlike others.

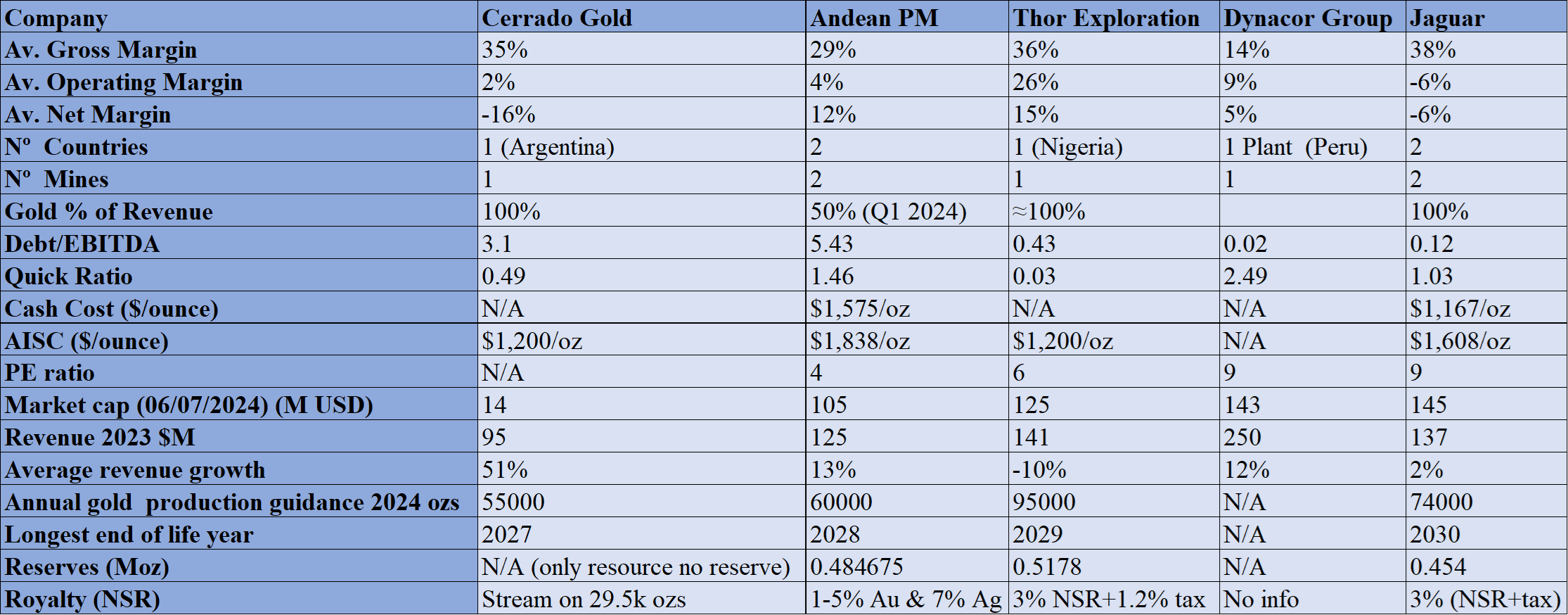

Canadian miners<$145M market cap

Data on Canada listed miners<$145M market cap. Mining economic reports (PEA, PFS), investor presentations, financial reports, and my own estimates.

From the miners in the table above the miner I like the most is Jaguar given that they have the longest life of mine, and they are backed by Eric Sprott. However, 6 years of mining life is too short in my opinion.

Dynacor is not strictly a miner. They own a plant in which they process ore from other miners. Therefore, their business model is much less risky. However, I don’t like Peru as a jurisdiction for a large investment. That said, for those of you who are risk averse, firms like Dynacor offer leverage to precious metal prices, with lower execution and logistical risk than conventional miners.

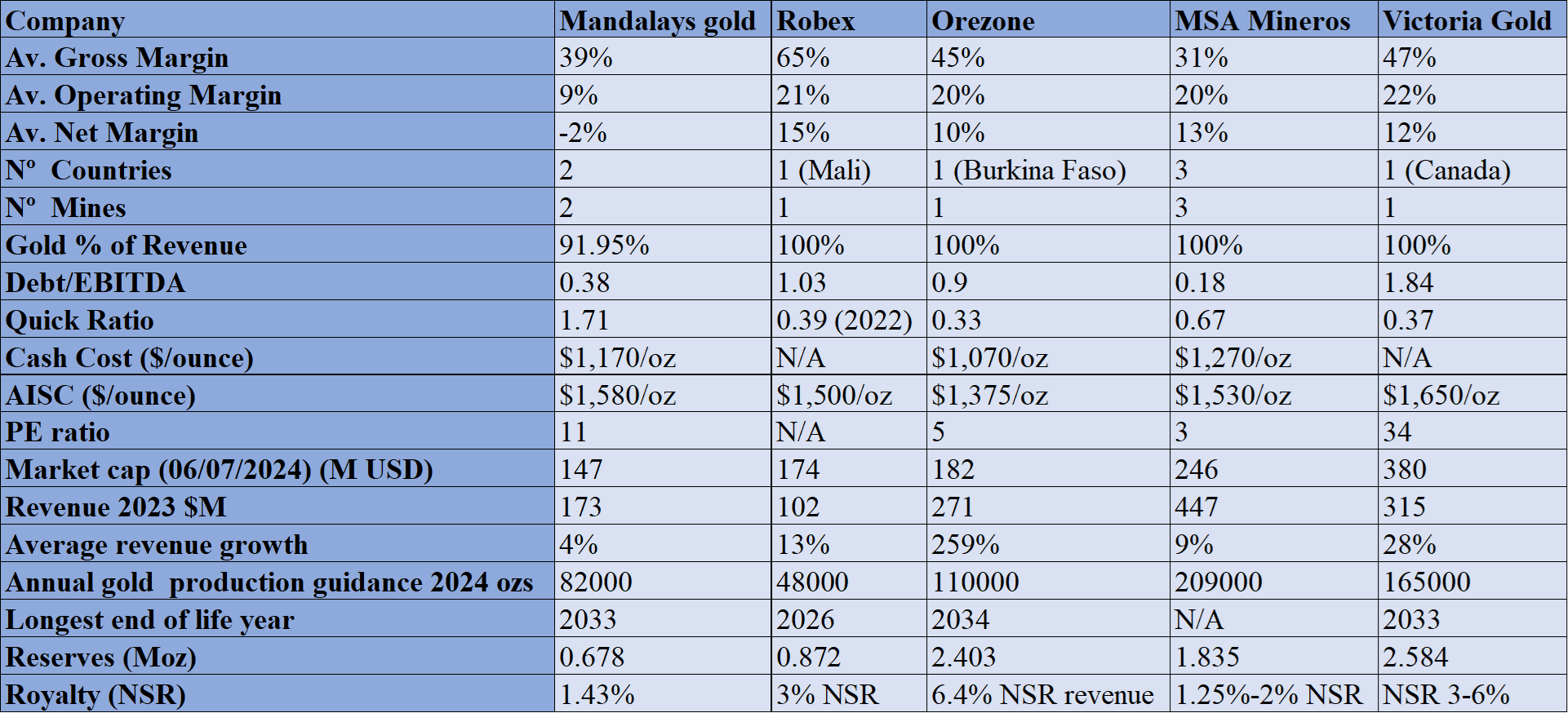

Canadian miners<$400M market cap

Data on Canada listed miners<$400M market cap. Mining economic reports (PEA, PFS), investor presentations, financial reports, and my own estimates.

Victoria Gold seemed like an interesting choice when I first check it out but at a PE ratio of 34 it seems too expensive. Orezone has very good economics, revenue growth and at least 10 years of life of mine, but Burkina Faso is not investable for me. MSA Mineros seemed like the most interesting. They have some jurisdictional risk, but they are very profitable, they have low levels of debt and have some good reserves. Unfortunately, I have reviewed workers opinions on MSA Mineros, and working conditions are rather deficient. I have read opinions about workers complaining about lack of safety measures and I have read workers complaining about work not getting paid. I don’t want to invest in a company with that work environment.

Canadian miners<$1,000M market cap

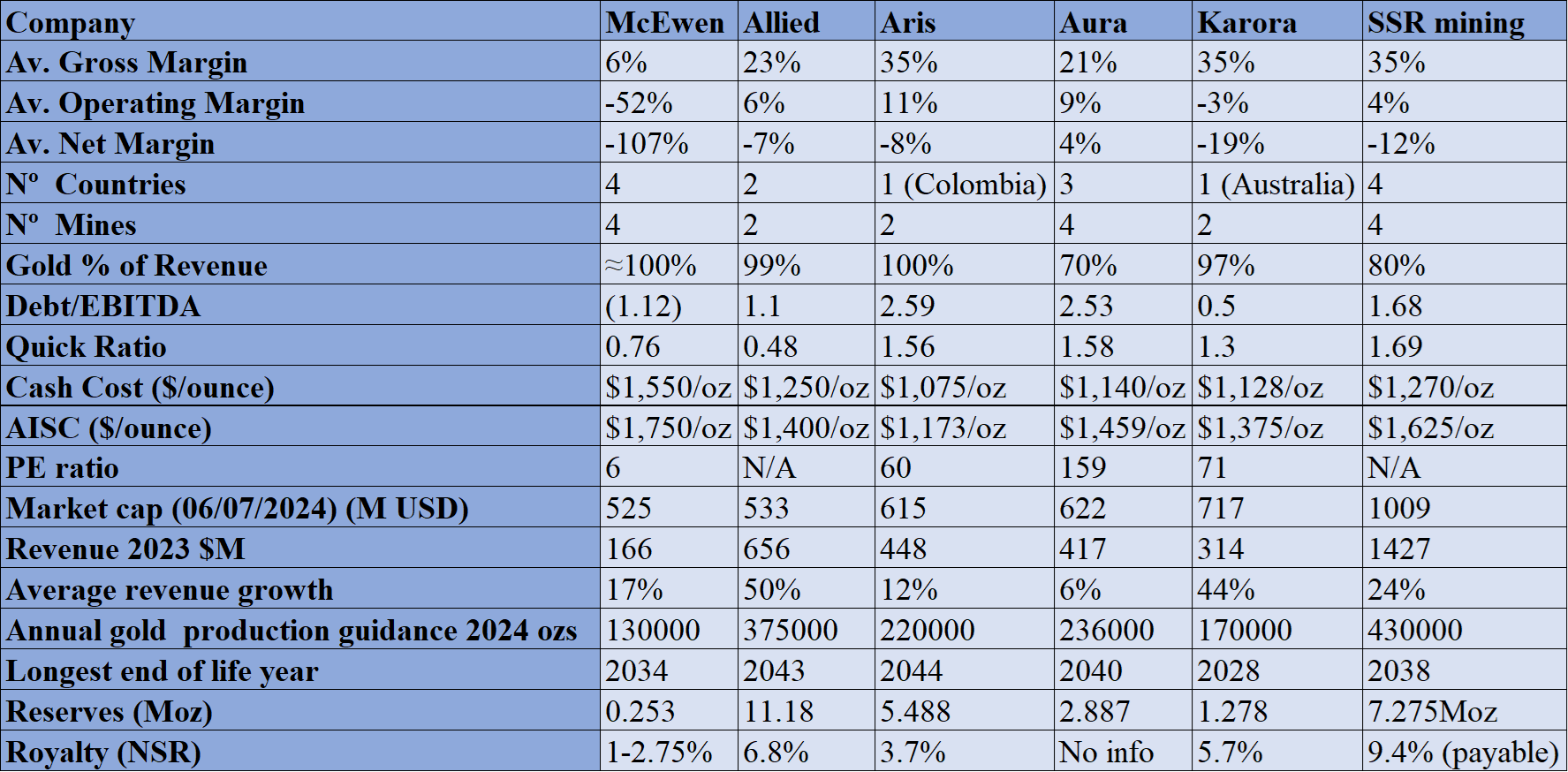

Data on Canada listed miners<$1,000M market cap. Mining economic reports (PEA, PFS), investor presentations, financial reports, and my own estimates.

The miner I like the most from the last table is SSR, but due to the environmental disaster in Turkey they aren’t profitable and the liability there could be huge. The other miners have a PE ratio too high for me. And McEwen Mining has a terrible track record, they have mostly destroyed shareholder value.

Both Karora and Allied have very high revenue growth. But Karora has terrible margins. Allied is too exposed to Africa, a region I think will become more unstable in the short and medium term.

I also considered Galiano Gold for this report as it fit all my criteria. However, given that they just bought into the JV they previously held with Gold Fields and that it seems like they can’t make a profit out of it, I preferred to leave them out. It is yet to be seen if they operate the mine just as well now that Gold Fields is out of the JV. Also, the terms of the purchase seemed a bit expensive in my opinion. Also, liabilities have spiked for Galiano, and their gold hedging strategy is making them lose money, which may indicate a lack of financial expertise on their side.

Canadian miners<$1,500M market cap

Data on Canada listed miners<$1,500M market cap. Mining economic reports (PEA, PFS), investor presentations, financial reports, and my own estimates.

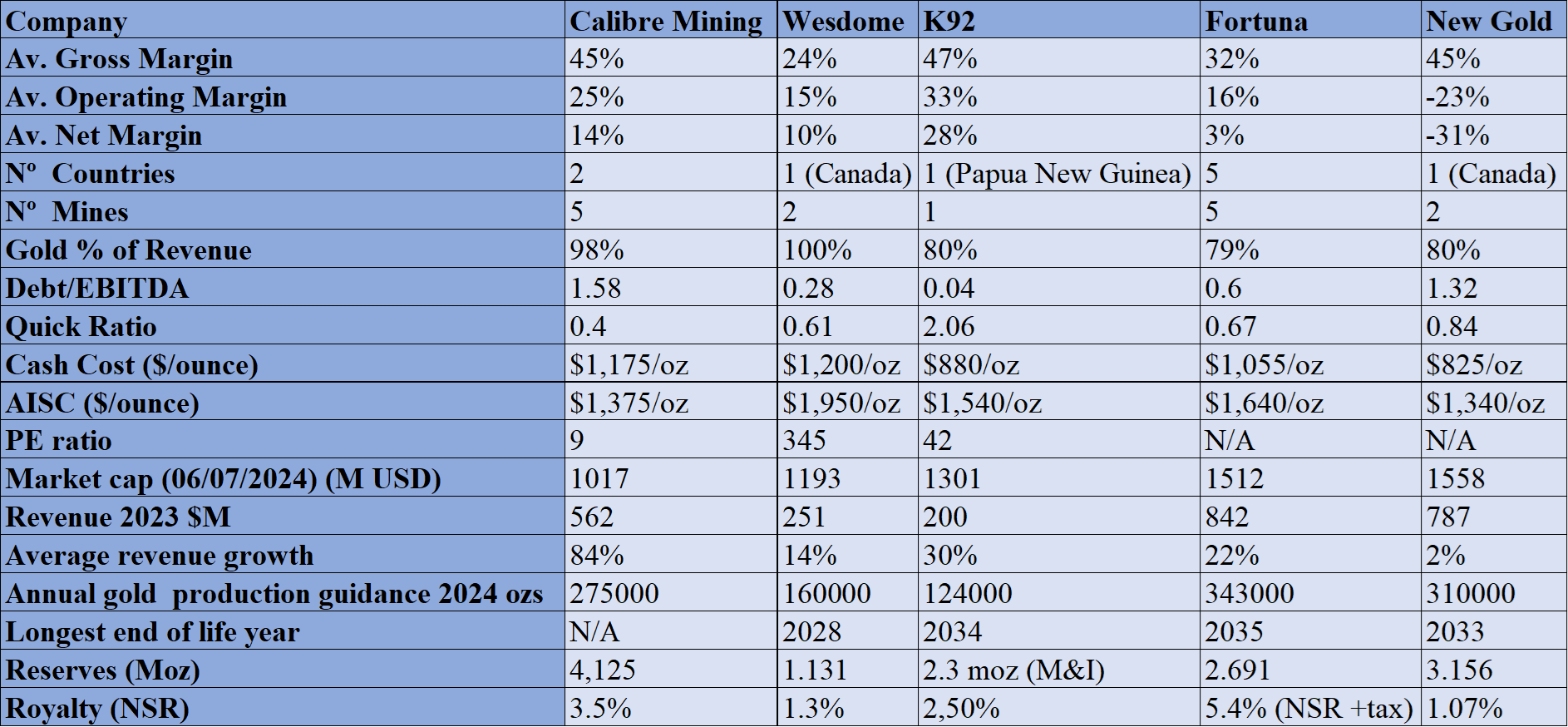

By mistake I analyzed a few companies above my $1B threshold. The most interesting one by far is Calibre Mining. However, Calibre Mining is about to spend $336M in their Valentine project, and the debt they went into to buy Marathon matures in 2027. Which is not a reasonable timeframe considering that at its peak, Calibre made $85M net income in 1 year. I think Calibre is going to spend more on CAPEX and debt repayments than on shareholder returns. The other miners in the table trade at a PE ratio too high for me, or are not profitable now, which is not acceptable with current metal prices in my opinion.

ASX listed gold miners

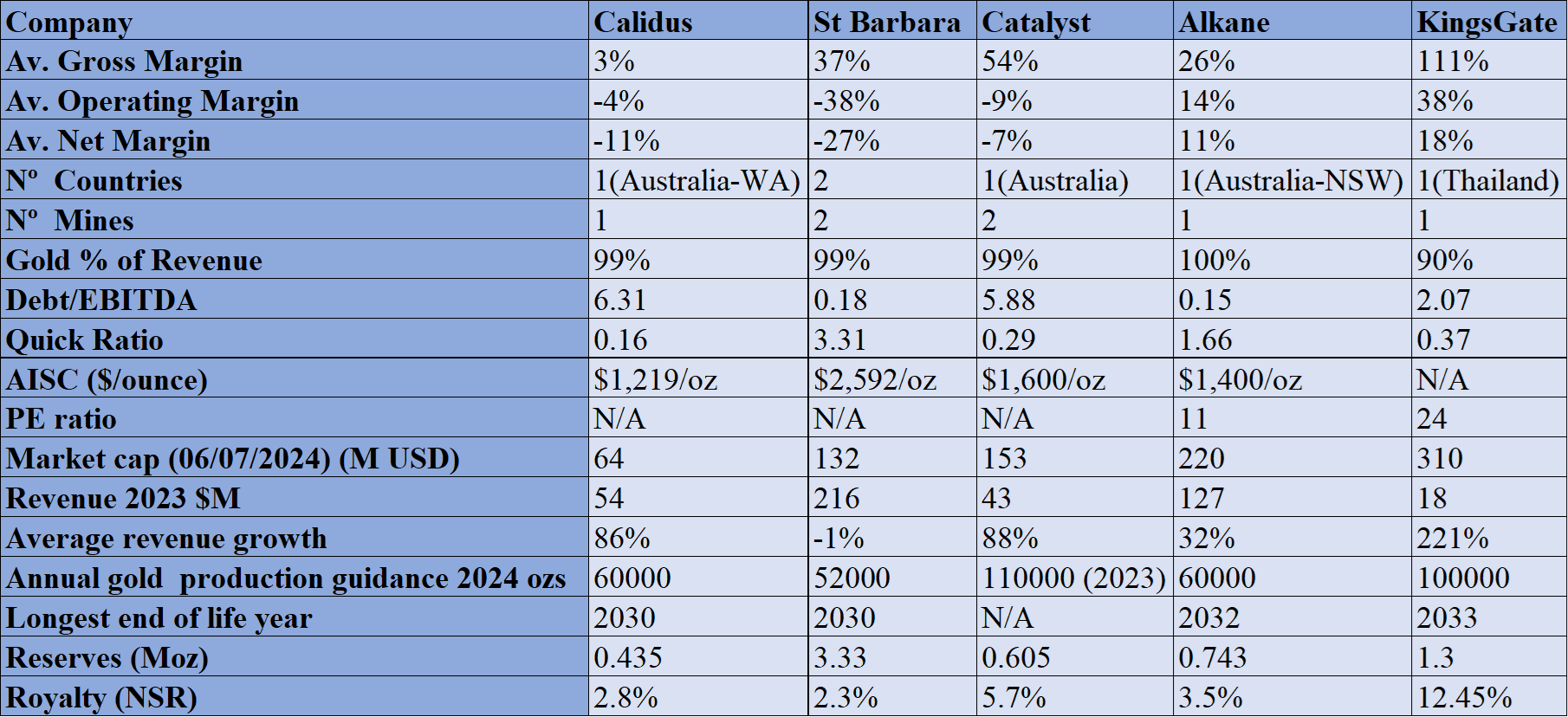

ASX listed gold stocks don’t use measures like cash costs, that´s why you will find cash costs in Canadian or US miners, but not in the tables of ASX stocks. Please take into account that Catalyst, KingsGate, Pantoro, Orabanda, Calidus and Genesis have recently started producing metals. Therefore, their debt levels and revenue growth are much higher than others.

ASX miners<$350M market cap

Data on ASX listed miners<$350M market cap. Mining economic reports (PEA, PFS, scoping studies), investor presentations, financial reports, and my own estimates.

The table above has a lot of new miners. Namely Calidus, Catalyst and KingsGate. They are, however, very much indebted, and not very profitable (except Kingsgate). The miner I like the most from this list is Alkane due to their profitability, low debt and that they operate in one of my favorite jurisdictions. However, Alkane is running low on reserves and by 2032 they may be out of business.

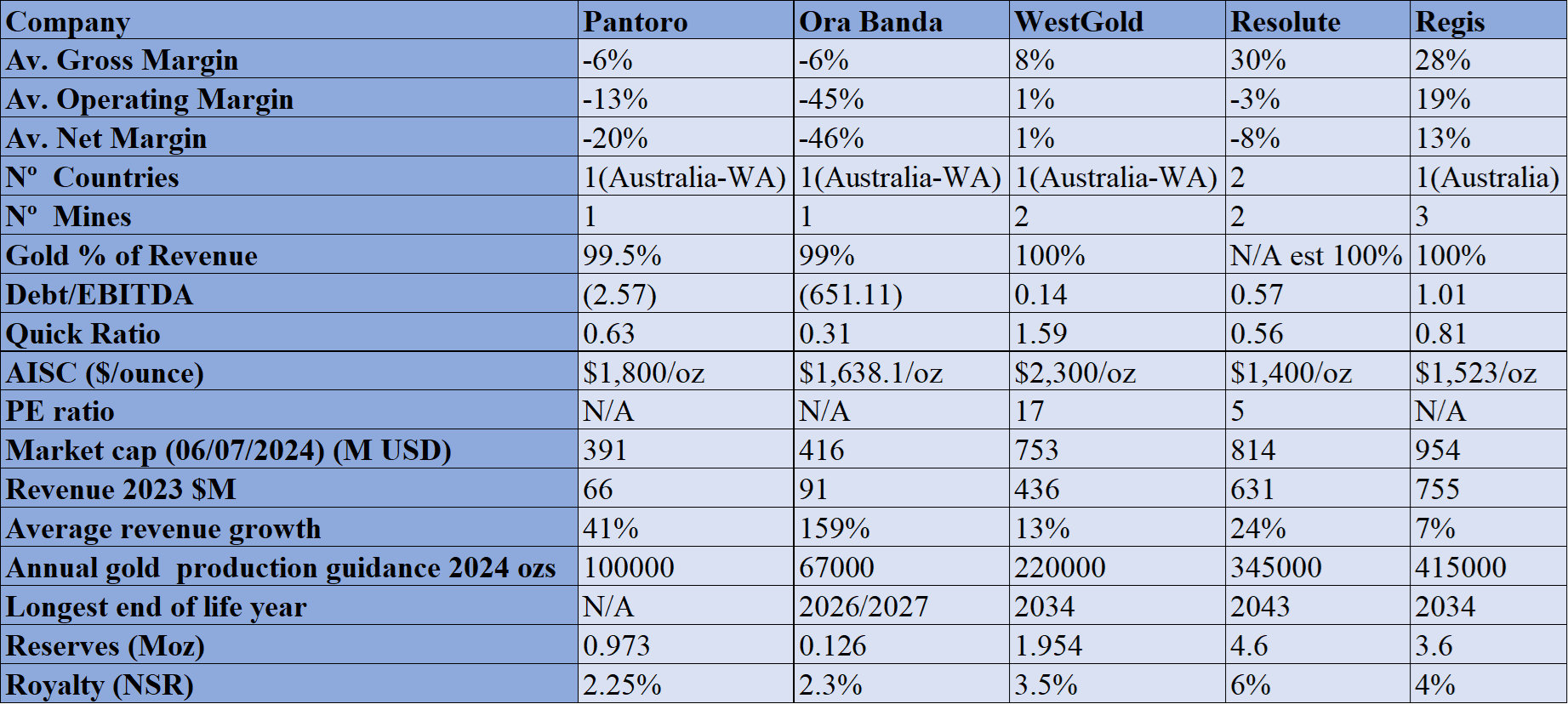

ASX miners<$950M market cap

Data on ASX listed miners<$950M market cap. Mining economic reports (PEA, PFS, scoping studies), investor presentations, financial reports, and my own estimates.

From the miners shown above, WestGold and Resolute are the only profitable ones. Resolute is the one I like the most by far due to their large mineral reserves, which will enable them to produce at least until 2043. However, resolute has an average 6% royalty of its assets which I dislike very much. Please bear in mind that the higher the gold price the higher the royalty tends to be. So having streams or royalties on a miner really reduces both profitability and leverage to gold prices.

The average historical margins of Ora Banda are so low I’m not sure how they will stay in business. My guess is that soon another miner will buy their assets for pennies if they go broke.

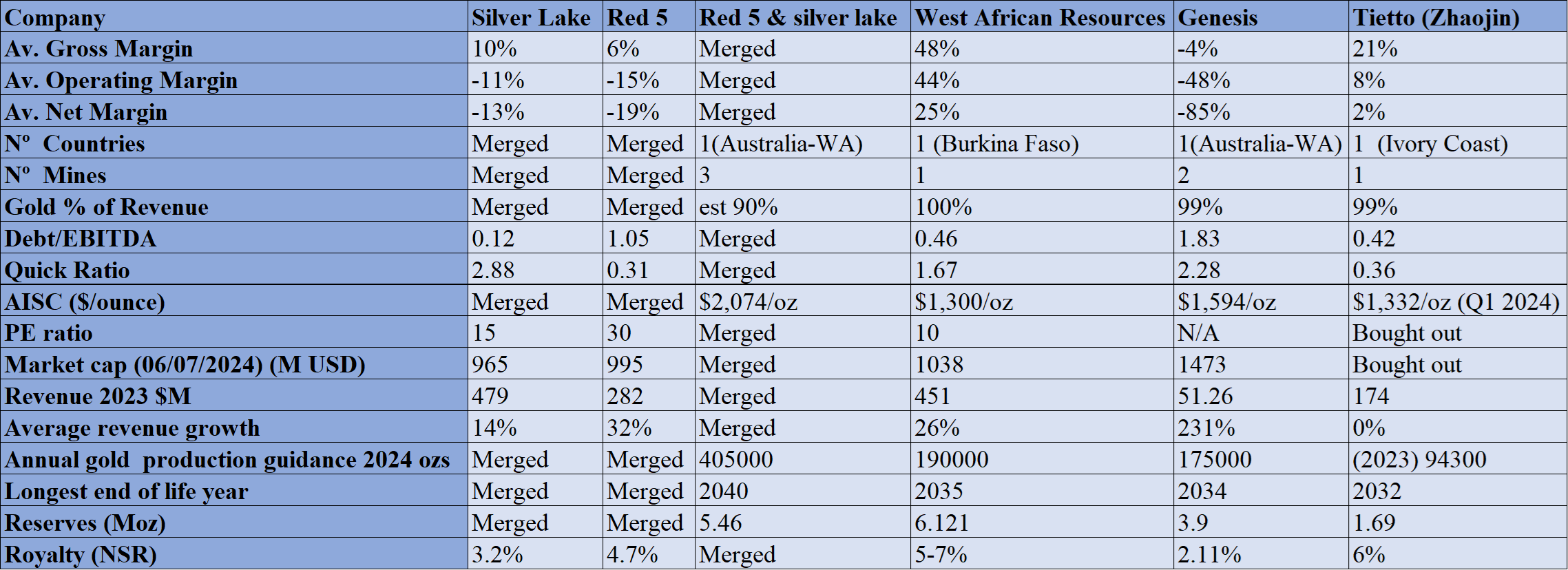

ASX miners<$1500M market cap

Data on ASX listed miners<$1,500M market cap. Mining economic reports (PEA, PFS, scoping studies), investor presentations, financial reports, and my own estimates.

Once again, I made the mistake of analyzing a firm above my threshold of $1B market cap: Genesis.

Red 5 and Silver Lake and merging and they will become a gold behemoth that will produce 400,000 ounces a year. However, I don’t like their high cost of production at over $2,000/oz. That said, it’s a producer that offers a lot of leverage to gold prices. But I don’t like the lack of margin of safety in that stock.

Conclusion

Unfortunately, I haven´t found any gold producers worth putting money in. I have found 2 gold developers and 1 explorer/early-stage developer that I think will soon become takeover target: Liberty Gold, Medallion Metals and Aurion Resources. I have also found a publicly listed gold broker: A-Mark Precious Metals. I own shares in all of them, both on my personal portfolio and through an account that I manage.

The developers will become takeover targets, as soon as reserves start to decrease in the mineral inventories of the larger miners. In the meantime, the rise in the price of gold should help the performance of the developers. And if Aurion can continue delivering good discoveries, the stock should perform even better than it has until now. And AMRK will become more valuable as demand for physical gold is rising rapidly.

I hope you all have found my report useful and informative. If you have any questions, suggestions, or stocks that you believe fit my criteria but haven’t been included in the report, please leave a comment and I will add them. You can also contact me through Twitter (X) at @AAGresearch.

Going forward I have planned a few reports: A report on my other exploration stocks. A report on how I approach stock picking (which a few subscribers have asked me to write). A report on uranium. And finally, I will write a report disclosing my full portfolio and the portfolio of the account I manage.

Thank you for your time.

Any feedback is welcome in the comments, or you can send me a message on Substack or through my twitter account @AAGresearch.

I want to thank my girlfriend Yeimy, who has helped me a lot at home while I was researching this by myself. Doing this report would not have been possible in 2 months without her support.

I hope this finds you well,

Alberto Álvarez González.

This is a real deep study, I´m really impressed !!!

Congrats !!!

Thanks Alberto, quite a resource on gold miners. I think there is one gold miner in West Australia that would meet your criteria as a buy, and it is bigger than some on your list. It is Beacon BCN.ax I think it is cheapest gold miner in world and it has great upside after getting a new property with high grade copper/gold outcrops. EV/EBITDA of 2.3 I wrote them up here: https://ceo.ca/@geodan/the-best-gold-miner-value-stock-in-the-world-looks-like-beacon Cheers