How I approach the valuation of precious metals royalty firms

How I approach the valuation of precious metals royalty firms

Case study of a gold royalty firm I recently sold

Introduction

A paid subscriber sent me a message a while back saying: “As a suggestion, many times when I read articles about investments, they are usually about cheap companies, which is great, but it would also be interesting to know when a company stops being cheap and it is time to get out”. And I thought it was a great suggestion, particularly because at the end of May I sold a big position I had in a gold royalty company.

So, I decided to write a report about how I value royalty companies in the precious metals industry and why I decided to sell Orogen Royalties at the end of May. I do confess that I probably sold it too early and the stock probably has some potential upside from here, but I didn´t feel comfortable holding any longer at these valuations. However, I was happy with a more than 140% gain and the possibility of deploying that capital towards my top pick Manolete Partners.

It is a pity I did not get a chance to write about Orogen before I sold it. However, I decided instead to write about the picks I have a higher conviction in such as Manolete Partners, Ero Copper, Aurion Resources, Goliath Resources or Generation Mining.

Orogen Royalties stock price. Google Finance.

Summary

· In this report I will go through why I sold all my shares of Orogen Royalties, both in my personal account and through an account I manage, at the end of May.

· The firm has a producing asset (Ermitaño 2% NSR) and an exceptional development asset called Expanded Silicon (1% NSR), which holds a mineral resource of 13.3 million ounces of oxide gold through the Silicon and Merlin deposits.

· Ermitaño is operated by First Majestic Silver and Expanded Silicon is owned by AngloGold Ashanti. Both top quality operators.

· In the report I will also point out how I value royalty firms and what I look for in precious metals royalty companies.

About royalty firms

Royalty firms make payments to mining firms in exchange for a perpetual debt payment. This payment is based on the future production of a deposit. The agreement often involves a term called Net Smelter Royalty (NSR), which involves the mining firm giving the royalty owner a certain percentage of all the smelting proceeds of that deposit or project.

Historically royalty mining firms have delivered much better returns than mining firms. This is primarily because once they buy a royalty, they do not have to incur in any of the operational costs of that project.

In fact, in 2019, back when I was an intern in a family office in Madrid, I did some research in my own time and realized that royalty firms have delivered exceptional returns.

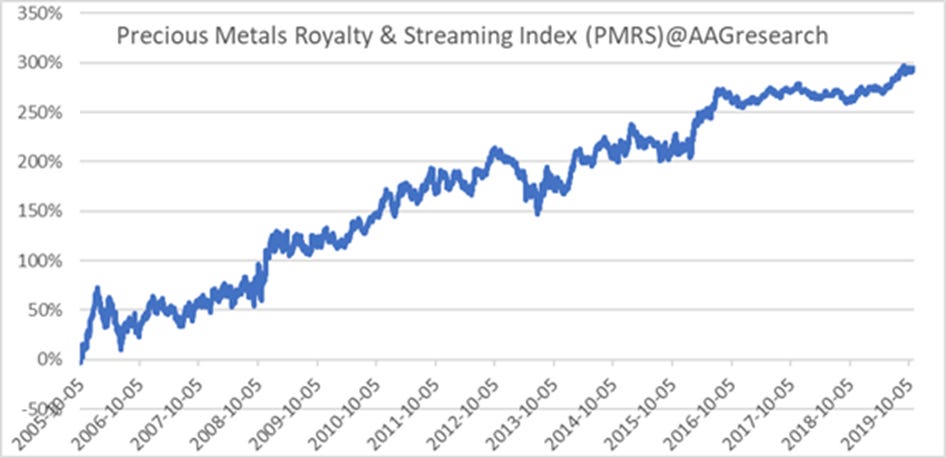

In fact, I built an index that was made of 100% precious metals royalty firms. And this index was weighted by market capitalization. This index beat the S&P 500, mining ETFs and most other indices by a long shot. Therefore, royalty firms are a good place to be invested if you do not want to make a lot of research into other firms.

PMRS Index. Own estimates.

Components of the index.

What I look for in royalty firms

· Great assets: As I pointed out in previous reports about gold and gold mining, the world is running out of reserves and resources for gold mining. Therefore, I believe there will soon be a bidding war for large and economically viable gold deposits located in top tier jurisdictions. Furthermore, the market for royalty purchases has dried up due to a lack of new royalties. This means that almost all the royalty assets available out there are already owned by royalty firms. Therefore, the only possibility of expansion is through M&A. Orogen ticked all the boxes as they own an exceptionally large asset in Nevada.

· Good location: the two flagship assets owned by Orogen are in Nevada and Mexico. Most importantly, the asset in Mexico is an underground mine. This is a key factor, as open pit mining is now disliked by the government in Mexico.

· Good management: Paddy Nicol, the CEO of Orogen has been in the exploration business for 20 years. And as CEO of Evrim (former name of Orogen) he made the Ermitaño royalty possible. Management in the mining business is key.

· Good balance sheet: Nowadays most of the royalties that are being generated are exploration targets, which are years or decades away from production. Therefore, you rarely want debt in your small royalty firms, albeit in the larger firms some debt may be in order due to the high return in capital invested. Orogen has more current assets than total liabilities.

· Production in the short term: As I just mentioned, a lot of royalty assets are years or decades away from production. Therefore, having a royalty asset that just started production or is close to producing is critical. This is the kind of thing that larger royalty firms will be looking at in the short term as potential takeover targets.

· The quality of the operator: Royalty firms do not incur in any of the costs of the mining asset. However, they have no say on how the asset is managed either. Therefore, it is very important for a royalty asset to be managed by a great mining firm. In the case of Orogen, First Majestic Silver and AngloGold operate Orogen´s flagship assets. These two firms are top quality producers when it comes to management of assets, albeit First Majestic has had profitability issues, and it is a much smaller firm than AngloGold.

How to value royalty assets

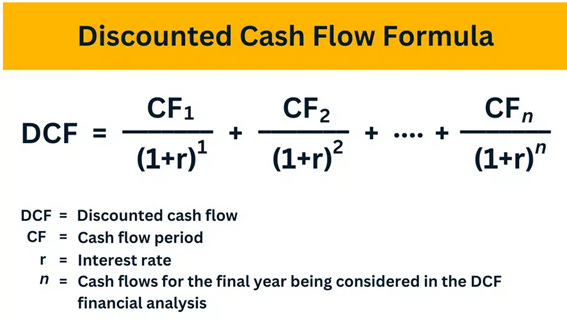

In my opinion there are two ways to value royalty assets: Discounted cash flow (DCF) on the one hand and project value on the other.

For those of you not familiar with either I will go into some detail:

DCF:

Formula for DCF.

Discounted cash flow is a valuation method that estimates the value of an investment based on its expected future cash flows. In the case of royalty assets, I just used the production output the firm announces or estimate my own and multiply that by different metals prices to get different scenarios. This value then gets multiplied by the % NSR the firm owns over said mining asset, all this results in the cash flow (CF) figure.

The tricky part of this method is to choose the interest rate. For mining I always use 10% as it is the least amount of interest any sensible bank or lender would ask for. The average interest rate in US history is around 7%. So, 10% for a mining firm is not too farfetched.

Project value:

This is the simplest method out there.

It just follows this formula: Production Project value in US Dollars = (Proven oz + Probable oz + Measured oz + Indicated oz+ Inferred oz) * royalty rate * current market price per oz.

This method, however, does not take into account interest rates nor time frame. I think both the DCF and Project value complement each other, hence I used both for the valuation of Orogen.

Orogen Royalties Valuation

The firm has two main assets: Ermitaño and Expanded Silicon (Merlin and Silicon deposits).

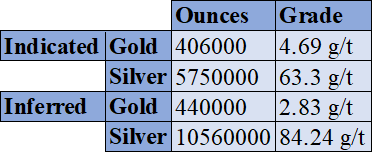

Emitaño project details. Resource studies.

Ermitaño is a high-grade silver and gold project. It produces 81,000 - 90,000 ounces of gold and 1.1 - 1.2 million ounces of silver (estimated over 90% of production from Ermitaño) per year. However, in terms of size its not very big and I think it has a life of around 10 years, which I have accounted for in my DCF analysis.

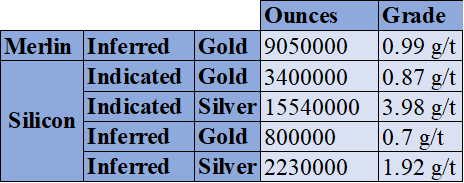

Expanded silicon project details. Resource studies.

The Expanded silicon project is a massive gold and silver project with decent grades. The project is in the development phase and AngloGold has a Prefeasibility study underway. Therefore, production is years away.

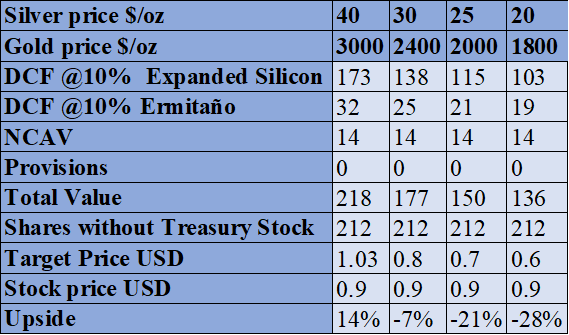

DCF Orogen Valuation. Own estimates.

The DCF Orogen Valuation shows that the firm is trading at a fair value or perhaps it is even a bit overvalued. Furthermore, even at higher metal prices, the firm does not offer much upside.

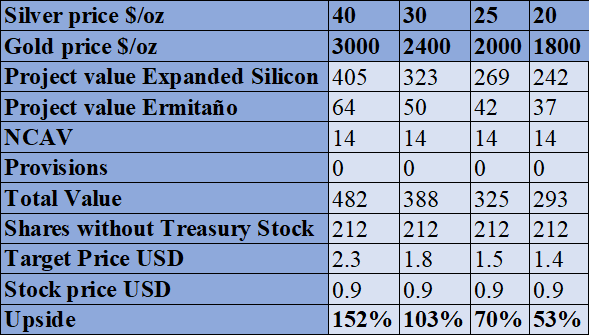

However, the project value method is much more generous with Orogen, probably because this method does not take time or interest rates into account.

I assume that the true valuation of Orogen of lies somewhere in between these two estimates and therefore I decided to sell. If gold prices are going to $3000/oz, I found that there are much better options available as I pointed out in my report about gold mining firms and AMRK.

When it comes to the calculation of the DCF, I assumed Ermitaño will produce 81,000 - 90,000 ounces of gold, and 1.1 - 1.2 million ounces of silver (estimated over 90% of production from Ermitaño) per year, for 10 years. And Expanded Silicon will produce just over 650,000 ounces of gold and 888,500 ounces of silver per year for 20 years. Bear in mind that royalties incur in no operational pr capital costs. So no costs are included in these calculations.

Project value Orogen Valuation. Own estimates.

Orogen owns another 25 royalties which are in exploration stage. I am not familiar with these assets so I wasn’t able to give them any value. Incidentally I do not think anyone can value exploration assets. The only ones I am familiar with are the ones operated by Heliostar Metals, which I think has good management. When it comes to mineral exploration opportunities, I much rather speculate with the firms I posted on my previous report: Aurion, Goliath, Azimut, Gladiator, Inflection, Hannan, CopperCorp and Radius.

Conclusion

Orogen Royalties will probably be taken over at some point in this cycle due to its existing producing royalty and the high quality of the Expanded Silicon project. However, at current valuations it does not make much sense to me. A high upside would be well into the three figures (something close to 500%) and Orogen does not get anywhere near that. The reason I am so demanding with the upside is that a high upside also often comes with a high margin of safety, something I think Orogen lacks at these prices.

I hope this report is of use for any of you looking into the royalty mining industry. For now, I have not found a royalty firm that is cheap and has all the components I mentioned in the report, but I am open minded, and I am always looking for a way to make money.

Any feedback is welcome in the comments, or you can send me a message on Substack or through my twitter (X) account @AAGresearch.

As always, I want to thank my girlfriend Yeimy, who has helped me a lot at home while I was researching this by myself. This report and this blog would not be possible without her support. Thank you.

I hope this finds you well,

Alberto Álvarez González.

What do you think about Sandstorm? They did a bad allocation raising debt and shares but nowadays it looks like one of the Royalties with higher growth for the next years

I’ve been reviewing all the gold royalty companies with market caps below $1 billion and have plotted their revenues, EBITDA and EV here (https://ibb.co/Hrtc6W1). What are your thoughts on EMX?

It appears to have the highest growth and surprisingly, the lowest valuation by far while being almost free of debt taking into account short term investments. It's trading at roughly the same EV/EBITDA multiple as Sprott, one of Kuppy's favorite proxies for gold despite its much higher growth.